4 TYPES OF COMPLEX ATO YOU NEED TO KNOW ABOUT

– Introduction

– Deep fakes

– SIM swap scams

– SMS OTP fraud

– Session hijacking via RATs

– Originality is key

– Introduction

– Deep fakes

– SIM swap scams

– SMS OTP fraud

– Session hijacking via RATs

– Originality is key

– Introduction

– Reducing false positives and negatives

– Know Your User

– Automating fraud response

– Conclusion

A summary of the findings of Yobota’s recent survey into how banking and financial services firms responded to covid-19 in terms of digital transformation and technology uptake.

Cash payments have been in decline in the UK over the past decade, with contactless payment becoming the popular choice. But with the limit on contactless transactions set to double to £100 by the end of the year, what chance does cash stand? In this new article from Ingenico’s Contactless 2021 series, Blair Stalker examines the impact of the change and the #SCA mitigations against an increase in fraud.

Episode Six is transforming the buy now, pay later (BNPL) landscape, by putting control in the hands of card issuers versus the acquirer or other third parties. For the first time, issuers can implement changes at the account level in real-time. To understand why this is important, we take a look at the interest in BNPL and how it works.

As we have noted in the past, federal regulation of the digital asset/cryptocurrency/DeFi community is evolving and there are many perspectives on what direction it should take. For instance, earlier this week, the House Democratic leadership and a group of moderate House Democrats agreed to a compromise that would prevent the House of Representatives from amending the Senate-passed “Infrastructure Investment and Jobs Act” (H.R. 3684), thereby preserving the bill’s provisions expanding the definition of “broker” under the Internal Revenue Code to apply to various digital asset market participants.

The Federal Deposit Insurance Corporation (FDIC) has issued a “Request for Information and Comment on Digital Assets” (RFI) to learn more about the “novel and unique considerations related to digital assets….[g]iven that banks are increasingly exploring the emerging digital asset ecosystem.” A key theme of the RFI is the development of a framework to promote “responsible innovation.”

One of the most discussed subjects in the industry today is how digital has transformed banking and financial services. And of course this has been even further amplified by the Coronavirus pandemic.

Ordo and Certua are integrating Ordo’s open banking payments capability with Certua’s embedded finance platform to better serve the needs of businesses and their end customers with novel financial services.

Localise, globalise and optimise your business with our unique range of payment and banking solutions. Reduce online fraud, increase conversions and drive business growth across the world.

On 22 June 2021, HM Treasury (HMT) confirmed that it will take forward legislation to introduce a gateway for the approval of financial promotions of unauthorised persons. Once the gateway is in place, only firms which have successfully applied to the FCA to approve financial promotions will be permitted to approve the financial promotions of unauthorised persons.

Compliance with regulatory requirements regarding the approval of financial promotions has been a recent supervisory concern for the FCA, especially in circumstances where the products being marketed are complex and targeted at the retail market, and the FCA has issued a number of letters and publications setting out concerns and guidance for authorised firms approving financial promotions

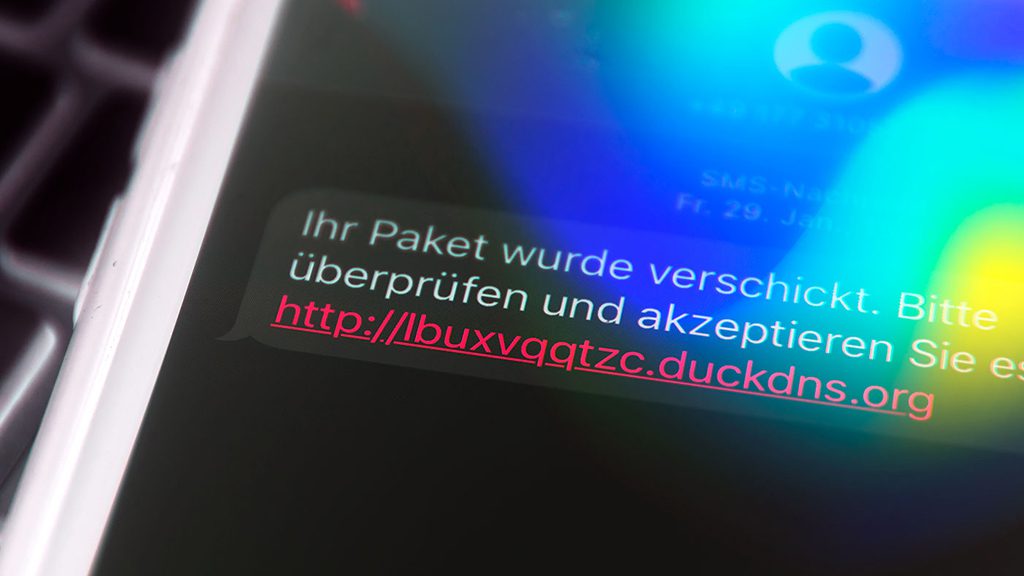

The distribution of this banking trojan is one of its main strengths since the use of text messages impersonating delivery services companies is a really good idea for deceiving the victims and getting them to install the malicious application.

