EML & Fupay Join Forces To Launch Europe’s First Responsible BNPL-as-a-Service Product Attached To A Virtual Card

EML expands its connection with Fupay beyond Australia into a true growth collaboration.

EML expands its connection with Fupay beyond Australia into a true growth collaboration.

Join VIXIO’s upcoming webinar on May 20 with guest speakers from Gemini, Mackrell.Solicitors and the European Parliament to discuss how payments firms can balance innovation with crypto regulation.

A KPMG Private Enterprise report on Venture Capital investment in UK scaleup businesses in the first three months of 2021

https://home.kpmg/uk/en/home/insights/2021/04/investment-in-uk-innovators-soars-to-record-level-in-first-quarter-of-2021.html

Trust Payments announced it has expanded into Ireland. The payments technology group will open an office in Dublin city centre as it seeks to benefit from local talent and rapid growth in the country’s FinTech sector.

The new PXP research report ‘The COVID-19 Effect on European E-Commerce and Retail’,

explores UK and European consumer attitudes to the future of retail shopping.

Open banking platform Tink partners with payments technology provider Tribe for open banking payment initiation and account check services.

Blog post below –

https://tink.com/tink-tribe-payments-partnership/?utm_content=165197139&utm_medium=social&utm_source=linkedin&hss_channel=lcp-2735919

Thames Technology is delighted to announce its partnership with ekko, the latest member of Mastercard’s Priceless Planet Coalition, as it becomes the first fintech globally to use Thames Technology’s recycled plastic debit cards.

Sokin Enterprise has addressed the issue of traditional payments burdening users with high and hidden fees by creating a seamless cross-boarder payments ecosystem. Focused on facilitating speedy transfers and transparent fees for both consumers and businesses.

Three key things the UK can do to continue leading the way on fintech – innovation, inclusion and partnerships. Article by Jill Docherty, Head of Business Development, UK&I, Visa.

EML and Frollo have made financial history with the announcement of the EML Nuapay product suite.

Today, PPS, a banking and payment provider, announces that they will be powering a new B2B banking service for SMEs in Finland with accounting company Talenom. The brand new partnership will enable financial services to be integrated into Talenom’s emerging SME solution ‘Accounting Alex’ to modernise banking for SMEs in Finland.

Compliance, requirements, deadlines, oh my! By now you should have a comprehensive overview of what to be aware of as PSP. As such, it is time to wrap up the topic of SCA compliance. In this article, we cover how Okay uses security evaluations to fine-tune our product as well as how we can help you meet SCA PSD2 RTS compliance standards.

Compliance. A scary term for any payment service provider (PSP) in a world of increasingly stricter regulations and requirements. To make it a little less scary, we are opening the PSD2 RTS Compliance door to extract some key points of interest. Read on for the fundamental requirements PSPs should be aware of if issuing cards or e-money payments and why said requirements are necessary.

Join our upcoming webinar on May 11 to hear how fintech partnerships are driving innovation in payments in 2021.

Ambitious Danish fintech Blocser and top UK card manufacturer allpay.cards are ready to let ‘Butterfly’ take flight.

allpay.cards are providing their unique end-to-end card manufacturing solution to Blocser who are launching an app, with a payment card, to support the ever-growing number of UK gig economy workers.

In the wake of the financial crisis of 2008, financial institutions increasingly turned to ‘de-risking’ – exiting relationships and limiting interaction with clients deemed high-risk – as a way to reduce their exposure. Join industry leaders Mitch Trehan, Banking Circle’s Head of Compliance and MLRO, and Philip Doyle, Group Director, Financial Crime, Revolut as they take a deeper dive into the topic. They will explore some key questions:

– How has de-risking impacted the industry?

– Why are institutions de-risking, rather than managing existing risk?

– Has de-risking by traditional banks created a vacuum for new players to fill?

– How is the regulatory landscape shifting?

– What’s next for the payments industry?

Fintech is a market that is in many ways defined by specialism. The first fintech disrupters took aim at specific services and through technology reduced costs, improved the experience, and boosted accessibility. In this article, Moorwand CCO Luc Gueriane speaks to Financial IT about why fintech specialists need fintech specialists to succeed and scale.

Launching a payments business in Europe requires every founder to understand their market. That means doing customer research, scoping out competitors, and – perhaps the trickiest of them all – navigating the regulatory environment. In this payment guide, Moorwand breaks down three of the key regulations you need to know about when thinking about launching a business in Europe.

Get to grips on the road ahead with Level 2 of the EU Sustainable Finance Disclosure Regulation (SFDR), coming into effect for financial market participants and financial advisors from January 1, 2022.

On Thursday 29 April at 1.30pm BST / 2.30pm CEST join Eversheds Sutherland’s international panel as they discuss the future for blockchain, crypto-assets and smart contracts in financial services, including: crypto-asset regulatory regimes and how they differ; custody, security, smart contracts and tokenization innovations; and how the technology is shaping change in process applications and efficiency savings.

