What is this article about?

The Financial Conduct Authority’s controversial ‘name-and-shame’ policy and its implications for the financial industry

Why is it important?

The policy has sparked significant backlash due to concerns over potential market instability and reputational damage to firms.

What’s next?

The FCA may consider alternative strategies, such as anonymised reporting, to balance transparency with protecting firms’ reputations.

The Financial Conduct Authority (FCA) announced last month that it was promising to “engage further with industry” after the backlash from its controversial decision to ‘name and shame’ firms it was investigating proved to be greater than it expected.

The regulator’s plans to disclose firms ‘in the public interest’ caused uproar in the city. The Chancellor, alongside many others, called on the regulator to scrap the plan, saying the measure could impact firms’ valuations and destabilise financial markets.

In a speech at TheCityUK’s City Week last month, FCA executive director Sarah Pritchard cooled tensions by saying she recognised the move was “a sensitive and emotive issue.”

After issuing just eight fines in 2023, the regulator’s plan was designed to pressure banks to settle enforcement issues earlier. However, both the Economic Secretary to the Treasury, Bim Afolami, and Jeremy Hunt hit out at the plans, the former claiming that the regulator “still doesn’t get it.”

The debacle prompts the question: No matter the FCA’s intention in naming and shaming firms, how much transparency is necessary?

Usually, the regulator only names the firms it investigates under extreme circumstances. ‘ However, it believes that increased transparency could help maintain market integrity and provide consumers with early warnings about any questionable activities. The move is part of its commitment to safeguarding consumers, ensuring market legitimacy, and fostering fair competition.

However, this has not been recognised by the industry, with Natalie Lewis, partner and head of fintech, market infrastructure & payments at Travers Smith: “It is abundantly clear that the industry and other stakeholders are very concerned about these proposals, and the FCA’s next steps will need to be watched very closely.”

What are the concerns of companies with the name-and-shame mandate?

As of 31 March 2024, the regulator had 500 investigations underway. However, so far, it has only issued three fines, most recently to Citigroup. Last year, the regulator issued twelve fines totalling £53.4 million. So far this year, it has issued £28,695,840 in fines.

Data from the regulator also indicates that it only closed 153 investigations in 2023/2024, with 67% closed with no further action. The primary concern for businesses is knowing an investigation could be detrimental to business, with the likely outcome being closed with no further action. Another cause of concern is the likelihood that the move to name companies being investigated could be a case of guilt before proof in the public eye.

Lewis has reservations about the choice to reveal firms’ names under ‘exceptional circumstances’, claiming that the new test the regulator proposes “includes a very low threshold for publication.”

This raises a number of issues, including the potential for over-publication. Although the regulator has made subsequent comments indicating it does not intend to publish the information every time, there is uncertainty about how firms and their advisors will interpret this. Lewis believes companies are concerned that despite the FCA’s reassurances, the low threshold might lead to more frequent publications than necessary.

The FCA’s messaging is ambiguous, which could lead to varied interpretations and, therefore, confusion and inconsistent application of regulations. If information is published on a more frequent basis, it could have a number of negative ramifications for the firms involved, including reputational damage, increased scrutiny and the need to manage more public disclosures, the latter having the potential to create a heavy burden on firms in terms of their compliance and public relations teams.

What does this mean for businesses?

The implications for businesses are far-reaching. With reputation at stake, there is little room for error. As Lewis points out, given that most investigations do not culminate in formal enforcement action, investigations can last for years, with “no remedy available to a firm identified which is then ‘cleared’—it will largely have to live with any reputational damage that occurred in the meantime.”

Lewis notes that an unfortunate by-product of firms being ‘cleared’ of any wrongdoing is the likely fact that any public announcement exonerating the firm won’t receive the same media attention given to the earlier investigation announcement.

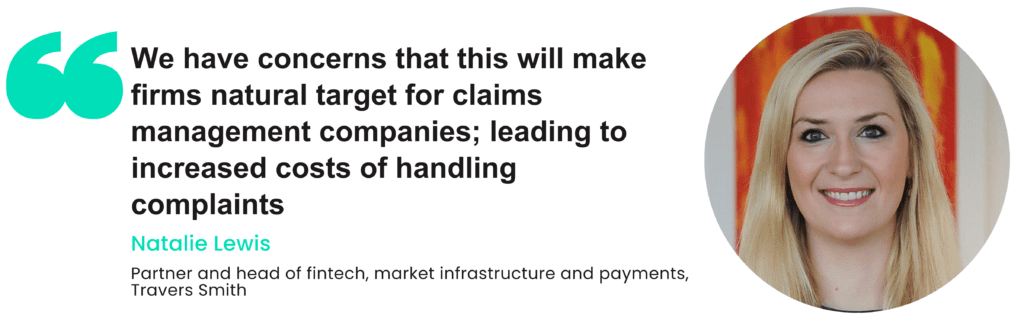

“Practically, we also have concerns that this would make the firm a natural target for claims management companies; this could easily lead to increased costs of handling complaints,” she admitted.

