Unleashing the potential of Open Banking

This report sets out to clarify the potential of the open banking opportunity, identify what might hamper its realisation, and recommend what the community can do to unleash it.

This report sets out to clarify the potential of the open banking opportunity, identify what might hamper its realisation, and recommend what the community can do to unleash it.

This guide explains what identification and authentication are, presenting an overview of the technologies that can help you. It also arms you with key questions to put to suppliers when determining which solutions will meet your needs best.

This report emphasises the seismic change that COVID-19 will have on how we use payments to live, work and shop and the effect this will have on the shape and size of the payments industry.

Your one-stop guide by Modulr to making sense of the bright new future that’s just around the corner. This eBook is intended for businesses across lending, FinTech, employment services, payroll, travel, accounting and many more services.

The Payments Association’s Project Regulator brings our members together to consider regulatory issues, provide feedback to the regulators and influence change.

This report discusses the fight against fraud and financial crime. It makes the case for increased investment in technology systems and greater centralisation and consolidation of department responsibilities. The content of this report draws on discussions at a workshop organised by the Payments Association.

This report provides a detailed summary of fraud up to the present, the various solutions that have been developed to tackle it, an explanation of the innovative new technologies being utilised against fraudsters, and how fraud is expected to evolve in the future.

The guide describes an AML risk assessment and why is it necessary. It describes an ‘EnterpriseWide Risk Assessment (EWRA)’ and a ‘Customer Risk Assessment (CRA)’. It then makes the case for why and how often a risk assessment should be conducted.

The first edition of the Payments Association’s Guide to Payment Account Providers. This is the first time that anyone in the UK has invited all providers to contribute to an independent, objective summary of providers.

This report covers realtime bank payments and card payments as well as transaction data. It has been produced based on discussions from a workshop that was arranged by the Payments Association.

A summary-level guide, based on internal data, to current salary levels in UK FinTech

The Payments Association, in conjunction with the European Women in Payments Network (EWPN) undertook this project to: 1) set a baseline in gender equity issues that will

allow for the measurement of change over time; 2) understand the social and structural barriers that inhibit change, and 3) make recommendations

This report discusses how innovation and regulation within lending and credit will impact the payments industry and consumers. It has been produced based on discussions from a workshop that was arranged by the Payments Association.

A White Paper on the impact of Strong Customer Authentication strategies on the experience of payments users and what this means for the industry.

This document was created to assist the industry in implementing the requirements of proportionality, objectivity and nondiscrimination (POND) set out in the Payment Services Regulation 2017 (PSRs), Regulation 105.

In this report SWIFT examines the trends observed over the course of 2018 and 2019, showcasing how both business and security information can utilise tell-tell signs, and become key in detecting and responding to attempted attacks.

This report discusses data markets, value cycles, and evolving business models around data monetisation. It has been produced based on discussions from a workshop that was arranged by the Payments Association.

The report explores the disruptive innovations and technologies that are or will be relevant in shaping and managing digital businesses, the impact that these innovations will have upon the payments ecosystem, and the social and commercial drivers which will enable these innovations to flourish. It has been produced based on discussions from a workshop that was arranged by the Payments Association.

A whitepaper that details the anti-money laundering considerations in EEA jurisdictions

This report explores the disruptive innovations and technologies that are or will be relevant in shaping international trade finance and global commerce, the impact that these innovations will have upon the payments ecosystem, and the social and commercial drivers which will enable these innovations to flourish. It has been produced based on discussions from a workshop that was arranged by the Payments Association.

9 industry experts share their latest and greatest insights

Analysis of payments-related financial crime and how to minimise its impact on the UK In association with Barclays, Refinitiv and a syndicate of Payments Association members

This report sets out the contribution the financial sector makes, some of the challenges the sector faces, and the key steps to enable financial services to support UK growth and promote world-class financial services that will deliver great customer outcomes.

An in-depth analysis of today’s dynamic payments environment

An in-depth analysis of the development of new payments ecosystems, which are opening new horizons in payments and transaction banking.

This paper explores some of the challenges that the industry faces if it is to unlock the potential of API technology

A research report on the competitiveness and effectiveness of the personal current account market

Consumer demand for fast, frictionless, and low-cost international transactions has necessitated an increasingly global payments landscape. This shift presents many opportunities, but also many challenges, particularly for small and medium-sized merchants that want to expand into new territories.

Our research reveals the pain points for merchants that trade internationally.

Consumer experience is the new competitive differentiator for prepaid programs

This report by Rich Wagner, CEO and founder APS and former Chairman of the The Payments Association, has been devised with insights from the Payments Association’s members, which outlines our consolidated views on how to build a payments system that works for the banks – without excluding the increasingly influential alternative payment providers.

Is your business getting lost in the rapidly changing payments landscape?

Lost in Transaction is Volume One of a new independent research project conducted by Paysafe in conjunction with Loudhouse, a London-based research agency.

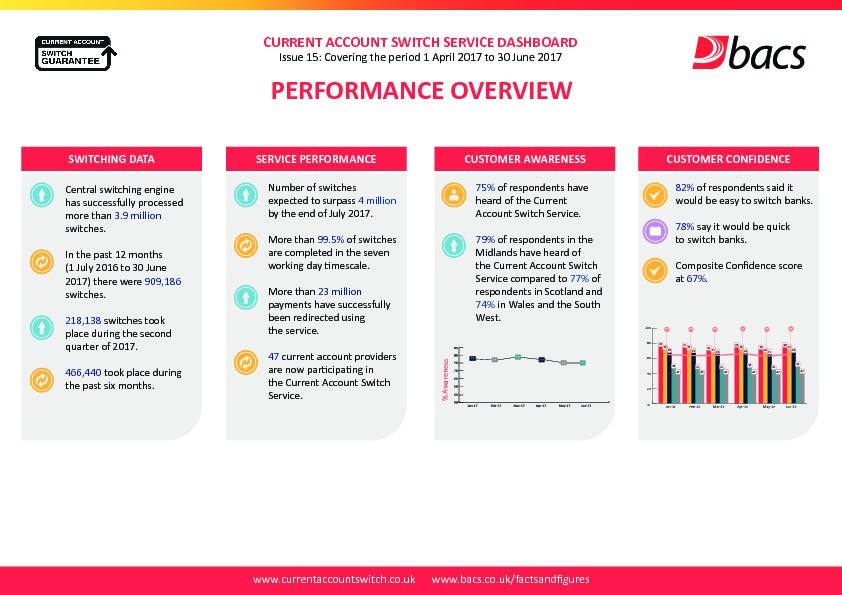

CURRENT ACCOUNT SWITCH SERVICE DASHBOARD – Issue 15: Covering the period 1 April 2017 to 30 June 2017

This paper explores how you can potentially use payments services to compete as well as comply.