What is this article about?

The challenges faced by the payment operations sector due to shrinking card payment revenues caused by capped interchange fees.

Why is it important?

It highlights the need for banks and payment providers to adapt their business models and operational strategies in response to regulatory pressures and technological advancements

What’s next?

Accelerating digital transformation, focusing on automation and cost reduction, adopting alternative revenue models, and leveraging transaction data for personalised services and improved customer engagement.

Credit card losses and associated costs are skyrocketing across the UK, US, and EU, hitting payment operations hard. The sector is now struggling to cope as capped interchange fees shrink card payment revenues. In the EU, these fees are capped at 0.2% for debit cards and 0.3% for credit cards, significantly lower than the previous rates of 0.5-2.0% before the Interchange Fee Regulations of 2015.

Card issuers must find ways to reduce their operational costs to maintain profitability. This could involve streamlining payment processes, automating various operations, and leveraging technology to enhance efficiency. However, implementing automation and advanced technologies often requires significant upfront investment. This includes the cost of purchasing new systems, integrating them with existing infrastructure, and training employees to use them effectively.

The increasing complexity of international card schemes means payment networks constantly update their systems and requirements, leading to more complex operations for issuers.

Rivero co-founder Fatemeh Nikayin tells Payments Intelligence that she’s seeing “a constant stream of updates from payment networks. Payment network licensees (issuers and acquirers) face increasing weekly requirements and updates from each network, requiring them to receive, digest, and implement these updates across multiple schemes.

“This process becomes even more complex when you factor in new payment methods entering the market. Surprisingly, before we started our company, there was no solution available to help banks manage this increasing complexity.”

Alongside this, ensuring compliance with regulatory requirements adds another layer of complexity. New technologies and processes must meet stringent security, data privacy, and compliance standards, which can be resource-intensive to implement and maintain.

Nikayin’s colleague, CEO and co-founder of Rivero, Thomas Mueller, believes that overheads for compliance costs are going up as revenues decline. He says: “You have to invest more in that area than maybe some 10 or 20 years ago.

“Customers these days are more demanding in terms of customer service, what they expect, and if you can’t already do that in a digital form, in a self-service form, you will just keep hiring more and more people to staff your customer support hotline, which drives costs quite substantially and does not necessarily help with the quality of customer service.”

Impact on payment revenues

Increased regulation on interchange fees, especially in Europe and globally, is reducing revenue per transaction. Meanwhile, stricter regulations on credit card interest rates in many European countries are limiting the profitability of credit products.