The mandatory geolocation in banking transactions came into force in Mexico as of March 23, 2021

For e-commerce and contact centre payments, cards have been the only payment option but are costly to businesses and increasingly difficult to use for consumers. Open banking regulation and technologies has created new options for businesses

Manchester FinTech Accesspay has made three senior hires as part of ambitious growth plans to double headcount in 2021.

We are extremely proud to announce our expansion to the United States with Paysafe Group & Mastercard as a partner of their Digital Doors program.

SimplyPayMe will from now on empower & enable American SMBs by allowing them flexibility in getting paid and the ease of running their business, all within one single application.

We are also working with banks and digital partners to help them serve their SMBs better, giving them the option to offer SimplyPayMe as a value-added service or as a white label.

Demand for cash injections from alternative finance providers shows no signs of abating, as such, lenders must embrace innovation to improve their business finance offering. Read @Currencycloud’s blog to discover how APIs are the future of invoice finance. https://bit.ly/3wEqwCr

Ordo wins Open Banking Expo #PoweroftheNetwork Award 2021!

This 2021 report summarises a survey taken by over 200 payments professionals across the banking, financial, fintech and corporate sectors. It provides an overview of the payments landscape, explores the key findings, and provides insight into the various elements that had an impact on failed payments throughout 2020.

PSD2 is a hot topic for the UK market. How can we tackle it?

We take a look at challenges and solutions for the UK payment ecosystem in complying with PSD2 requirements.

With PSD2 now live in most European countries, being 5 months past the December 31, 2020 deadline, the UK is next, as the deadline for March 2022 is approaching. In order for the cardholder and merchant to properly adopt additional authentication without abandoning the transaction, the main focus is eliminating as much friction as possible. Testing data¹ from merchants such as Amazon, Google and Microsoft has shown that although Strong Customer Authentication has been enabled for most of the UK ecosystem, it is still grappling with several issues. Examples of this are relying on Risk Based Authentication for lower challenge rates, issuer readiness on latest protocols, issuer latency and lastly confusion on what exemptions to properly utilize.

– Introduction

– Poor hygiene & Persistent threats – ‘perfect storm’ of online fraud

– Customers expect Banks to Know Your User

– Fraud Fighting Collective – Fraud Fusion Centers

– Overwhelmed with Alerts, Automation is key

– Clear ‘risk calculation’ – Frictionless First

– No silver bullet – but there are best practices

– Introduction

– What is BionicID™ analysis best suited for?

– Does BionicID™ data collection or analysis impact the user experience?

– Does BionicID™ data collection/analysis comply with SCA/PSD2?

– Does BionicID™ data collection/analysis (behavioral biometric digital identity) comply with GDPR?

– Introduction

– Physical vs. Behavioral Biometrics

– What is a BionicID™

– What makes Revelock’s BionicID™ solution unique in fraud prevention?

– What makes Revelock’s BionicID™ more accurate than other behavioral biometric solutions?

Banking as a Service (BaaS) refers to the services and tools that allow financial institutions to adapt to the current digital banking shift. BaaS providers are the ones that build the web and mobile applications for these institutions so that customers may access their accounts digitally. But has this environment changed since the release of PSD2? Absolutely – let’s take a look.

It is becoming ever more apparent that ‘Big Tech’ players are looking to service a slice of the financial services sector. What does this mean for the industry and the banks that service it today?

