Financial crime 2026 pulse report

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Developed in collaboration with The Payments Association’s Digital Currencies Working Group

Drawing on case studies from The Payment Association’s Digital Currencies Working Group, this report explores how stablecoins are being deployed across a range of use cases and where the opportunities, limitations, and bottlenecks lie.

This report was produced in collaboration with The Payments Association’s Digital Currencies Working Group, drawing on expertise from across the payments ecosystem, including law firms, consultancies, banks, and fintechs. It examines five different use cases of stablecoins, setting out the state of the market, case studies, and how the UK is positioned to leverage each.

The report draws on publicly available data, regulatory publications, and industry research. All factual claims are cited to primary or credible secondary sources. Where market figures or projections are referenced, sources are identified so that readers can verify and interrogate the underlying data.

What distinguishes this report is its practitioner foundation. Alongside the analytical sections, working group members—including organisations such as Travers Smith, Addleshaw Goddard, OpenPayd, Elmore Insurance, and Worldpay, among others—have contributed original case studies drawn from live implementations, regulatory engagements, and pilot programmes.

These contributions reflect direct institutional experience, offering concrete reference points for assessing the commercial and operational realities of stablecoin adoption in the UK today.

This section outlines the growth in the market for tokenised assets and how the programmability, settlement finality, and the atomic settlement capability of stablecoins enable them to function as digital money in this space.

$27bn

63%

$2tn

The rise of agentic AI introduces a fundamental requirement for machine-native payment infrastructure. Stablecoins, with their programmable logic, instant settlement, and interoperability with smart contract environments, are uniquely positioned to meet that requirement.

57%

#4

13x

A key long-term driver of stablecoin adoption may be the emergence of autonomous AI agents. Stablecoins are rapidly becoming a foundational element in the evolution of agentic commerce, where autonomous AI agents transact, negotiate, and settle payments on behalf of human users or enterprises with minimal direct intervention.

Stablecoins are a natural settlement layer for this model. Their value lies in programmability and composability: encoding conditions for execution and enabling automated chains of transactions triggered by incoming funds.

Traditional card rails, built for human-initiated, single-leg payments, cannot support high-frequency, sub-cent transactions. By contrast, fees on Ethereum Layer 2 networks have fallen from around $24 in 2021 to less than one cent, making such activity viable.

The opportunity is significant. McKinsey estimates agentic commerce could generate $3-5 trillion in global B2C retail alone by 2030. Smart contracts can also replicate card-network protections, with programmable chargebacks, conditional payments, and embedded dispute resolution.

Adoption will vary with the level of automation. The table below from McKinsey illustrates how autonomy differs across use cases.

Google’s Agentic Payments Protocol (AP2) is backed by more than 60 organisations, including major payment processors and banks. It integrates Coinbase’s stablecoin extension, x402, enabling agents to monetise services, transact with each other, and execute micropayments automatically.

Coinbase has developed similar tooling, with early demos showing end-to-end transactions from natural language input to stablecoin settlement. With Google, it built a proof-of-concept demo for Lowe’s Innovation Lab that turns DIY advice into a fully transactable experience. The agent workflow:

The result is a personalised, locally matched cart with fulfilment pre-arranged.

Governance questions remain, particularly around accountability, liability, and regulation when agents transact autonomously.

The UK’s principles-based approach to AI regulation identifies “autonomy risks” from agentic systems as an area requiring further attention, with bodies such as the FCA, ICO, and CMA expected to issue guidance covering these behaviours.

The FCA maintains that accountability under the Senior Managers and Certification Regime remains unchanged: delegating decisions to algorithms does not dilute liability. This must be translated into rules for autonomous payments, including which entity is accountable when an AI agent initiates a transaction and how liability is shared across interacting agents.

Regulators will need to determine liability, and firms will need systems that make accountability traceable and enforceable.

The convergence of agentic AI and stablecoin payments plays to the UK’s strengths in fintech and AI. While the US and China lead, the UK remains a credible “best of the rest”. Stanford’s HAI Global AI Vibrancy Tool ranks the UK fifth globally, while The Observer’s Global AI Index places it fourth, highlighting strengths in R&D, education, and governance. Google DeepMind and Stability AI are both headquartered in the UK.

Realising this potential will depend on enablers such as smart data schemes, secure digital identity, and interoperability standards.

