Evolving money laundering risks for EMIs: Insights from the 2025 NRA

Q3’s updated UK NRA reclassifies EMIs as high risk for ML and TF, prompting debate across the sector on compliance, innovation and proportionality.

Q3’s updated UK NRA reclassifies EMIs as high risk for ML and TF, prompting debate across the sector on compliance, innovation and proportionality.

AI is transforming compliance in financial services, offering efficiency gains while introducing new risks that demand robust governance.

Operational resilience is key for financial firms amid rapid tech advances, enabling innovation but increasing cyber threats, regulations, and risks.

The new Reimbursement Claims Management System (RCMS) aims to simplify APP fraud claim processing, enhance PSP cooperation, and ensure adherence to updated compliance standards

Swift’s updated CSP and IAF are essential for ensuring robust cybersecurity and compliance across the global banking community.

Enhancing the FCA’s complaints reporting process aims to swiftly identify consumer harm, improve regulatory compliance, and streamline operations for financial firms.

In 2021, the Financial Conduct Authority (FCA) Business Plan made clear its intent to apply a more intensive assessment with greater scrutiny of financial information and business models. This is being particularly felt in the payments space.

As the regulatory landscape continues to evolve, is innovation at risk in the fintech space?

The UK’s financial watchdog has warned that e-money firms must undertake a “significant shift in culture and behaviour” if it is to comply with the new Consumer Duty rules, due to come into force in July.

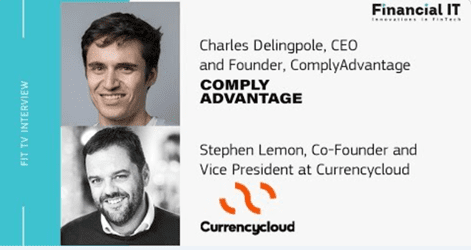

Check out this recent Financial IT interview featuring Currencycloud’s Co-Founder & VP Strategic Partnerships, Stephen Lemon and ComplyAdvantage’s Founder and CEO Charles Delingpole as they discuss all things Fintech.

Watch the interview here: https://www.youtube.com/watch?v=XG9JlvilL10

The deadline for the 6th Anti-Money Laundering Directive (6AMLD) is rapidly approaching — currently, it is set for June 3rd. That said, the question of whether 6AMLD’s measures are clear and robust enough to combat the ever-growing problem of money laundering remains.

Marius Galdikas, CEO at ConnectPay, has taken the opportunity to overview how the AML regulatory framework has changed over the years, starting with the first Anti-Money Laundering Directive. He has also outlined what to expect in the near future, as some challenges regulators have yet to outline as possible threats.

In order to receive 3D Secure messages, process said messages, and authenticate card users, issuing banks must deploy Access Control Servers (ACS). To ensure that transaction integrity is never compromised, the Okay software works in parallel to prevent attacks and protect user information during confidential transactions. The process looks a little something like this:

With the advent of passwords at MIT 60 years ago, Gerhard Oosthuizen Entersekt CTO, contends that it’s time that we replace passwords with more robust technologies.

With regulators increasing their focus on compliance, pressure on financial institutions of all sizes to have compliant open APIs is growing. To help simplify the delivery of high-performing APIs, Ozone has launched the Open Finance Hub.

Compliance, requirements, deadlines, oh my! By now you should have a comprehensive overview of what to be aware of as PSP. As such, it is time to wrap up the topic of SCA compliance. In this article, we cover how Okay uses security evaluations to fine-tune our product as well as how we can help you meet SCA PSD2 RTS compliance standards.

Compliance. A scary term for any payment service provider (PSP) in a world of increasingly stricter regulations and requirements. To make it a little less scary, we are opening the PSD2 RTS Compliance door to extract some key points of interest. Read on for the fundamental requirements PSPs should be aware of if issuing cards or e-money payments and why said requirements are necessary.

One of the more vexing problems of the modern age when it comes to international business is that regulatory regimes often do not keep pace with technological innovation.