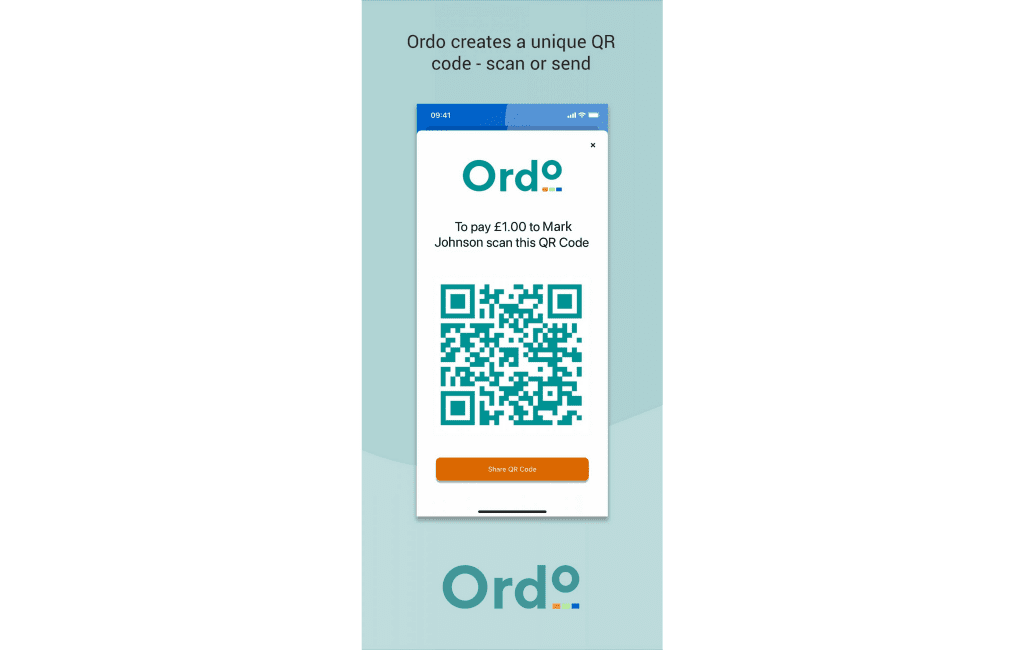

Ordo is making payments right – providing Open Banking enabled solutions that mean businesses can securely and simply collect payments from their customers, instantly. No hidden fees. No hassle. No worries.

This guide takes you through some of the innovations and trends taking place in payments, including how different sectors responded to the challenges of Covid-19; why business-to-business payments are ripe for innovation and changes in regulatory landscape that will impact payments in the future.

Okay is mainly concerned about security and Strong Customer Authentication. However, that doesn’t prevent us from taking part in industry conferences or being a member of industry groups. In this blog, we take a look at a few of the hot topics that have been on the discussion table over the past year, with some insight as to where they may be headed.

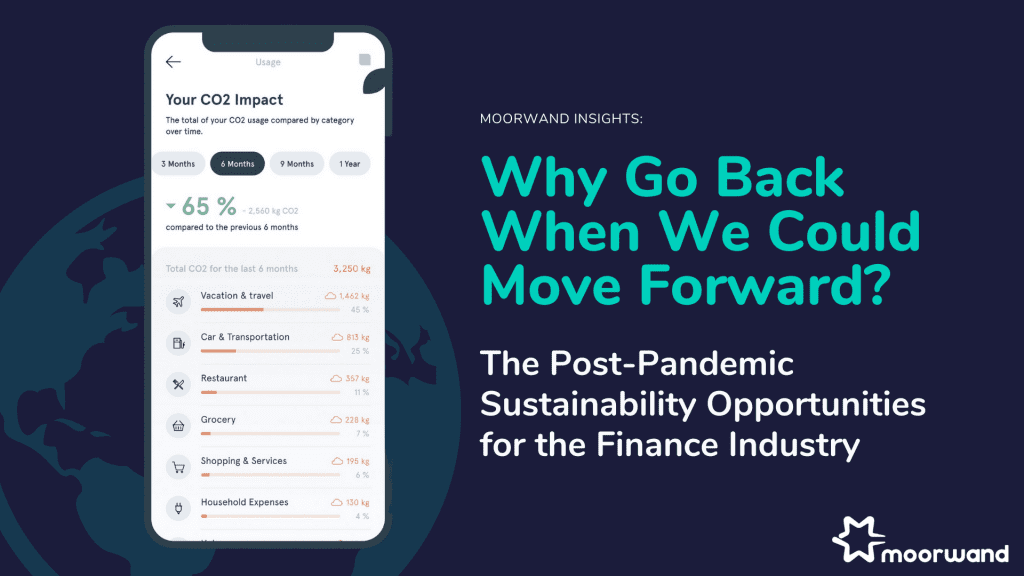

It is important to remember that even before COVID-19, the planet was in a state of emergency. So with the finance industry focusing on recovery, resilience, and longevity as we come out of lockdown, should sustainability and the environment be top of the agenda as well?

In this article, we break down the post-pandemic sustainability opportunities for the finance industry and speak to our partner ecolytiq about why the best time to focus on climate change was yesterday.