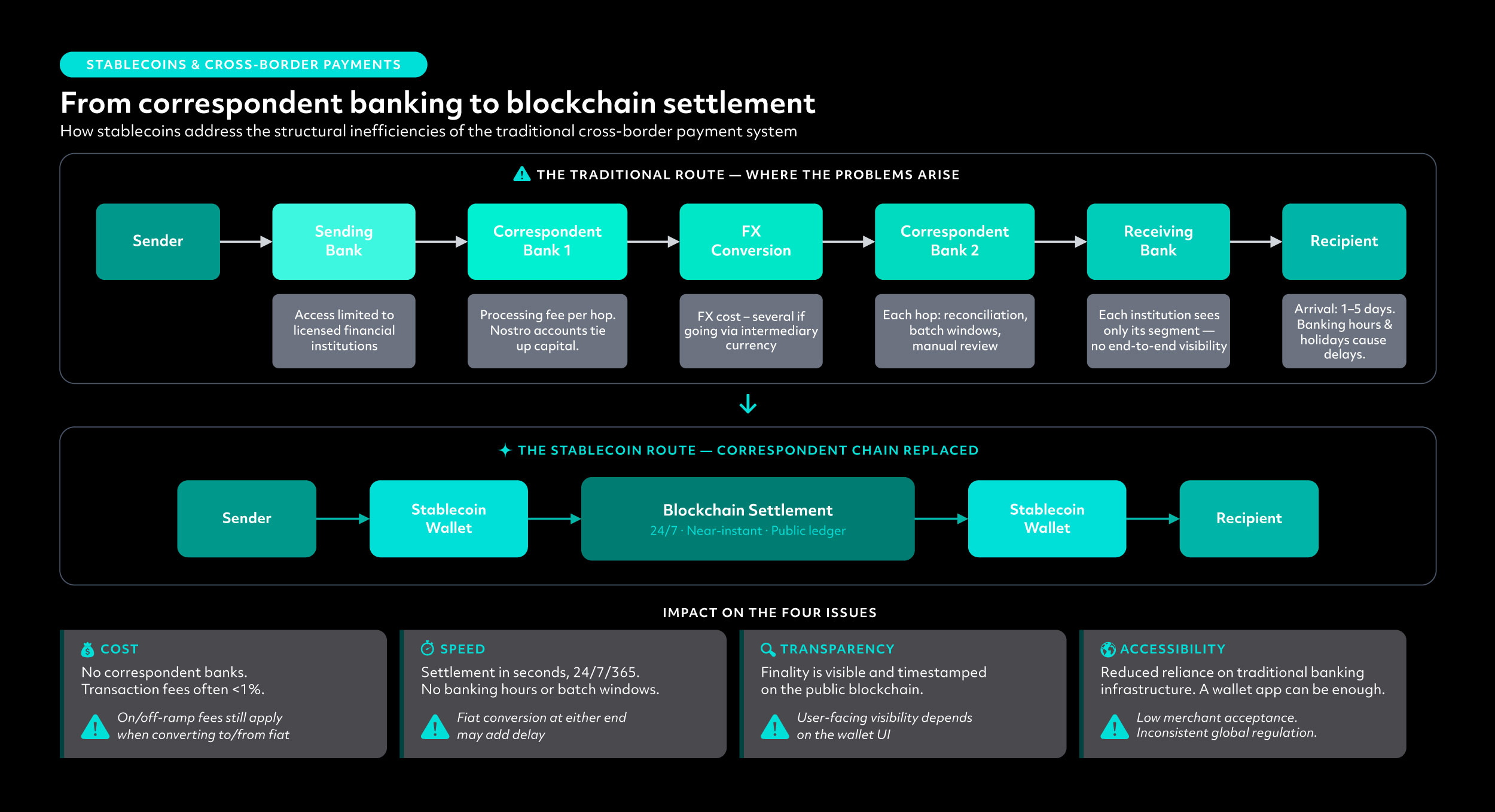

Cross-border payments are among the best-recognised applications of stablecoins. By replacing the correspondent banking system with blockchain technology, stablecoins offer significant improvements in cost, speed, transparency, and accessibility.

6.49%

$17.9tn

2-5 business days

In 2020, the G20 prioritised faster, cheaper, more transparent, and more accessible cross-border payments. The Financial Stability Board set quantitative targets in 2021, to be met by 2027 (see table below).

A December 2025 Bank for International Settlements report found only modest progress, with targets unlikely to be met on time. Many issues stem from the correspondent banking network.

Stablecoins offer a direct alternative. Instead of routing through intermediaries, payments settle on-chain, transferring value directly with finality.

