A multi-service app may be the cure to what’s ailing small businesses

UK banks’ reduced lending and account closures stress SMEs, highlighting the need for multi-service apps (MSAs) to streamline financial services with open banking.

UK banks’ reduced lending and account closures stress SMEs, highlighting the need for multi-service apps (MSAs) to streamline financial services with open banking.

The first stablecoin was launched in July 2014, 10 years ago. A decade later, it has reached a market cap of $165 billion, with trillions in stablecoin payments settled each

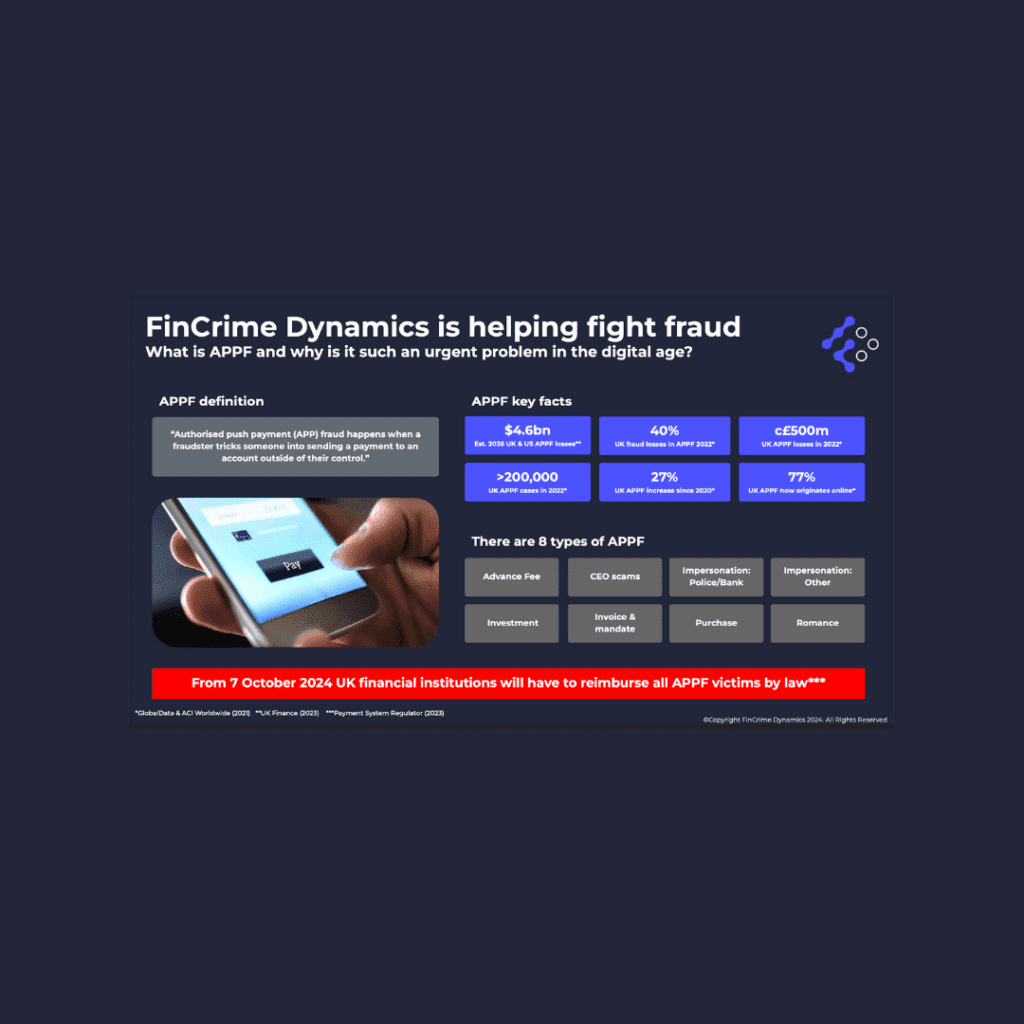

From 7 October 2024, UK financial institutions must reimburse APP fraud victims. FinCrime Dynamics’ SaaS service helps banks identify vulnerabilities, quantify losses, and improve fraud defences.

The “Redefining Community Finance: Unlocking Pathways to Financial Inclusion” whitepaper by the Payment Association provided crucial insights and recommendations emphasising the need for enhanced innovation and support for the community