Award-winning Banking-as-a-Service platform, Contis, is pleased to announce the appointment of Andy Lyons as Managing Director of Banking Solutions. Andy brings a wealth of experience in retail and corporate banking to boost Contis’ banking division and cement its position as the European leader in Banking-as-a-Service (BaaS).

Wealthify is teaming up with Tink for open banking powered payments.

In order to receive 3D Secure messages, process said messages, and authenticate card users, issuing banks must deploy Access Control Servers (ACS). To ensure that transaction integrity is never compromised, the Okay software works in parallel to prevent attacks and protect user information during confidential transactions. The process looks a little something like this:

Sam Head of Currencycloud shares his top 3 recommendations on what to look for in the right partner for your strategic, long-term journey to borderless transactions.

He covers the pros and cons on a bundled solution, the idea of future proofing your partner choices for business growth ambitions, the important considerations involved in the costs as well as owning the customer experience.

Transact365 is more than a gateway. It is a methodology platform that has been designed to operate as a technical consultancy business, lending our years of experience and knowledge whilst building on new and exciting technology that can zero out fraud.

Monneo, virtual IBAN and eCommerce bank account provider, has unveiled an innovative new look logo and website design this week, as the brand expands across Europe and beyond.

Top UK fintech pitches a 100% recyclable card product – that even picks up on antennae.

Embedded finance is making waves in the lending industry by challenging the status quo – giving rise to a new breed of Fintech provider: the Lendtech.

While the goal of Lendtechs is not necessarily to compete directly with incumbent financial institutions on their turf, embedded finance – and subsequent embedded lending – has dented their market share. These legacy providers now have a choice: stick to what they know or embrace the opportunities embedded finance creates for their products and services by working in partnership with Lendtechs.

In this blog post Jack Wilson, Head of Policy & Regulatory affairs at TrueLayer, examines the security and protections provided by open banking when buying online.

A major study reveals how banks and building societies are responding to the post-pandemic world.

A world where digital commerce has become the default and customers expect their services, including payment processing, to be real-time and traceable 24/7.

With more and more fintech start-ups cropping up with shiny new card programmes, it’d be all too easy to assume launching one yourself would be counterproductive. But owning a card programme comes with a whole host of benefits, regardless of the competition, and it’s never been easier to launch one. Discover the benefits of starting a card programme for your customers in Moorwand’s payment guide.

Thames Technology is delighted to launch its new ELEMETAL range of high-quality metal payment cards, offering the ultimate in style and sophistication for premium banking customers.

The Bank of England and the UK Treasury have announced a Central Bank Digital Currency (CBDC) Taskforce to coordinate the exploration of a potential British CBDC. But how could a digital Pound actually work? As it happens, this is something that Consult Hyperion knows rather a lot about. Apart from our work on the first British central bank digital currency (Mondex) back in the 1990s, our work on the first population-scale mobile money scheme (M-PESA) in the 2000s and our work on the most transformational contactless payment roll-out (Transport for London) in the 2010s, our practical experience across implementation platforms means that we understand the architectural options better than anyone.

Vista Bank Group in West Africa has chosen Radar Payments for its processing activities and to drive digital payment adoption in the region. The solution will include SmartVista’s card issuance and lifecycle management, payment switching, ATM and point-of-sales management as well as providing digital channels such as mobile banking and e-wallet; personalised to both retail and corporate clients.

The Wirecard scandal 2020 shook the Fintech community and created a lot of questions for the industry regulators in Germany – thousands of people lost their jobs and client operations all over the world were disrupted.

But as we all know, in the middle of difficulty there is always lies opportunity. So we decided to act – this is a blog article that tells a story of how Gain The Lead came to be.

Tink and American Express are partnering to improve the onboarding process for prospective card members in Europe, by using open banking technology to instantly verify identity, income and account information.

In this blog, fscom’s Dipesh Patel discusses the Temporary Permissions Regime (TPR) for EEA firms, the communication of timeframes from the FCA and the proposed changes to the approach document in CP21/3.

In this blog, Blue Train Marketing delve into the transformation of video marketing, its increase in popularity and the pandemics impact. They reveal some tips and tricks on how to improve your video content whilst restrictions are still in place.

fscom’s Greg James looks at the proposed changes to strong customer authentication (SCA); one of the most contentious regulatory developments introduced by the second Payment Services Directive (PSD2). Greg breaks down the changes into those that will generate the most conversation and those that are simply explicit confirmations in existing guidance.