List of MCC codes & risk levels — Retail, e-commerce, travel, gambling, crypto, and more

Merchant category codes (MCCs) impact fees, chargebacks, compliance, and payment approvals—understanding your MCC can help optimise costs and reduce risks.

Merchant category codes (MCCs) impact fees, chargebacks, compliance, and payment approvals—understanding your MCC can help optimise costs and reduce risks.

PXP partners with Snowflake to deliver real-time data insights for merchants, combining advanced analytics with payment platform innovation.

Shape and PXP partner to deliver a turnkey payments solution for ISOs, ISVs, and Payfacs, combining automation, customisation, and scalability.

BPC’s latest report explores key trends reshaping acquiring, from soft POS and A2A payments to data-driven services and regulatory impacts.

How smaller landlords can improve rent arrears collection with automated engagement and simple payment tools—without adding to workloads.

SEON’s 2025 Digital Fraud Report explores how businesses are adapting to rising AI-driven fraud with increased spending, tech, and specialist teams.

A look at the FCA’s upcoming safeguarding rule changes for payments and e-money firms — and what businesses need to do to prepare.

Fyorin launches physical cards and smart expense management to help businesses streamline spending, improve control, and automate compliance.

Why merchant category codes (MCCs) matter—and how choosing the right one can reduce fees, manage risk, and improve payment approvals.

PLIM offers flexible, interest-free payment solutions for aesthetic treatments, making self-care more accessible while supporting clinics to reach more clients.

Chargebacks911 and Prommt partner to offer end-to-end solutions that help businesses prevent chargebacks and secure remote payments.

Mastercard and Thought Machine expand their partnership to modernise banking with cloud-native core and payment solutions.

Unlimit names Simu Liu as its first global brand ambassador, launching a major campaign on versatile payment solutions worldwide.

Lynx Tech launches AI-driven AML screening to help financial institutions combat money laundering with speed and accuracy.

The EBA’s redefinition of e-money challenges traditional models, raising regulatory uncertainties and requiring compliance reassessment.

Chargebacks and fraud are rising, causing financial losses and operational strain for businesses navigating digital transactions.

Exactly.com showcases its full-stack payment solution at the Retail Technology Show 2025, helping e-commerce businesses scale and reduce costs.

What’s next for payments regulation in 2025? Hear from industry leaders at the EY Payments Forum in March.

How are Finastra and Salt Edge advancing open banking? Discover their partnership’s impact and future vision.

How is Optimus gearing up for growth in the payments industry? Discover their new strategy and product offerings at PAY360.

How is Flutterwave driving enterprise payment growth in Africa? Discover key insights from its 2024 report.

How does your fraud strategy compare to industry standards? Explore Sift’s Fraud Industry Benchmarking Resource to find out.

How can financial institutions de-risk digital transformation and maintain quality at pace? Discover insights at PAY360’s Disruption Zone.

How are changing consumer habits shaping the peak shopping season? Discover Tink’s insights and catch them at PAY360 2025.

Are financial institutions risking payment glitches with DIY testing? Explore the benefits of specialist payment testing solutions.

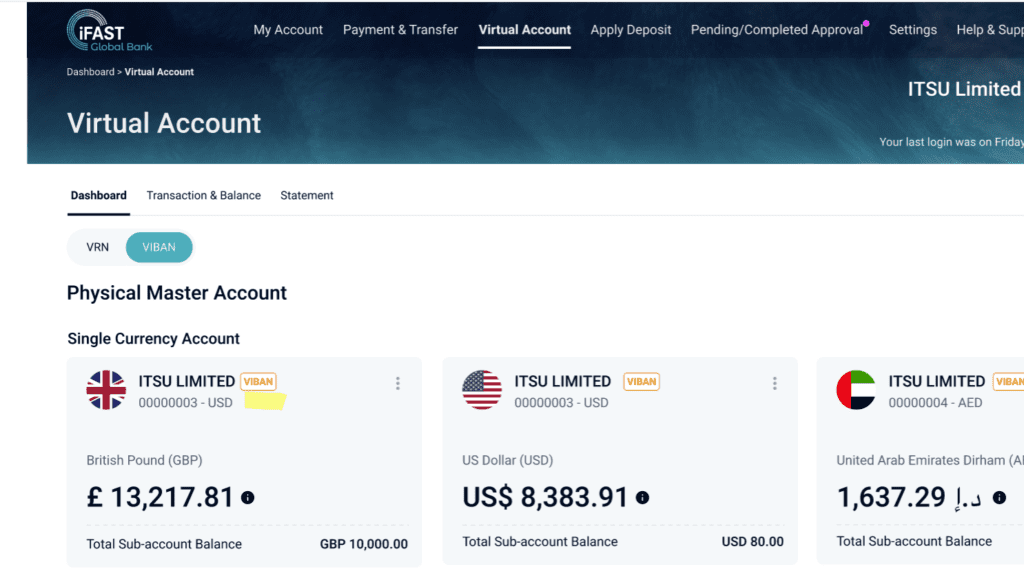

iFAST Global Bank pilots virtual IBANs, offering multi-currency solutions for EMIs, APIs, brokers, and large corporates.

Why must financial institutions rethink authentication to stay competitive post-PSD2? Explore the need for modern, risk-based solutions.

Bottomline has been named ‘Cross-Border Payment Company of the Year: North America’ for its global connectivity solutions.

Discover how Mitto’s CRM integrations enable customer engagement across SMS, WhatsApp, and Viber.

How can fleet and mobility businesses outsmart payment fraud? Find out in this upcoming webinar.

Can banks and fintechs balance seamless payments with robust security? Explore the debate in this upcoming webinar.

Legacy systems are a competitive risk—financial institutions must modernise with AI, automation, and cloud solutions to stay agile and scalable.

AI-driven fraud is evolving fast—banks must adopt adaptive AI models to detect and prevent scams in real-time.

Trudenty joins Mastercard’s Start Path to revolutionise fraud prevention with privacy-preserving data sharing and real-time consumer trust insights.

With AiTM fraud rising, businesses must strengthen security, adopt biometrics, and educate users to stay ahead.

E-invoicing is transforming financial operations, enhancing efficiency, compliance, and fraud prevention while shaping the future of digital tax systems.

Forex brokers must adopt payment orchestration, real-time settlements, and AI fraud prevention to stay competitive and compliant.

Personalised, omnichannel payment experiences are key to deepening loyalty, boosting retention, and exceeding customer expectations.

The future of e-commerce is subscription-based, offering businesses predictable revenue, deeper customer relationships, and long-term growth.

The future of payments is digital, inclusive, and transformative—driving financial access, innovation, and global economic empowerment.

Open finance is redefining data sharing, innovation, and growth in financial services.

Travel is surging, but outdated payments lag—fintech-driven innovation is key to seamless, secure, and sustainable transactions.

European banks must embrace digital transformation and fintech partnerships to stay competitive and compliant.

In 2025, payments firms must prioritise safeguarding funds, expanding open banking, and preparing for stablecoin regulation to stay competitive and compliant.

Open banking holds promise for e-commerce, but its success depends on targeted use cases, merchant incentives, and consumer trust.

Mobile payments and digital wallets are driving a cashless economy, reshaping commerce, and redefining consumer expectations.

Discover how AI is transforming cybersecurity, both as a weapon for attackers and a shield for defenders, in this webinar.

UPI is transforming cross-border payments, boosting India’s global digital payment reach.