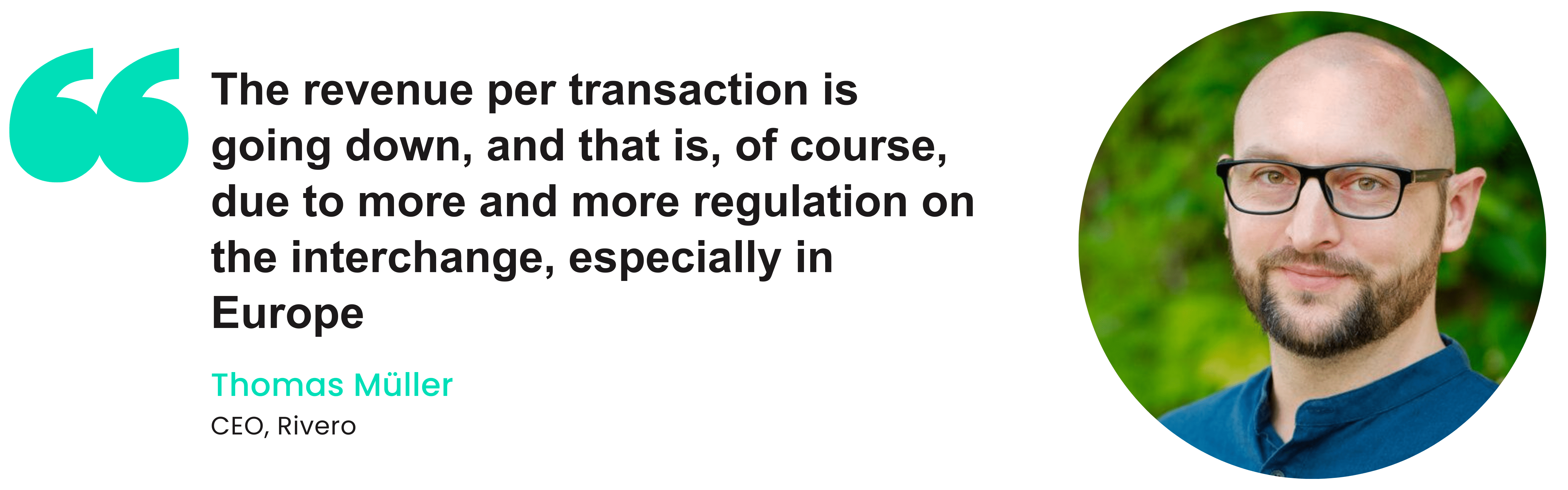

Mueller says: “The revenue per transaction is going down, and that is, of course, due to more and more regulation on the interchange, especially in Europe.” The trend, which Mueller believes shows no signs of reversing, is forcing banks and payment providers to reassess their business models and operational strategies.

This shift is likely to accelerate digital transformation efforts, with a focus on automation and cost reduction. Additionally, it may lead to industry consolidation as smaller players struggle to remain competitive.

Banks and payment providers will need to prioritise customer engagement and loyalty, potentially moving towards more service-oriented models. Ultimately, this regulatory-driven change is reshaping the payment landscape, pushing the industry towards greater efficiency and innovation to maintain profitability in a lower-margin environment.

Consumer awareness has also substantially increased, with more and more people comparing card products and services from neo and challenger banks. Mueller also notes that “Card payments used to be a significant source of revenue due to foreign exchange (FX) rates. Traditional high-street banks typically offered unfavourable rates, allowing them to profit significantly from these FX gains. However, consumer awareness has since increased, as people now compare rates more actively.”

This increased awareness and tendency to compare products is putting pressure on traditional banks’ revenue streams, particularly in areas like foreign exchange rates and annual card fees.

Cost-saving measures and operational efficiency

Mueller believes automating back-office operations is essential to streamlining operational efficiency while revenues are down. He says: “I believe that the digital transformation we have witnessed in the banking sector may have appeared fairly rapid at first glance. Many banks have introduced apps with decent features, which give the impression of digital transformation. However, when we look at what’s actually happening behind the scenes, it’s possible that much of the process is still very manual.”

He adds how some banks have created a facade of digital processes while still relying on manual work behind the scenes: “To the extent that sometimes we hear stories of a bank claiming to have digital onboarding in the app, but in reality, the process is just automated in the digital channel and then someone in the back-office manually inputs that data into another system.”

He suggests that the next phase of digital transformation will focus on these behind-the-scenes processes. The goal is to modernise and automate back-office operations to improve efficiency and reduce costs. Further, the trend towards insourcing is driven by the need for more control over data, real-time data processing capabilities, and the desire to reduce dependence on external processors.

While outsourcing has been popular due to perceived cost savings, a trend towards insourcing is emerging. This shift is driven by banks’ desire for greater control over their payment value chain and data, enabled by technological advancements and the modernisation of core banking systems.

Banks are now more capable of handling real-time processing requirements in-house, reducing dependence on external processors. However, this doesn’t mean a complete move away from outsourcing. Instead, banks are adopting a more nuanced approach, insourcing core functions while selectively outsourcing specific services to specialised, modern providers.

Nikayin adds: “Many payment processing providers offer a variety of services, but their primary focus is on processing transactions. The additional services they offer alongside payment processing are often of mediocre quality and based on outdated technology. Sometimes, these services are acquired from other companies and integrated into the processors’ systems.”

