Going global: How e-commerce brands can scale smarter

Unlock global growth with smart localisation, seamless payments, and trusted partners, build customer-first experiences that convert across borders.

Unlock global growth with smart localisation, seamless payments, and trusted partners, build customer-first experiences that convert across borders.

The Payments Association has partnered with Nineteen Group to accelerate its growth while maintaining its independent brand, leadership, and mission to empower the payments community.

Explore how AI is transforming Fintech customer support, enhancing efficiency, enabling personalisation, and preserving essential human touch.

SMEs that modernise payments can unlock growth, improve cash flow and build trust—while those that delay risk revenue loss and reputational damage.

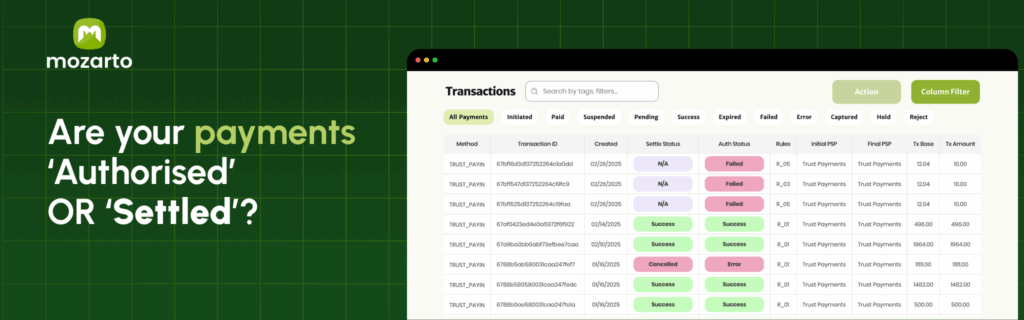

Many ‘instant’ payments still face delayed settlement. Merchants need visibility and certainty—Mozarto’s platform delivers both via API and webhook.

QR code payments are gaining traction among UK SMEs, offering instant, low-cost transactions and new ways to drive loyalty through open banking.

Embedded finance is no longer optional—it’s how brands remove friction, retain users, and unlock new revenue streams without added regulatory burden.

APP fraud cost the UK £450m in 2024. With scams starting online, debate grows on who should bear responsibility for prevention.

Banks must rethink card issuing as a strategic lever—focusing on UX, simplification, cloud agility, and resilience to stay ahead in payments innovation.

There is no excerpt because this is a protected post.

Ripple selects BNY Mellon to custody RLUSD reserves, strengthening institutional trust in its enterprise-grade stablecoin for global payments.

OpenPayd partners with Ripple to power real-time EUR and GBP payments, expand stablecoin access, and simplify global cross-border transactions.

Dialect welcomes Lynsey Hoxha as head of sales, bringing 15+ years of fintech experience to drive growth and deepen industry partnerships.

Bottomline helps banks modernise payments with integrated platforms, ISO 20022 readiness, and scalable real-time solutions for global compliance.

CASS 15 imposes strict safeguarding rules on payments firms. Learn what’s required by 2025 and download the guide to stay compliant.

Virtual cards gain momentum in Q3 as merchants seek faster, safer, and more scalable ways to manage business spend and streamline payments.

Paydock simplifies complex payment workflows, enabling merchants to launch faster, reduce costs, and scale with just a few lines of code.

PXP partners with Moneycorp in Q3 to offer real-time FX, 130+ currencies, and smarter treasury tools for faster, borderless commerce.

Discover how Techwave uses AI, data, and embedded finance to transform payment operations, boost reach, and drive fintech innovation at scale.

The cross-border payment platform has grown into a fully developed financial infrastructure with a robust acquiring solution—complete with a new name, logo, and color palette.

UK banks need modern card processing with minimal risk. Worldline offers cloud agility, migration expertise and regulatory assurance in one.

PSPs that embrace automated, API-first onboarding can turn compliance from a bottleneck into a strategic growth driver—faster, smarter, and globally scalable.

AI agents are reshaping payments. Learn how tokenisation and cloud-first infrastructure are unlocking the next era of autonomous digital commerce.

Gen X prioritises payment security, trust and rewards. PXP research shows they favour cards over wallets and value clarity over novelty.

We’re new to the Payments Association, but not new to payments. We’ve been helping businesses handle transactions smoothly for decades, from fuel stations to vending

myPOS, a leading provider of integrated payment solutions for businesses across Europe, has announced the appointment of three new Country Managers as part of its

We’re excited to announce our FX Inbound Auto Conversion solution — designed to help you grow your business whilst staying compliant with upcoming FCA safeguarding

BAT-VC, a leading venture capital firm specializing in fintech and cross-border innovations, has announced a strategic growth investment in Payall Payment Systems. The investment will

Q3’s updated UK NRA reclassifies EMIs as high risk for ML and TF, prompting debate across the sector on compliance, innovation and proportionality.