Stay up to date on the latest developments in the payments industry from the UK, Europe and beyond, with Eversheds Sutherland’s quarterly bulletin, Payment Matters.

In the latest edition, they discuss: significant developments in the UK’s plans for Open Banking and Open Finance; continued focus on the effectiveness of the revised payment services directive (PSD2); the Contingent Reimbursement Model (CRM); newly introduced for payment initiation service provider (PISP) payments, and the recent review published by the Lending Standards Board (LSB); and the success of Instant Payments in the Netherlands, and the drive for eurozone coverage, backed by the European Central Bank.

ekko partners with Paynetics UK to power fintech arm of new app that is turning the tide on climate change

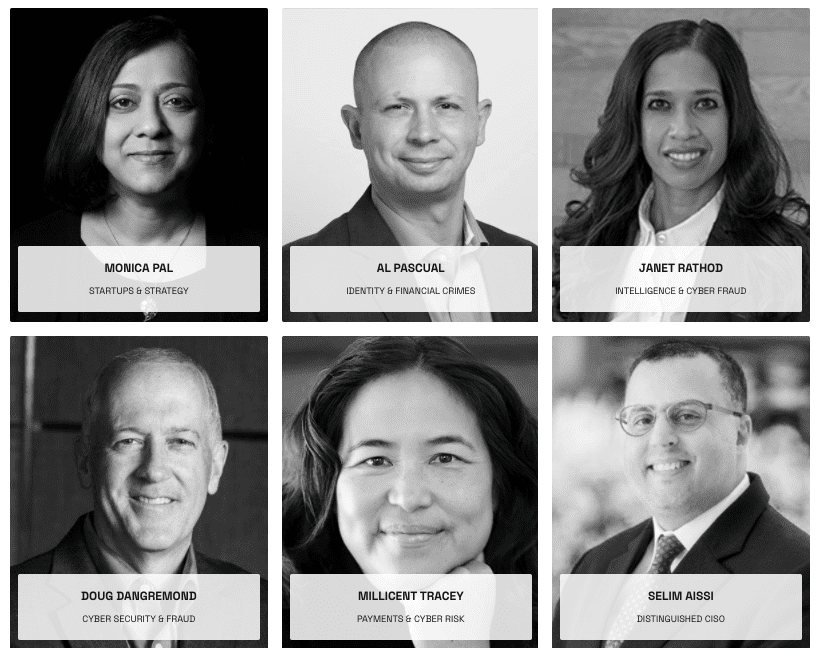

Revelock, the pioneer in behavioural biometric-based online fraud prevention (formerly buguroo) has announced the formation of its Advisory Board.

Six prominent industry experts – Monica Pal, Selim Aissi, Janet Rathod, Doug Dangremond, Millicent Tracey and Al Pascual – come together to bolster the company’s ability to proactively protect banks, fintechs and their own customers from ever-evolving fraud.

Revelock, the pioneer in behavioural biometric-based online fraud prevention (formerly buguroo) has launched its new Fraud Detection & Response platform for financial institutions.

The platform uses behavioural biometrics to continuously verify identities, protect web and mobile banking apps from account takeover, malware attacks RATs and phishing.

buguroo, a pioneer in behavioral biometric based online fraud prevention, has become Revelock after undergoing a major rebranding process as it enters a new era of online fraud prevention.

Spanish cybersecurity company also unveils the Revelock Fraud Detection & Response (FDR) Platform – updating and enhancing its capabilities to protect against more threats and further reduce the operational costs of fighting fraud – as well as a new Advisory Board made up of industry veterans.

Paynetics’ sister company phos, the fintech behind the leading software point of sale (POS), has partnered with Nordics fintech innovator maxaa to give merchants access to a complete and affordable digital payments solution.

The inaugural meeting of the International Institute of Finance (IIF) – The Payments Association Global Payments Forum was held on March 16, 2021 as a virtual event. Around 100 people registered for the first meeting from across IIF and Payments Association members and invited guests. The findings from that meeting are reported here.

Annex – Polling results in detail

One stop business payment solution provider, Safenetpay, has joined forces with ground-breaking payments specialist, Banking Circle, to further enhance its cross border payment offering. Utilising Banking Circle’s multi-currency accounts, SPayments Association and SWIFT transactions solutions and foreign exchange (FX) capabilities, Safenetpay’s business customers can now access additional currencies, competitive FX rates and quick, reliable transactions within SPayments Association.

In this payment guide, the Moorwand team break down the three key payments regulations a founder needs to know about when launching their new card programme.

Join Tandem, Lloyds, Trading 212, and TrueLayer on this webinar tomorrow, 28th April, and uncover the blueprint for high converting payment flows.

French consumers have no need to switch banks to enjoy state-of-the art financial management.