A KPMG whitepaper finds that settlement times can fall from days to seconds or minutes, with costs reduced by over 99%. Lower pre-funding requirements also free up trapped capital. By removing intermediary “hops”, stablecoins improve all four G20 target areas:

Area | Target (by end of 2027, for remittance costs by end of 2030) |

|---|---|

Cost | Retail: Global average no more than 1% and no corridors with costs higher than 3% for. Remittances: Global average no more than 3% for USD 200 remittance, no corridors with costs higher than 5% |

Speed | 75% of transactions providers to be credited to the recipient within one hour upon initiation and the rest within one business day |

Transparency | All payment services providers to publish a minimum defined list of information |

Accessibility | Wholesale: Minimum of one option per payment corridor for sending/receiving wholesale cross-border payments. Retail: All end users have at least one option for sending or receiving cross-border payments. Remittances: More than 90% have access to electronic remittances. |

Source: Financial Stability Board (2021)

Payments Intelligence

There are two components to transparency in the context of cross-border payments: one is an understanding of how much a transaction will cost and how long it will take prior to initiating the payment; the other is the ability to monitor the status of a transaction once it has been initiated.

Stablecoin transactions are auditable in real time by authorised participants. On public blockchains, this auditability is universal; on permissioned networks, it is limited to credentialed parties. In either case, the blockchain provides a timestamped, immutable record of settlement, a marked improvement to the opacity of the correspondent banking chain. This level of transparency will be of increasing value given the direction of travel in regulatory reporting and financial crime compliance.

The retreat of correspondent banking from lower-volume and higher-risk corridors has reduced access to cross-border payments. Stablecoins address this by enabling direct, on-chain transfers without reliance on intermediary banks.

While costs vary by network, stablecoin transactions are typically 0.5% to 1% of value. Even with on- and off-ramp fees, they remain cheaper than traditional rails. Fees are also largely fixed, meaning larger transfers benefit most.

Adoption is most visible in high-inflation economies such as Argentina, Venezuela and Turkey, where stablecoins are used to preserve value and transact outside unstable local systems.

Although accessing wallets and exchanges introduces some friction, stablecoins often remain more accessible than legacy cross-border infrastructure.

Trade finance remains one of the most paper-dependent, friction-laden processes in global commerce. Stablecoins, combined with smart contracts and blockchain-native settlement rails, offer a structural response: programmable, atomic payment that can replace the slow, intermediary-heavy instruments that continue to cause friction in documentary trade.

$2.5tn

40%

$24.4tn

Trade finance underpins global commerce, yet its infrastructure remains largely unchanged. The global trade finance gap reached $2.5 trillion in 2025, up from $1.5 trillion in 2018, according to the Asian Development Bank. While capital constraints contribute, fragmented documentation, slow settlement, opaque counterparty chains, and reliance on paper processes are equally significant.

Traditional trade finance is operationally intensive. A single letter of credit can involve dozens of documents across multiple intermediaries, each maintaining separate records and verification processes. Bills of lading, invoices, inspection certificates, and insurance policies must be manually exchanged and reconciled, creating delays, costs, and fraud risks such as duplicate financing.

Distributed ledger technology has long been proposed as a solution. Platforms such as Contour digitise letters of credit on shared networks, reducing processing times from days to hours through a single, shared record. Backed by banks including HSBC, Standard Chartered, Citi, and BNP Paribas, these initiatives demonstrate the feasibility of blockchain-based trade finance. However, settlement has typically remained in fiat via traditional rails.

Stablecoins provide the missing settlement layer. Smart contracts define payment conditions, while stablecoins enable atomic, intermediary-free settlement. A stablecoin-funded escrow that releases payment automatically upon verified delivery replicates the function of a letter of credit with far lower operational overhead.

The scale and growth of global trade highlight the size of the settlement opportunity, where more efficient infrastructure, such as stablecoins, can reduce friction.

Rising interest in technologies such as DLT and AI reflects growing institutional momentum behind modernising trade finance infrastructure.

Stablecoins apply to both documentary trade and supply chain finance, though in different ways. In documentary trade, they act as escrow, released against verified shipping conditions. In supply chain finance, they are the disbursement instrument, providing working capital against approved invoices.

Early deployments are beginning to validate this model. In February 2026, Unloq completed its first live trade financing deal for Singaporean supplier Chemtank using XUSD, a US dollar stablecoin issued by StraitsX. Executed on Unloq’s SC+ platform, the transaction combined documentation and payment in a single blockchain workflow, enabling faster settlement while preserving buyer payment terms.