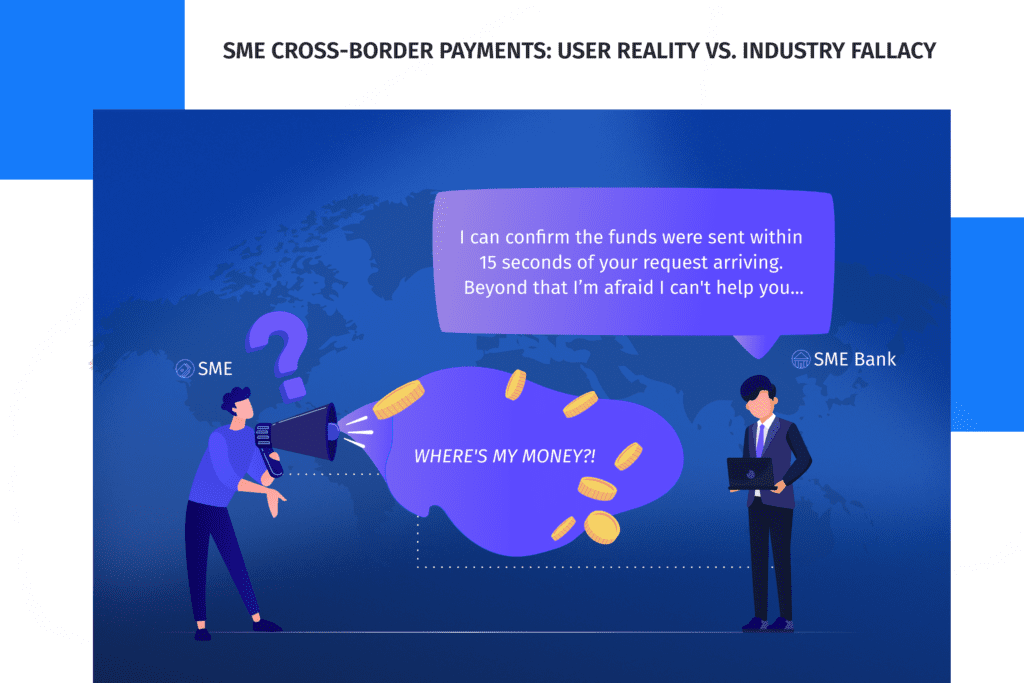

The white paper, “User Reality vs. Industry Fallacy,” examines cross-border payment challenges for SMEs and their crucial role in the global economy.

Mitto’s report shows increasing consumer demand for personalised, real-time communication via SMS and WhatsApp, aiding businesses in boosting satisfaction and engagement.

Issuers and merchants should adopt click-to-pay for a faster, safer eCommerce experience, reducing cart abandonment and enhancing security through tokenisation.

Privat 3 Money and ClearBank offer a multi-currency account with a single IBAN for seamless transactions and a new stainless steel P3 Debit Card, enhancing global financial management.

Paynetics has acquired Novus, the UK’s first “impact neobank,” to enhance ESG initiatives and expand its embedded finance offerings, empowering clients to integrate positive impact efforts with financial services across Europe.

Paynetics has been selected for TechRound’s FinTech 50 list for 2024, recognised for its innovative Embedded Finance solutions that seamlessly integrate payments into business offerings.

Swift’s updated CSP and IAF are essential for ensuring robust cybersecurity and compliance across the global banking community.

Giesecke+Devrient’s Convego payment card portfolio allows banks to use innovative and sustainable materials, such as wood and ceramic, to create unique and personalised payment cards.

The rise in online payment fraud has led nearly 98% of industry leaders to enhance security with identity verification and facial biometrics.

Digital wallet payments are projected to reach $19.6 trillion by 2027, and Thredd’s guide offers insights on trends, best wallets, tokenisation, and finding the right payments partner.

Trust Payments has partnered with Freepay to enable fast and secure payouts via Visa and Mastercard for Danish merchants, starting with Bingo.dk, enhancing payment processes and customer satisfaction.

Waitrose is partnering with Trust Retail to implement a dynamic inventory management system, improving stock visibility and freeing up Partner time for customer-facing activities, with full rollout expected by 2025.

Card issuer processors face integration, compliance, and fraud challenges but can stay competitive by streamlining processes and enhancing customer experiences.

A deep dive into the Financial Crime 360 survey, highlighting key challenges, prevalent fraud types, and strategic responses across various financial sectors

The financial struggles of UK adults highlight the vital role and challenges of community finance institutions in promoting financial inclusion.

Enhancing the FCA’s complaints reporting process aims to swiftly identify consumer harm, improve regulatory compliance, and streamline operations for financial firms.

Firms must navigate complex payment service regulations and the often-overlooked EBA Guidelines on Remuneration Policies to ensure compliance and foster fair customer outcomes.