Irish consumers can now manage their money using just one card and digital app

Polish consumers can take advantage of great FX rates and 1% cashback rewards

The innovative risk management and fraud prevention company Cybertonica today announced its strategic partnership with Acuris Risk Intelligence (ARI), the independent data intelligence provider. The partnership will integrate Cybertonica’s cutting edge real-time behavioural biometrics platform with the Risk Intelligence flagship fraud product Cybercheck.

One of the more vexing problems of the modern age when it comes to international business is that regulatory regimes often do not keep pace with technological innovation.

Nonetheless, novel solutions to B2B cross-border business have emerged in the form of virtual IBANs, financial instruments that drive the innovation economy and enable new, powerful business models.

Here we have outlined three ways that virtual IBANs are transforming the way companies do business locally and abroad:

When it comes to digital banking and compliance, robust KYC practices not only prevent fraud and financial losses but also strengthen a firm’s ability to conduct business with confidence.

This is typically because of the four key elements of strong KYC practices that make sure firms know who they’re doing business with and what to expect from that relationship.

We’ve identified the four essential elements of effective compliance in KYC practices for digital banking in order to show you how they help improve the competitiveness of businesses of any size or scale:

The year 2020 saw many of the innovations and prognostications of analysts come true as contactless payments and digital banking solutions drove the field of Fintech innovations. Looking ahead, however, 2021 could be the year that consolidates much of this growth and prepares the economy for the next stage of digitization.

We at Monneo have identified five major trends that we think are driving the Fintech innovations in digital banking, in 2021 and beyond:

The digital banking era is upending traditional payment solutions and transforming the global financial industry in the process. And this is on both the corporate and consumer level with changes in payments solutions reaching into every facet of the international economy.

These innovations in digital banking are not only enabling increased efficiencies and expediting capital flows at a rate previously unthinkable but also are leading the way in changing the dynamic and level of depth of the business-customer relationship.

The reason why re-enrollment is so sensitive is simple: when you do an app-based strong customer authentication (SCA), the user has already been authenticated on the device. This means that it is possible to check the ‘possession’ factor using a device fingerprint from before.

If a customer has a new device, and has an existing device registered to their account, we recommend using SCA to enroll. A typical way to do this would be to use a QR code that the user can scan from one device to another. In the case where there are no existing devices linked to an account, we recommend that the customer go through a full “know your customer” (KYC) procedure in order to re-enroll their new device.

One of the ways we’ve helped our customers strengthen their re-enrollment process is to implement a mechanism known as ‘magic link’. A magic link is a link received through a semi-secure channel that authorises the customer to use a particular device. Using a link like this can be practical, as the re-enrollment procedure might be stretched out over time.

Interested in hearing more about Magic Links? Be sure to read the full article at okaythis.com/blog.

Join Modulr on 11th May at 10 am for the launch of this quarter’s industry pulse on payments – Leaders vs Laggards: The Race to Escape the Payments Dilemma.

We will discuss how leaders are overcoming their payments dilemma and overcoming the laggards as fintech fast-tracks innovations in a legacy ecosystem.

Secure your spot today: https://landing.modulrfinance.com/laggards-and-leaders-exclusive-launch-epa

Even with the advent of central bank digital currencies (CBDCs), senior policy-makers have said it will be some time before financial institutions can enjoy frictionless cross-border transactions.

Modulr receives strategic investment from the venture arm of FIS

• FIS Ventures invests in leading UK FinTech Modulr, as it drives real-time payments solutions and capabilities at a global scale.

• Modulr, the payments platform, is regulated by the Financial Conduct Authority and Central Bank of Ireland, with the EMI also benefiting from direct access to the Bank of England.

• The corporate and business payments market, in which Modulr operates, is considered to be worth $2 trillion, nearly five times as large as consumer payments.

National competent authorities have taken an ambiguous position on their enforcement deadlines for strong customer authentication — which has left the market unsure about how much flexibility there is, sources say.

Featured is one of Blue Train Marketing’s most recent blogs ‘QR Codes: A Secret History’. In this blog the writer, Jeff Banks, goes into detail of the history of QR Codes and how they are rapidly being adopted across the globe!

Checkout.com, the leading cloud-based global payment solutions provider, has announced the launch of its Payouts Product, which enables merchants to make seamless payments directly to eligible recipients’ cards and bank accounts.

The solution will enable merchants to make payouts in real-time to over four billion cards in over 174 countries and seamless payments to local bank accounts in over 40 countries around the world. It also leverages market-leading scheme and interbank FX rate sources, leaving global merchants with minimal exposure to currency fluctuations.

Payouts will enable the remittance, digital wallet, travel, insurtech and the gig economy industries to deliver more efficient, faster payments as a competitive differentiator. Checkout.com is the only payment service provider to have built a completely new infrastructure that spans the entire payouts value chain.

Online Payment Platform, the Netherlands payment service provider, has selected payments expert and licensed bank, Banking Circle, to enhance its marketplace offering.