Market interest is rising. The 2026 Thomson Reuters Institute Global Trade Report, surveying 225 professionals, found 40% are exploring technologies such as AI and blockchain, up from 6% in 2024. While AI is a key driver, growing pilot activity suggests genuine institutional demand for blockchain-based settlement.

Challenges remain. Regulatory frameworks have yet to fully recognise digitised trade documents, leaving questions around legal enforceability and cross-border validity. Interoperability between DLT platforms, stablecoin networks, and legacy systems is another barrier. Scaling stablecoin-based trade settlement will require coordinated progress across regulators, industry bodies, and technology providers.

Stablecoin adoption among retail users and merchants is accelerating globally, driven by the promise of cheaper, faster settlement and access to dollar-denominated value in underserved markets.

125%

$187bn

#1

Stablecoin adoption is strongest where traditional finance falls short, particularly in Latin America, Sub-Saharan Africa, and South-East Asia, where inflation, currency instability, and limited banking access persist.

Remittances are a major driver: the World Bank estimates average costs at 6.49% in Q1 2025, over twice the United Nations target of 3%.

Crypto use is rising quickly, with retail transactions up 125% year-on-year in 2025. In Sub-Saharan Africa, stablecoins make up around 43% of volume, supporting cheaper cross-border payments and broader financial inclusion.

For merchants, stablecoins are primarily about cost. Card payments carry layered fees, with US merchants paying $187 billion in 2024. Stablecoins could bypass this model via on-chain settlement, reducing costs.

Visa now supports 130+ stablecoin-linked card programmes across 40+ countries, enabling spending from stablecoin wallets without changing checkout.

It also launched USDC settlement in December 2025, allowing partners to settle on Solana rather than fiat. Early participants include Cross River Bank and Lead Bank. Stablecoin settlement is scaling globally, with volumes exceeding a $3.5 billion annualised run rate, and pilots extending to payouts for gig workers and creators.

Mastercard enables stablecoin spending at over 150 million merchants through partnerships with platforms such as MetaMask, Crypto.com, OKX, and Kraken. Users can link wallets to Mastercard-branded cards and spend without any changes to merchant infrastructure. It also supports stablecoin payouts, which is particularly relevant for cross-border freelancers and creators facing high costs and delays on traditional rails.

PayPal launched PYUSD in 2023, a fully reserved dollar stablecoin issued by Paxos. It can be used across PayPal checkout, Venmo, wallets, exchanges, and multiple blockchains. By March 2026, PYUSD had expanded to 70 markets, enabling merchants to access funds within minutes rather than days. With more than 430 million active accounts and around 36 million merchants, PayPal provides a significant distribution channel for stablecoin adoption.

Stripe’s strategy is more merchant-focused. Its $1.1 billion acquisition of Bridge in 2024 strengthened its infrastructure, and Stablecoin Financial Accounts, now in preview across 101 countries, allow businesses to hold balances in stablecoins. While Stripe has supported stablecoin payments since 2024, these were initially converted into USD; newer products enable merchants to retain stablecoin exposure directly.

This allows merchants to hold balances, accept payments, and settle in stablecoins within Stripe’s existing stack, creating a low-friction route to adoption for businesses already using Stripe. In June 2025, Stripe expanded its partnership with Shopify, enabling merchants in 34 countries to accept USD Coin.

Research from the Financial Conduct Authority shows usage remains concentrated in crypto markets. Of those who had bought stablecoins, 50% did so to trade other cryptoassets.

Other use cases have declined. Buying goods and services fell from 27% to 17% in 2025, financial product purchases dropped to 15%, and transfers to friends and family to 11%.

Adoption may still grow. Over a third of respondents cited lack of knowledge as a barrier, and 16% could not define stablecoins.

Among those aware of crypto but not users, 29% said Financial Conduct Authority regulation would increase their likelihood of adoption, with Financial Services Compensation Scheme protection also a key factor (25%).

Worldpay (is now Global Payments) is embedding stablecoins across acquiring and payouts through partnerships with Zero Hash and BVNK. Merchants can receive card settlement in stablecoins such as USDC, enabling 24/7 near-real-time settlement while reducing FX and treasury friction, with complexity fully abstracted.

It is also enabling near-instant global payouts across 180+ markets via BVNK, integrated into its existing platform and without requiring clients to handle digital assets.

Together, these capabilities extend stablecoin rails across both settlement and disbursements, improving speed, cost efficiency, and reach.

HM Treasury, the Bank of England, and the FCA have published a range of discussion papers, consultation papers, and policy papers on stablecoins in the past year. This section sets out the current state of UK stablecoin regulation and what to expect in the coming year.