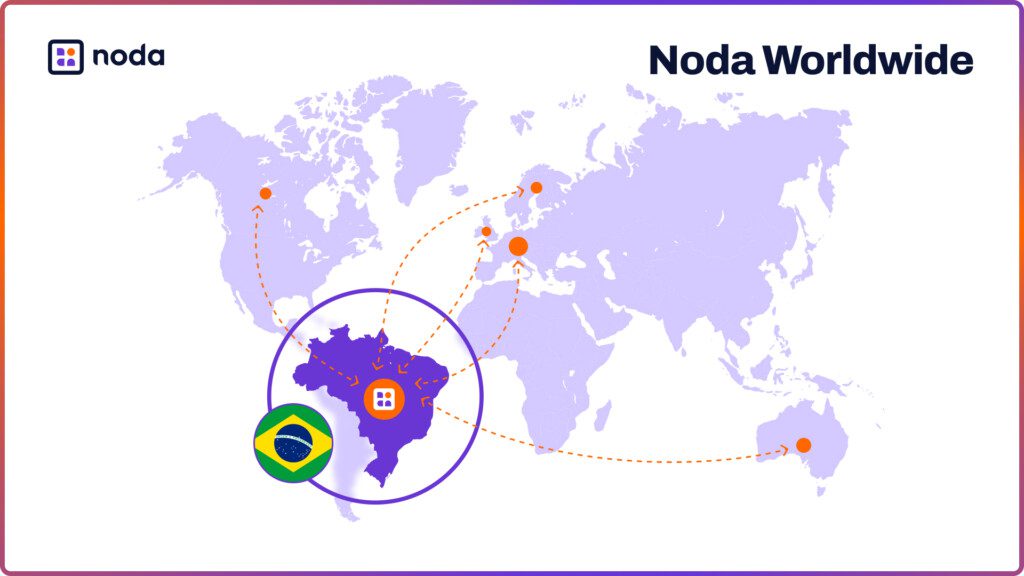

Noda is expanding its open banking network to Brazil, allowing merchants to access seamless cross-border payment services, unified reconciliation, and instant banking across Brazil, Europe, the UK, and Canada.

The payment operations sector is navigating significant challenges due to capped interchange fees, driving a need for digital transformation, cost reduction, and innovative revenue models to maintain profitability.

Navigating the complexities of global expansion in fintech requires strategic partnerships, innovative solutions, and a deep understanding of regional regulatory and cultural nuances.

New regulations will cap overdraft fees, drastically reducing them from around $30 to approximately $3, significantly impacting banks’ revenue streams.

Thames Technology, a leading provider of innovative payment solutions, has announced that it is one of the first card manufacturers to offer Mastercard-approved pre-paid paperboard cards. Designed exclusively for magnetic

The cross border payments landscape is experiencing rapid expansion. New corridors, new customers and new technology and processes are seeing more money than ever move across the globe. Consumer and

The digital payments landscape is rapidly transforming, driven by technological advancements and changing consumer preferences. Electronic money institutions (EMIs) facilitate secure and efficient digital transactions, enabling businesses and consumers to

Banks de-bank payment providers, disrupting cross-border transactions and financial inclusion.

Open banking revolutionises financial services by enhancing user experience with seamless account integration, real-time transactions, and personalised services.

APP fraud is surging, with UK Finance reporting £42.6 million lost in early 2023, prompting calls for stronger consumer protections.

Unlimit partners with Convera to simplify cross-border tuition payments for students in emerging markets, starting with Brazil using the PIX payment system.

Key findings from Cifas highlights the rising threat of identity fraud and the need for advanced, collaborative solutions.

The new APP fraud reimbursement policy mandates up to £415,000 per claim from October 2024, raising industry concerns over its implementation and impact on smaller fintech firms.

Payment businesses must leverage AI technologies to combat increasingly sophisticated fraud networks and protect digital transactions.

The payments space is facing a surge in online fraud, with almost 90% of business leaders reporting that online fraud is costing them up to 9% of their annual revenue

The Bank of England is modernising its RTGS system to boost resilience, innovation, and cross-border payment efficiency.

As the climate crisis unfolds around us, going green has never been more pertinent, or more prevalent. Industries from fashion to construction are being transformed by a drive towards sustainability,

Combining digital innovations with traditional in-person services allows banks to provide a seamless experience that leverages the convenience of digital services and the personal touch of physical interactions.

Utilising payments data analytics can drive financial growth by enhancing services, reducing costs, and improving security, though it requires overcoming challenges in data management, integration, and fraud prevention.

The FCA’s controversial ‘name-and-shame’ policy has sparked significant industry backlash, raising concerns over market stability and reputational damage.

Exploring the need for a digital euro to maintain Europe’s financial autonomy and enhance transaction efficiency in an increasingly digital global economy.

Adopting ISO 20022 is essential for modernising cross-border payments, enhancing fraud prevention, and ensuring seamless interoperability and efficiency in international financial transactions.

With Financial Crime 360 around the corner, Payments Review spoke to some of the leading figures working tirelessly to combat the growing issue of financial crime within the payments ecosystem.

Tony Sales, a former fraudster turned fraud prevention specialist and co-founder of WeFightFraud, shares his perspective on effective strategies and technologies businesses can use to protect against evolving threats.

Exploring the transformative impact of social commerce on consumer behaviour and the lurking risks of online scams.

Europe’s banks are enjoying a revival, but higher interest rates, bad loans, and tech challengers threaten to derail the recovery.

Exploring Australia’s comprehensive strategy to tackle payment fraud and enhance security across the national payments system.