Nonetheless, novel solutions to B2B cross-border business have emerged in the form of virtual IBANs, financial instruments that drive the innovation economy and enable new, powerful business models.

Here we have outlined three ways that virtual IBANs are transforming the way companies do business locally and abroad:

When it comes to digital banking and compliance, robust KYC practices not only prevent fraud and financial losses but also strengthen a firm’s ability to conduct business with confidence.

This is typically because of the four key elements of strong KYC practices that make sure firms know who they’re doing business with and what to expect from that relationship.

We’ve identified the four essential elements of effective compliance in KYC practices for digital banking in order to show you how they help improve the competitiveness of businesses of any size or scale:

The year 2020 saw many of the innovations and prognostications of analysts come true as contactless payments and digital banking solutions drove the field of Fintech innovations. Looking ahead, however, 2021 could be the year that consolidates much of this growth and prepares the economy for the next stage of digitization.

We at Monneo have identified five major trends that we think are driving the Fintech innovations in digital banking, in 2021 and beyond:

The digital banking era is upending traditional payment solutions and transforming the global financial industry in the process. And this is on both the corporate and consumer level with changes in payments solutions reaching into every facet of the international economy.

These innovations in digital banking are not only enabling increased efficiencies and expediting capital flows at a rate previously unthinkable but also are leading the way in changing the dynamic and level of depth of the business-customer relationship.

Okay has been running compliance audits since 2016. What did it look like back then compared to today? Are two channels for SCA really needed? This week we briefly explore the changing security environment of mobile phones related to identity verification.

The Fintech for Fintech’s Kani Payments, specialising in payment reconciliation and reporting has announced hitting £5 billion reconciliation milestone and the appointment of three senior hires.

W2, award winning global provider of regulatory compliance solutions today announced their partnership with market leading payments provider Contis to supply end-to-end KYC/AML processes for customer onboarding and ongoing monitoring.

The recipe for success in the e-commerce business is much the same as any other entrepreneurial endeavor except it comes with many opportunities for growth and leverage that physical businesses don’t have.

Online business may be the future of many markets, and for good reason. From scalability of immediately needed resources to cost-effective innovation and optimization, we have identified five key elements of success for e-commerce business in the modern age:

E-commerce businesses can’t put enough of a premium on online cybersecurity and protection against threats. Not only can malicious actors steal data and commit fraud, but they can also completely undermine a customer’s confidence in your business.

To avoid costly fraud and cyber threats, we’ve found five primary areas of focus that e-commerce businesses need to keep in mind as they move forward in the online market:

As part of a European Union mandate called the Revised Directive on Payment Services, or (PSD2), merchants operating in the EU economic zone must use payment service providers within the European Economic Area that offer what is known as strong customer authentication.

This is also sometimes referred to as the SCA requirement or the PSD2 compliance. In essence, this directive ensures that transactions occurring within the EU’s economic territories make use of multi-factor authentication in order to verify a buyer’s identity.

The promises of the European Union single market, while not full borne out in the reality of the business world, where the same are actually still far from the dream promised when it comes to the virtual single market. What does this mean?

In other words, the European Union might act as a single market when it comes to monetary issues and beyond, but the EU single digital market is hampered and its growth restricted by a myriad of factors including various compliance regimes and the logistical mastery needed to make it all work.

If your goal is to service the largest percentage of market users, respect must be given across all accessibility levels. But what is a reliable solution for non-smartphone users? In this post, we review our remote dial option as a reliable PSD2 SCA fallback.

We have spoken a lot about strong customer authentication (SCA) over the past year. However, the regulation has technically been in effect since mid-September of 2019. Now well into 2021, it is time for all European countries to fully enforce the updated SCA regulations. Let’s take a look at some of the deadlines.

One of the great innovations of the modern age is the ability of eCommerce to connect businesses, merchants, and consumers all across the world. Not only has this opened up new opportunities for businesses and consumers alike, but also it has expanded the realm of what is possible for small and medium enterprises on the global stage. And here we start with the interesting part of the current topic.

