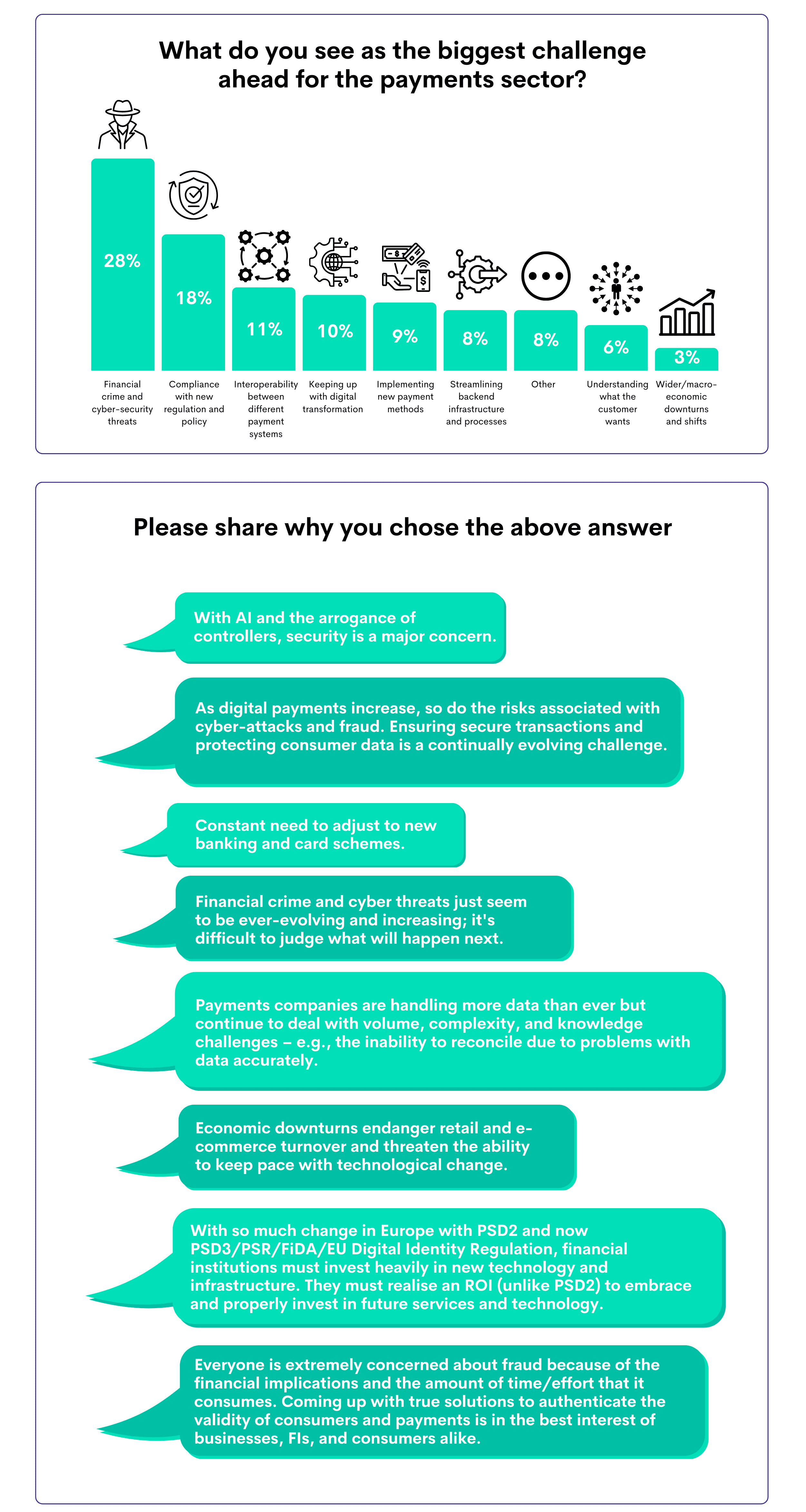

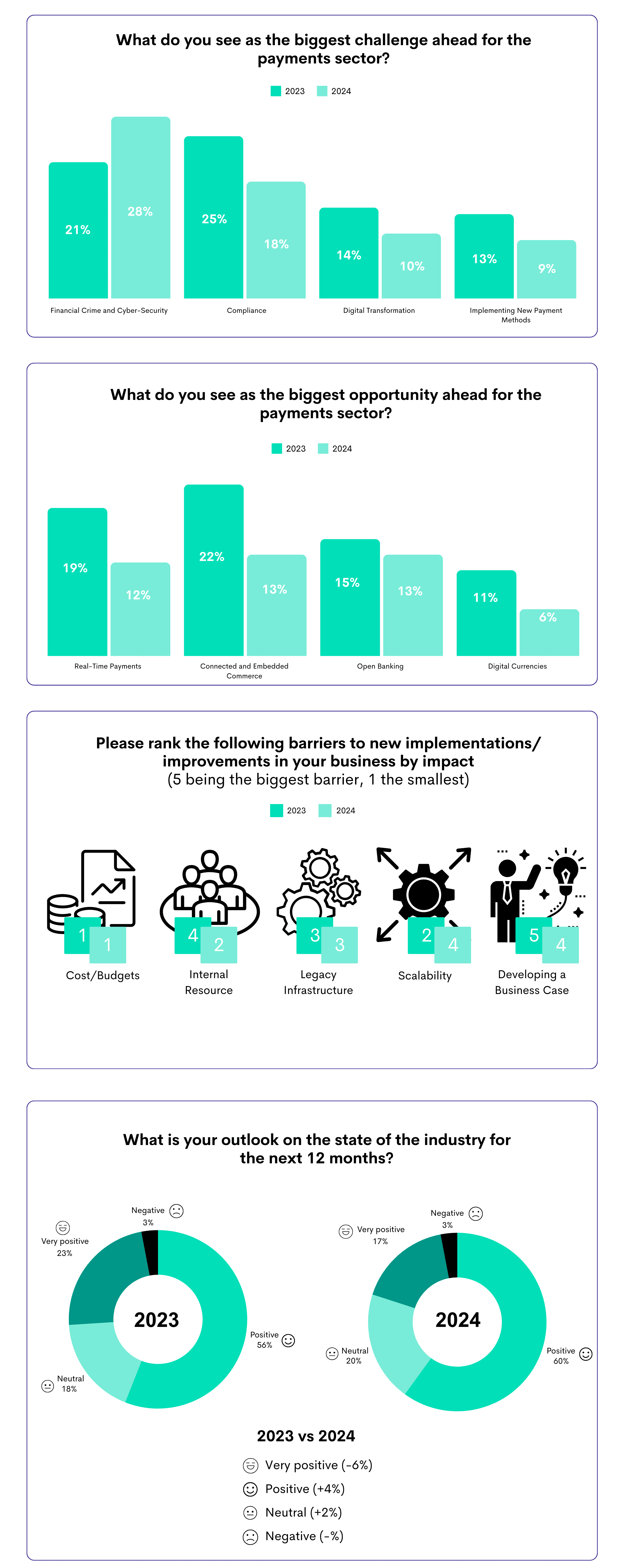

In light of the survey findings, payment industry leaders should prioritise enhancing security measures to address the escalating threat of financial crime and cybersecurity, which I believe is now the sector's most pressing challenge.

Investing in emerging technologies is not just important; it's pivotal for bolstering security, driving efficiency, and delivering customer-centric solutions. Fostering collaboration with fintechs and open banking providers may accelerate innovation and ensure seamless integration across the payments ecosystem.

Additionally, it is essential to address internal resource limitations and modernise legacy infrastructure to overcome operational barriers, maintain a competitive edge, and avoid regulatory scrutiny. As cost constraints persist, strategic investments in areas with the highest potential for ROI will be vital to navigating the complexities of the evolving market while capitalising on emerging opportunities.

The overarching view is one of positivity, rooted in embracing technology to drive modernising ageing stacks and applications but remaining, at all times, customer-centric. Technology has a great part to play in helping to combat the ever-present cyber security threat, with greater opportunity for AI, ML, Data & analytics to help combat, prevent and predict threats. Many see the benefits of collaboration with partners as “greater than the sum of their parts”, helping to alleviate challenges with modernising legacy technology and remaining regulatory compliant. But, we should always focus on competitive collaboration to drive innovation.

Consumer behaviour 2026 report

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.

How AI-powered banking tools are failing vulnerable customers

New research shows vulnerable customers are strong adopters of AI and digital banking, but are far more likely to experience failed payment journeys and poorer outcomes.

Agentic commerce in UK retail: An unresolved liability question

UK merchants expect agentic commerce to grow rapidly, but uncertainty around liability, fraud, and standards is slowing readiness.