Agentic commerce in UK retail: An unresolved liability question

UK merchants expect agentic commerce to grow rapidly, but uncertainty around liability, fraud, and standards is slowing readiness.

UK merchants expect agentic commerce to grow rapidly, but uncertainty around liability, fraud, and standards is slowing readiness.

Stablecoins are moving into mainstream finance, reshaping payments, trade, and regulation as institutions explore faster, programmable settlement.

Bankfeed and Salt Edge partner to automate multi-bank operations, enabling real-time data access, faster reconciliation, and more efficient payment workflows for SMBs.

There is no excerpt because this is a protected post.

As A2A payments expand in UK commerce, clear “certainty of fate” confirmation is vital to ensure trust, avoid duplicate payments, and support reliable merchant fulfilment.

NoCFO has partnered with open banking provider Salt Edge to embed payment initiation directly into its AI-native financial platform, allowing small business owners to approve and pay invoices without leaving

UK e-commerce is maturing fast, pushing banks to support both cards and open banking. Success will depend on orchestration, fraud control, and modern acquiring infrastructure.

Open banking is growing steadily, but trust, commercial viability and regulation will determine whether it reaches mainstream scale.

Salt Edge has launched a bulk payments solution using open banking APIs, enabling fintechs and platforms to execute secure, real-time mass payouts across Europe.

A data-led analysis of the key trends shaping payments in 2025, offering clear insight into market shifts, technology adoption, and emerging priorities.

New research from The Payments Association shows confidence in regulation is split, while payments leaders increasingly view AI as the key to tackling financial crime.

Account-to-account payments are poised to redefine the UK’s payments landscape, but success hinges on trust, usability, and rapid open banking adoption.

As banks go digital and branches close, PaysafeCash offers a secure, branchless way to deposit cash, ensuring inclusion in a cash-reliant Europe.

Global adoption of open banking is uneven. Regulation, standards and governance will determine whether it scales or fragments

This whitepaper examines how APIs are reshaping banking, driving innovation, enabling open ecosystems, and balancing opportunities with risks.

The 2025 State of the Industry survey reveals rising cyber risks, shifting priorities, and strong investment in payments innovation.

Infographic: UK SMEs weigh up the pros and cons of open banking, revealing a fragmented but growing interest in account-to-account payments.

Yaspa partners with VIALET to expand real-time multi-currency payments across UK and Europe, enhancing merchant options and Q3 2025 regulatory readiness.

UK SME survey shows open banking intrigues merchants with faster, cheaper payments, but gaps in awareness and security fears slow adoption.

Open banking and instant payments are reshaping how regulated sectors manage compliance, onboarding, and real-time money movement at scale.

QR code payments offer UK small businesses a fast, low-cost alternative to card terminals—boosting cash flow and meeting modern customer expectations.

Open Banking’s value lies in transforming raw transaction data into actionable insights—boosting accuracy, fraud detection, and customer understanding.

Banks must ditch rigid legacy cores—modular, decentralised architectures enable agility, resilience, and innovation for a truly future-ready enterprise.

Open finance is expanding data-sharing beyond banking, reshaping payments, lending, and financial services worldwide.

How are Finastra and Salt Edge advancing open banking? Discover their partnership’s impact and future vision.

How are changing consumer habits shaping the peak shopping season? Discover Tink’s insights and catch them at PAY360 2025.

Open finance is redefining data sharing, innovation, and growth in financial services.

Open banking holds promise for e-commerce, but its success depends on targeted use cases, merchant incentives, and consumer trust.

The EU’s shift to open banking and finance presents both opportunities and challenges, demanding a balance between innovation, security, and regulation.

Open banking faces rising fraud risks, demanding industry-wide collaboration and smarter security solutions to build trust and resilience.

A2A payments, enabled by open banking, provide faster, cheaper, and more secure direct bank transactions, transforming industries like e-commerce and gaming.

Bahrain mandates corporate APIs in open banking, boosting fintech innovation and SME financial access.

In today’s globalised business environment, managing international payments, taxes, and compliance can be daunting. The Merchant of Record (MoR) model offers a solution, taking on the responsibility of payment processing, tax management, and regulatory compliance, freeing companies to focus on core operations and growth.