This strategy allows banks to avoid the limitations of all-in-one outsourced solutions, which often offer mediocre or legacy ancillary services, and instead choose best-in-class solutions for each aspect of their operations. This hybrid approach aims to optimise operational efficiency, improve data control, and enhance the ability to innovate and differentiate in a competitive market.

Mueller explains the reasons behind this shift: “I think banks are starting to try to integrate more vertically, so to speak, and bring a lot more of this payment value back in-house. Modern technology allows us to do that, whereas in the past, we were more dependent on a payment issuing processor because of the real-time requirements.”

Alternative revenue models as potential solutions

As traditional revenue streams face pressure from regulation and competition, banks are exploring innovative ways to maintain profitability. They’re leveraging rich transaction data to offer personalised, contextual value-added services.

Igor Skachkov, chief product officer at payabl. believes AI-powered solutions are developing rapidly, and these technologies are adding tremendous value.

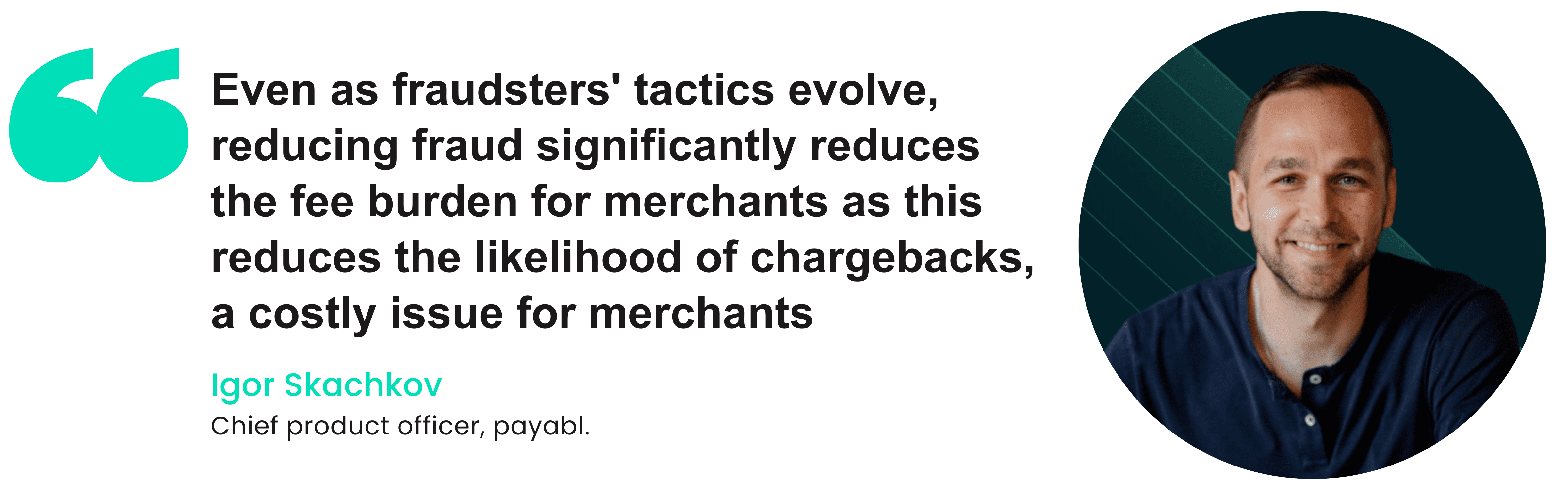

He tells Payments Intelligence: “Even as fraudsters tactics evolve, reducing fraud significantly reduces the fee burden for merchants as this reduces the likelihood of chargebacks, a costly issue for merchants.

“There are alternative payment methods (APMs) with lower fees, such as open banking or local wallet payments, which are gaining popularity in specific markets. Merchants can use payment orchestration to work with different acquirers globally, routing transactions via local acquirers to reduce costs.”