7

Q4 2026

£10m

The UK’s stablecoin regulatory framework is taking shape but remains incomplete. The architecture is now broadly established across HM Treasury, the Financial Conduct Authority, and the Bank of England, each with a distinct but interlocking role. However, the final regulatory framework is pending, and several significant policy questions remain open.

The foundation is the Financial Services and Markets Act 2023, which empowers HM Treasury to bring stablecoin activities into scope. This is being implemented through the Financial Services and Markets Act 2000 (Regulated Activities and Miscellaneous Provisions) (Cryptoassets) Order 2025, finalised in December 2025.

The Order introduces regulated activities for issuing qualifying stablecoins and safeguarding cryptoassets, requiring FCA authorisation. However, it does not extend the Payment Services Regulations 2017 to stablecoins. As a result, stablecoin payments remain outside the regulated payments framework, with no clear timeline for inclusion.

The UK distinguishes between systemic and non-systemic stablecoins. A stablecoin is deemed systemic if its widespread use in UK payments means disruption could threaten financial stability, as determined by HM Treasury with input from the Bank of England.

Systemic stablecoins fall under the Bank of England, while non-systemic issuers are regulated by the Financial Conduct Authority. A November 2025 consultation proposes that systemic issuers hold reserves in short-term UK government debt and non-interest-bearing deposits at the Bank.

Proposed holding limits of £20,000 for individuals and £10 million for businesses have drawn industry pushback, and the final position remains pending.

The FCA acknowledge that stablecoins are increasingly important in cryptoasset markets and could drive innovation in financial services, with a range of potential uses. As such, alongside consultations, the FCA have launched a stablecoins cohort in their regulatory sandbox and have begun conducting tests alongside four firms, to gain further insights into how stablecoins should be regulated. This complements the pre-existing Digital Securities Sandbox that the FCA and the Bank have been operating jointly, examining how stablecoins can be used as a settlement asset.

The UK government today passed the Financial Services and Markets Act 2000 (Cryptoassets) Regulations 2026 to establish a regulatory regime for cryptoassets and plans to modernise payments legislation, including stablecoin payments. The government aims to avoid unnecessary regulatory burdens for firms, especially those providing stablecoin payment services, while comprehensive payment services reforms are developed. Draft legislation has been published to clarify policy intentions, address industry feedback, and correct unintended consequences in the crypto regime, with further industry consultation planned. Payment services using UK-issued qualifying stablecoin (UKQS) will be consulted on for inclusion in regulated payments, with UKQS issuers required to meet FCA authorisation standards.

UKQS will be temporarily carved out from regulated activities of dealing and arranging in cryptoassets, but lending and borrowing involving UKQS will remain regulated to address consumer risks. Cross-border stablecoin payments may still face regulatory frictions, particularly for overseas-issued stablecoins, and these issues will be explored further with industry.

The government proposes clarifying the temporary settlement exclusion to ensure it does not apply to holding UKQS during payment services. Additional proposals include changes to the financial promotions regime, early implementation of stablecoin backing asset provisions, and correcting CSD nominee company exemptions for cryptoasset safeguarding.

HM Treasury will consult with industry on these proposals, with a deadline for feedback set for 22 May 2026. Final rules are expected in H2 2026.

In this discussion, Lisa Lee Lewis, partner at Addleshaw Goddard and current lead of the Digital Currencies Working Group, and Natalie Lewis, partner at Travers Smith, explore the evolving role of stablecoins with Riccardo Tordera-Ricchi, VP of policy at The Payments Association. They unpack key regulatory challenges, competitiveness concerns for the UK, and the growing importance of use cases such as cross-border payments, tokenised markets, and emerging technologies, such as AI-driven agentic commerce.

Four key dates define entry to the UK cryptoassets regime:

Firms that fail to apply by the closing date risk being unable to take on new clients if their application is not approved by commencement. While timelines may appear generous, preparation is complex, particularly for firms new to FCA regulation, and early action is critical.

The challenge can be distilled into seven core pillars:

Progress across these pillars is essential for timely authorisation and long-term viability.

The Digital Currencies Working Group aims to develop a programme of thought-leadership content that educates and makes recommendations to the industry on a range of topics from the different types of digital assets and regulatory frameworks to wider ecosystem design.

Please fill out the form to indicate your interest in receiving more information about The Payments Association’s Digital Currencies Working Group. A member of our Project Team will be in touch with you shortly.

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.

You need to be logged in to do this!