Open Banking set out to revolutionize finance by giving third-party providers access to customer data (with consent) to drive innovation and empower consumers. But while Europe’s PSD2 regulation has enabled new fintech services and a vibrant TPP ecosystem, adoption has fallen short of initial expectations. Complex regulations, security concerns, and, most critically, profitability challenges for banks have created hurdles. Discover how a shift in strategy, combined with data enrichment, could help banks embrace Open Banking as a growth opportunity rather than a regulatory burden.

Noda’s Pay & Go simplifies registration, KYC, and payment processing in one flow, enhancing conversion rates and user onboarding.

How open banking can reshape finance, enabling personalised services, streamlined verification, and improved fraud detection.

Open banking enhances financial convenience and transparency, but security depends on using regulated providers and careful data sharing.

Trust frameworks are the cornerstone of a secure and competitive open finance ecosystem, ensuring safe data sharing and fostering innovation across the financial services landscape.

Banks and criminals are locked in competition for customers and transaction revenue, using advanced technologies as weapons of choice. Technologies that deliver speed and convenience in modern banking, if unprotected,

UK banks’ reduced lending and account closures stress SMEs, highlighting the need for multi-service apps (MSAs) to streamline financial services with open banking.

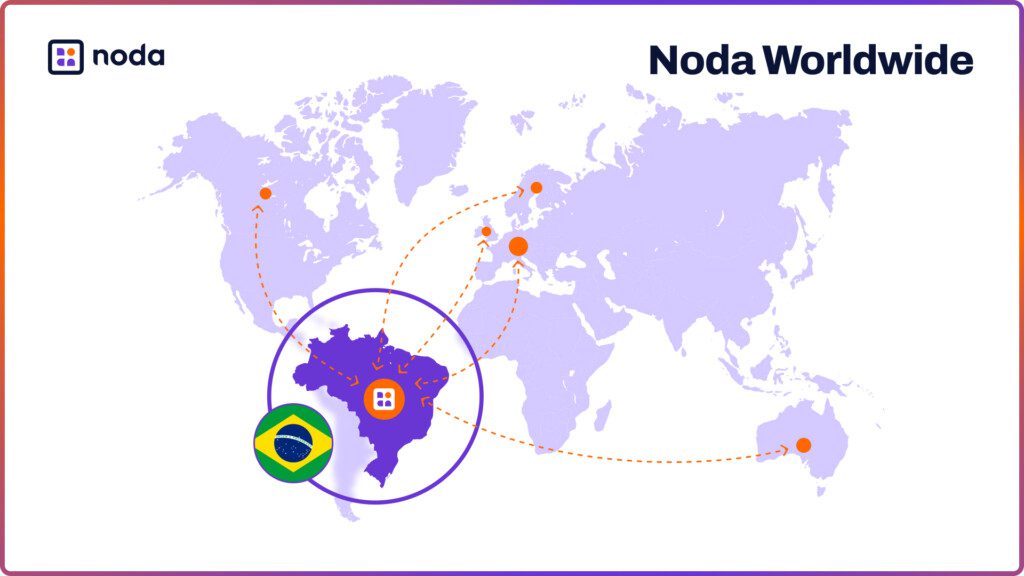

Noda is expanding its open banking network to Brazil, allowing merchants to access seamless cross-border payment services, unified reconciliation, and instant banking across Brazil, Europe, the UK, and Canada.

The payment operations sector is navigating significant challenges due to capped interchange fees, driving a need for digital transformation, cost reduction, and innovative revenue models to maintain profitability.

Open banking revolutionises financial services by enhancing user experience with seamless account integration, real-time transactions, and personalised services.

Open banking in the UK has yet to fulfil its potential, with apparent division between banks and fintechs regarding how best to proceed and establish viable commercial models.

Predicting customer lifetime value (LTV) equips businesses to allocate resources efficiently, focus on high-value customers, and enhance personalised marketing strategies, thereby increasing profitability.

Confirmation of Payee (CoP), a relatively new service in the UK banking landscape, has emerged as a powerful weapon in the fight against fraud. By verifying the name on a

The UK leads the open banking revolution, driven by the Payment Services Regulations and the revised PSD2, fostering competition, innovation, and secure data access, with significant adoption growth and benefits for businesses and consumers alike.

PSD2 mandated banks to share customer information with licensed third-party providers through secure application programming interfaces (APIs), contingent upon customer consent.