Over the last few years, Okay has gone through both security certifications and penetration testing. While they represent two uniquely different processes, each has greatly improved our product’s security, code quality and architecture. In this post, we discuss the importance of each, as well as what we’ve learned along the way.

What are some of the major forces driving the corporate banking digitization process? What are the factors and trends behind some of the most seismic moves in recent years in this otherwise quite conservative industry? What are the main key-topics we should have on our radar in order to stay ahead of our business competitors and be the first to learn what would be the next

“big thing”?

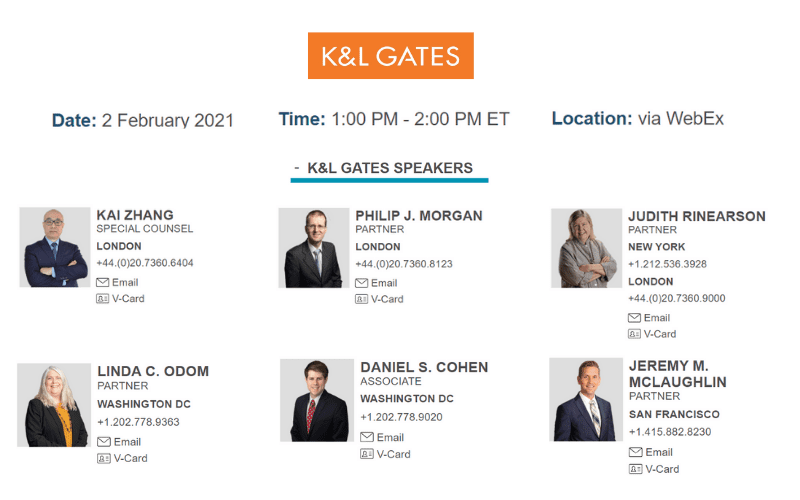

Join us for a cross pond webinar focusing on the enormous changes that are expected to impact payments in the US and UK featuring:

•In London, new K&L Gates Special Payments Counsel, Kai Zhang, and Partner, Philip Morgan.

•In New York, Partner and Global Fintech Co-Chair, Judie Rinearson.

•In Washington DC, Partner and Technology Law Specialist, Linda Odom, and Associate, Daniel Cohen.

•In San Francisco, Partner, Cryptocurrency and Fintech Lawyer, Jeremy McLaughlin.

Topics to be covered include:

•Expected changes to be implemented by the new US Democratic administration

•New leadership in the CFPB, SEC, OCC, and CFTC and what it means for banks and Fintechs

•UK and the implementation of Brexit with respect to payments and banking

•Anticipated changes in providing payment services to the UK and Europe

•The outlook for Fintech investment, Mergers and Acquisitions in the next 12 months on both sides of the pond

•What products and services are the winners and losers from these sweeping changes? Mobile apps? Traditional banking? Digital assets, stable coins and cryptocurrencies?

Miroslava Betinova, Head of Strategic Sales at PPS, discusses the trends we’ll see in the fintech industry this 2021.

The rise of digital banking has taken the traditional financial sector by surprise and for many good reasons. From pioneering the art of customer service online to using artificial intelligence to handle many of their operational tasks, digital banking is not just a glimpse of the future of finance. It is a peek into the future of the world of business itself.

– Introduction

– GDPR and behavioral biometrics – what can’t be seen, can’t be stolen

– PSD2: A smarter way of customer authentication

– SCA

– Malware

– Maintaining customer trust and safety

EML’s new FINLAB incubator has made its first investment in US FinTech disrupter Interchecks.

The London based E-Money solution for global citizens Privat 3 Money (P3) has selected leading anti-money laundering and intelligent compliance software provider Napier, to integrate enhanced transaction monitoring into the core P3 platform.

A personal account of the experience of being furloughed and 7 top tips to help come out the other side in a more positive place.