Why is the FCA naming firms involved in investigations?

In the foreword of the regulator’s consultation paper released in February, Therese Chambers and Steve Smart wrote:

“Reducing and preventing serious harm is one pillar of the FCA’s 3-year strategy and enforcement plays a vital role in delivering this aim effectively. Fines, bans and prosecutions are often what the public notices most about our enforcement work, and they are vital tools in holding to account those who don’t meet our standards. But enforcement action is not simply about individual instances of punishment. Its greatest impact is as deterrence, and in educating the whole market on what we expect, and where others have fallen short. Transparency about what we are investigating further helps to reassure, educate and drive our own accountability. That is why we’re proposing to communicate more about our investigations.”

It is clear that deterrence is one of the driving forces behind the move; however, given the likely event that an investigation is filed with no further action, is it strictly necessary to name and shame the firm?

Lewis points out: “There is an argument that it is worse than naming and shaming, as firms could get ‘named and shamed’ even if they go on to face no action.”

Thistle Initiatives Head of Payment Services, Lorraine Mouat, claims the FCA’s approach highlights a broader shift towards stricter oversight and accountability in the UK financial market.

She says: “Firms must adapt by enhancing their compliance frameworks, which may involve significant changes in operational practices and increased costs associated with regulatory adherence.”

Additionally, companies may become more conservative in their business practices, potentially leading to a more risk-averse industry culture, Mouat explains. “While this might reduce instances of misconduct, it could also limit innovation and competitiveness.”

Another suspected reason for the move is to highlight the differences between firms’ approaches to the hotly contested issue of APP fraud reimbursement. The Payments Association Director General Tony Craddock believes those using the PSR’s reimbursement reports are not qualified to interpret them effectively.

He tells Payments Intelligence: “This means that they change the behaviour of consumers, regulators, partners and investors in unintended ways. As APP Fraud is solely determined by the sending bank, the receiving PSP also has no ability to dispute their findings, which means the data is flawed from the outset. So I believe we should stop the ‘name and shame’ reporting currently undertaken by the PSR, which has no obvious anti-fraud benefit, immediately.”

The FCA believes this will educate other firms about potential issues and help deter future wrongdoing. However, Linklaters Counsel Sara Cody notes concerns that the FCA has not provided enough details about how this would work in practice. It also does not seem to fully appreciate the real risk that this may negatively impact firms’ reputations and business without achieving the FCA’s objectives.

She tells Payments Intelligence that the FCA’s lack of clarity is a concern. For example, the regulator has not provided enough information about what the notices would look like or how much information they would contain. Currently, there are also no specifics on the public interest test and how the impact on firms would be considered.

Currently, there are no specifics on the public interest test and how the impact on firms would be considered. Cody stresses that more clarity is needed on how the FCA plans to square naming firms with its confidentiality obligations during investigations. She was sceptical about the FCA’s ability to reconcile the two.

“If you compare this to consultations that we’ve had in the past about other moves to make investigations more transparent, such as the publication of warning and decision notices, they contained a breakdown of e.g. what a warning notice statement will look like or the statement at the start of a published decision notice that reminds readers that the decision in question has been referred to the Upper Tribunal.”

She adds: “This level of detail made it easier for firms to respond. Whereas I think here, we don’t know what the notice would look like. We don’t know how much information it would contain, other than that it would be enough to educate firms about conduct that they might need to look at because the FCA has concerns. So that that’s a problem.”

Has the regulator shot itself in the foot?

Cody expresses scepticism about the FCA’s ability to reconcile this with its confidentiality obligations. She believes that issues with the regulator’s confidentiality laws come into play.

She says: “The problem you’ve got with that is that the FCA is under an obligation to keep confidential information it receives about the business of a firm in the course of fulfilling its statutory obligations. Given this, it’s going to be very difficult to talk in any great detail about the concerns it has about an individual firm’s conduct if it does choose to publicise its new investigations.”