Worldline experts highlight digital wallet trends shaping Q3 Europe with focus on interoperability digital ID convergence and invisible payments evolution

Payments regulation roadmap Q3 2025 UK and Europe highlights key compliance updates including SEPA Instant FCA safeguarding crypto rules and horizon scan.

Yaspa partners with VIALET to expand real-time multi-currency payments across UK and Europe, enhancing merchant options and Q3 2025 regulatory readiness.

Yaspa secures \$10m from Discerning Capital to expand US gambling payments, scaling A2A solutions ahead of Q3 UK and EU regulatory horizon

UK Chancellor’s Mansion House speech sets Q3 regulatory agenda with Leeds Reforms targeting investment, fintech growth, and financial system rewiring.

Fintech’s audit processes remain manual and fragmented. Automating evidence collection and audit trails is key to scaling compliance in Q3 and beyond.

Chargebacks911’s 2025 Cardholder Dispute Index reveals rising UK and US chargeback misuse trends shaping Q3 merchant risk and compliance priorities.

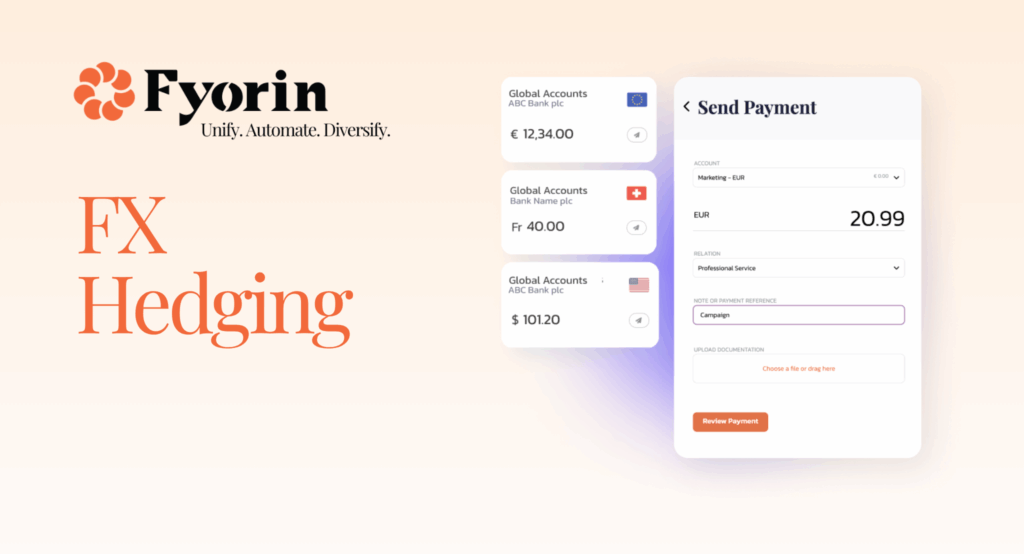

Fyorin expands its treasury suite with FX hedging for mid-market firms, offering embedded tools and Q4 2025 roadmap for broader treasury upgrades.

UK businesses are losing £70bn(i) annually by not attracting and retaining the custom of disabled people and their families, according to a new research report

Paymentology expands in MENA with a new Dubai hub, supporting growing demand for scalable issuer processing as digital banking accelerates regionally.

Explore 2025 financial crime trends, AI-driven fraud risks, regulatory challenges, and evolving prevention strategies shaping the payments industry.

Ecommpay wins Judges Award at FSF 2025 for its Payouts via Hosted Payment Page solution, recognised for innovation in secure, flexible payouts.

Help benchmark crypto compliance maturity—complete our short anonymous survey by 8 August to access insights, results, and an exclusive roundtable invite.

Payments sector D&I survey: 65% of firms keeping policies stable, with mixed priorities on sex, ethnicity, disability, and evolving evaluation practices.

Cloud-native POS platforms are reshaping merchant payments, blending AI, IoT, and omnichannel tools to boost efficiency, conversion, and CX at scale.

Paymentology appoints Julie Sutton as Head of Growth, Europe, strengthening its leadership team to scale issuer processing solutions across the region.

OpenPayd launches stablecoin infrastructure, enabling instant, compliant fiat-to-digital payments and accelerating global money movement for businesses.

The EBA clarifies how PSD2 and MiCA apply to EMTs, offering transitional relief and guidance ahead of PSD3 and the new EU Payment Services Regulation.

There is no excerpt because this is a protected post.