Mueller believes that value-added services can add great value to a customer offering. He says: “Imagine you booked a flight using your card, and your bank is aware of it. This is the perfect time for them to send you a push notification a few hours later, suggesting an insurance product they offer in partnership with others.”

Some are adopting a marketplace approach, selling third-party services and earning commissions. Strategic partnerships, like offering Uber credits with certain card products, are being forged to appeal to specific demographics. Banks are also using customer insights to develop targeted products and bundle value-added services with existing offerings.

“We’re seeing that banks are not only selling their own services on their digital channels, but they are also trying to act more like marketplaces by selling services from other companies and taking a share of the revenue in the process.”

There’s also a growing focus on engagement-based models to encourage more frequent card usage. Additionally, transaction data is being utilised to smartly cross-sell other financial products. These alternative revenue models aim to create new value propositions that offset declining fees and interest income while enhancing the overall customer experience.

Partnerships based on customer data refer to banks using insights from their customers’ transaction history to form strategic alliances with other businesses. This approach allows banks to offer more relevant services and generate additional revenue.

Leveraging transaction data

Leveraging transaction data is becoming increasingly crucial for banks to generate personalised offers and improve customer engagement. Mueller emphasises its importance: “There’s not a single other banking product capable of giving me as much insights about you as a persona.” This data allows banks to build detailed customer profiles, enabling targeted marketing and product development. However, challenges exist in accessing and processing this data effectively.

As Mueller notes: “It is crucial for banks to have access to complete and accurate transaction data, which can be a significant challenge as only parts of this data often flow from the processor to the bank. Additionally, real-time or near-real-time processing capabilities are essential for making timely and context-specific offers.”

Nikayin adds that leveraging this data effectively requires modernising back-office systems: “To get there, banks really need to digitalise the back office to be able to leverage that intelligence and data”.

By effectively harnessing transaction data, banks can not only improve their product offerings but also identify strategic partnerships and increase customer engagement, ultimately driving more transactions and revenue and gaining top-of-wallet positions for their cards.

There is a significant shift emerging towards a best-of-breed approach, moving away from one-stop-shop suppliers. Mueller explains: “We are observing a shift away from obtaining all of this from a single large entity, typically the payments processor, towards a more best-in-class approach.”

This strategy allows banks to work with “the leading edge provider in each category,” potentially improving their services in areas like fraud detection. By adopting a best-of-breed approach, banks can “unbundle these services and get the best type of products from the more modern providers,” offering them greater flexibility, improved performance, and the ability to differentiate themselves in a competitive market.

Importance of customer engagement for increased transactions

Customer engagement is crucial for increasing transactions because it keeps the bank’s card at the forefront of customers’ minds, encouraging more frequent use.