The regulator may breach its own confidentiality obligations by giving consumers enough information to ‘name and shame’ a firm suspected of wrongdoing.

“I don’t understand how the FCA thinks it can resolve this issue. If it can’t resolve this issue, then it isn’t even fulfilling its very first objective, which is to educate firms about conduct that could be a breach, or at the very least, concerning, more quickly.”

When it comes to other jurisdictions, Cody points out that the FCA is alone in what it is trying to do. “It does make us an outlier globally, particularly amongst financial services regulators,” she says.

This could be detrimental to investor confidence in the UK’s financial services sector; however, Mouat points out that it’s not just financial services firms that have criticised the move.

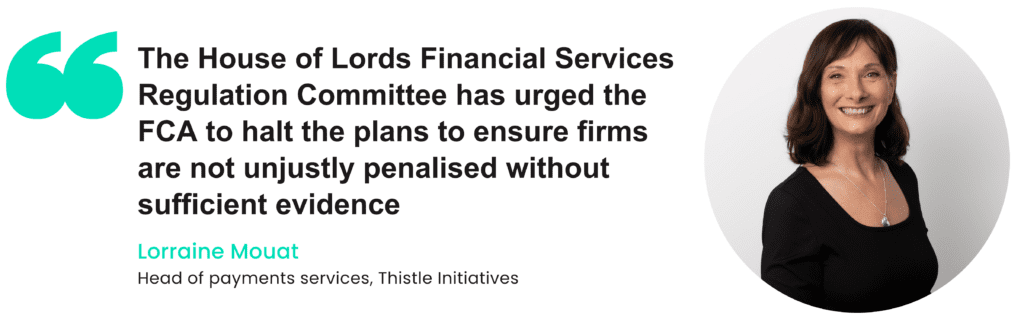

“Government officials and regulatory bodies have shown mixed reactions to the FCA’s proposal. Notably, the House of Lords Financial Services Regulation Committee has raised concerns about the potential market integrity risks posed by the policy. The committee has urged the FCA to halt the plans, citing the need for a more balanced approach that ensures firms are not unjustly penalised without sufficient evidence.”

What can the FCA do to right the situation?

As firms hit back at the FCA for its decision, there are alternate strategies that the regulator could adopt to maintain the market’s integrity without risking consumers’ and firms’ reputations.

Cody suggests an anonymised ‘Enforcement Watch’ publication, which could be published quarterly or annually, would be a better solution to the FCA’s concerns here. This could summarise ongoing investigations and areas of concern, educating the market but protecting firms by keeping the names of those under investigation anonymous.

Overall, she feels these alternatives could achieve what the FCA wants—deterrence and education—without many of the downsides of early publicity for new investigations.

Advice for firms

While the details of the FCA decision are uncertain, Cody recommends firms coordinate their communications, legal, PR, and board-level responses quickly once an investigation is announced publicly. She also recommends firms draft statements in advance in case they need to respond to or announce to the market. Meanwhile, operations and compliance teams need to be prepared to handle potential increases in customer/investor queries.

Cody criticises the short notice period proposed by the FCA in warning firms of an impending investigation, saying it should be pushed back on as it is not practical or feasible, especially if companies must coordinate across multiple jurisdictions.

Final thoughts and recommendations

The FCA’s ‘name-and-shame’ strategy, although rooted in intentions of market transparency and consumer protection, faces significant opposition from the financial industry. The potential negative ramifications, including reputational damage and increased operational burdens on firms, often without any formal enforcement action following investigations, outweigh the benefits at this stage, with further consultation deemed necessary.

The lack of clarity and low threshold for publication further exacerbate the industry’s unease. The FCA’s challenge lies in balancing its role as a watchdog with the need to maintain market stability and investor confidence. Alternatives like anonymised ‘Enforcement Watch’ publications could serve as a middle ground, providing the necessary deterrence and education without the adverse effects of naming firms.

Ultimately, the FCA must navigate these complex dynamics carefully to ensure its actions do not inadvertently harm the very market integrity it seeks to protect. Enhanced communication and clear guidelines will be crucial in addressing the industry’s concerns and achieving a sustainable approach to regulatory transparency.

More Payments Intelligence

Regulation Roadmap Q3

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Consumer behaviour 2026 report

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.

How AI-powered banking tools are failing vulnerable customers

New research shows vulnerable customers are strong adopters of AI and digital banking, but are far more likely to experience failed payment journeys and poorer outcomes.