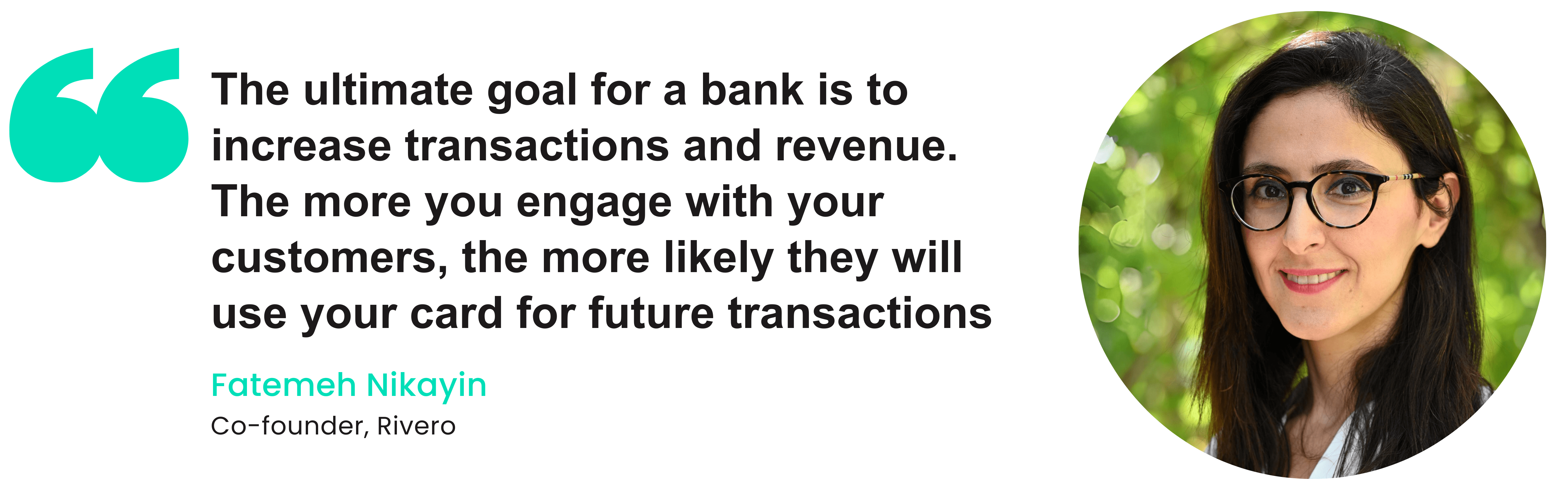

Nikayin says: “The ultimate goal for a bank is to increase transactions and revenue. The more you engage with your customers, the more likely they will use your card for future transactions. By offering compelling services and unique deals, you can differentiate your card from others in the market.”

By offering personalised services, timely offers, and relevant partnerships, banks can create multiple touchpoints with customers throughout their daily lives. This constant engagement increases the likelihood that customers will choose that bank’s card for their next purchase, leading to higher transaction volumes and, consequently, more revenue for the bank. The key is to make the bank’s services an integral part of the customer’s routine, thereby driving loyalty and increased card usage.

What payment leaders must do

As the payment industry undergoes a significant transformation, driven by regulatory pressures, technological advancements, and changing consumer expectations. Banks and payment providers face challenges such as declining revenues from traditional sources, increasing operational costs, and the need for more efficient back-office processes.

To thrive in this evolving landscape, payment leaders should adopt several key strategies:

- Embrace digital transformation, particularly in back-office operations, to streamline processes and reduce costs.

- Leverage transaction data to create personalised offerings and improve customer engagement.

- Shift towards a best-of-breed approach in payment operations, combining in-house capabilities with specialised external services.

- Develop alternative revenue models, including contextual upselling, marketplace approaches, and strategic partnerships based on customer data.

- Invest in advanced technologies like AI and machine learning for fraud detection and improved customer service.

As the industry continues to evolve, success will depend on balancing operational efficiency with innovation while maintaining a strong focus on customer needs and preferences.

Skachkov points out the growth of instant payments as an alternative strategy: “Instant payments are gaining momentum and creating a cheaper and faster alternative to card payments. Card schemes see this growing trend and are trying to adopt new technologies to remain competitive. Merchants should look for a technological provider who can provide a variety of payment alternatives and help to reduce costs by providing strong anti-fraud solutions and cost-effective cross-border payments.”

Skachkov also makes note of the impact of both open banking and PSD2 on payment processing fees. “The implementation of digital currencies in European markets will create an alternative to costly card payments in the future, although this is some years away from realisation,” he adds.

By embracing these changes and continuously adapting their strategies, payment providers can turn challenges into opportunities for growth and differentiation in an increasingly competitive market.

Read more Payments Intelligence

Regulation Roadmap Q3

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Consumer behaviour 2026 report

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.

How AI-powered banking tools are failing vulnerable customers

New research shows vulnerable customers are strong adopters of AI and digital banking, but are far more likely to experience failed payment journeys and poorer outcomes.