I am delighted to be joined by Mikko Ohtamaa (tech freelancer), Steven Borg (VP of Finance at Gnosis) and George McDonaugh (KR1) for a discussion about DeFi on Thursday 1 October 2020 at 3pm BST (14:00 UTC). You can watch the talk here: https://lnkd.in/eXh8f3C

As preparation for the panel discussion I thought it might be useful to sketch out some views about a few regulatory issues related to DeFi — particularly by looking at a number of stablecoins, derivatives and DAOs. Separately, I will be publishing a series of articles summarising the new proposed EU regime for Markets in Crypto Assets (MiCA).

What is DeFi?

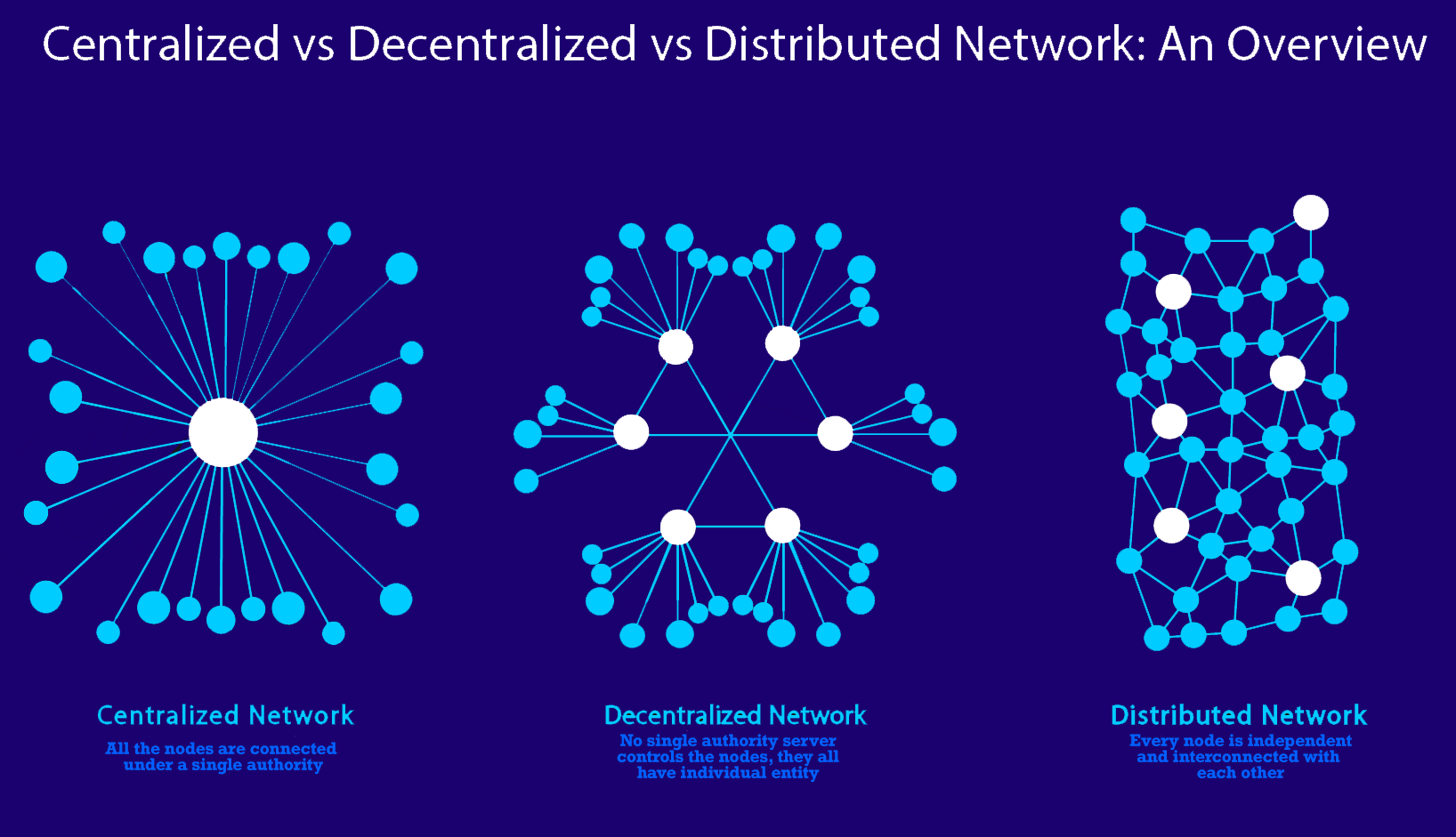

DeFi is primarily about the use of decentralised (and normally distributed) ledgers (often blockchain based) to undertake financial type transactions. The most common protocols for current DeFi projects are built on Ethereum using smart contracts.

The financial transactions may relate to, for example:

- decentralised exchanges (trading and position management) — 0x, justswap, uniswap, curve, kyber

- automated market making — uniswap, justswap, curve

- derivatives creation — synthetix

- lending and borrowing — compoundfinance, makerdao, aave

- earnings from staking (collateralising crypto assets for proof of stake or liquidity provision) — eth (2.0), staked

Crypto-assets can fall within the financial services frameworks when they relate to a range of financial assets. These could be:

- tokenised financial instruments such as securities (e.g. tokenised shares or bonds)

- tokenised funds (e.g. property funds)

- some forms of tokenised fiat currency (e.g. a fiat backed stablecoin issued by a European stablecoin issuer) under e-money legislation

- tokenised deposits (e.g. a bank issuing tokens against its deposits)

- tokenised B2C or P2P credit offerings or platforms (non-bank B2B corporate lending and borrowing often being out of regulatory scope).

Decentralisation for such transactions has enabled a novel way to structure intermediation of supply and demand for various assets which do not fit within the historic practical and regulatory model used for financial transactions (and regulation of the same).

Markets in Crypto Assets — MiCA

The European Commission is currently considering wide ranging changes to existing financial services laws to capture technology changes arising from blockchain and DLT, including:

- amendments to MiFID II to clarify the circumstances in which crypto-assets qualify as ‘financial instruments’;

- creating a regime for distributed ledger technology (DLT) securities tokens; and

- establishing a bespoke new regime for crypto-assets not covered under existing regulation (e.g. stablecoins, payment tokens and utility tokens).

In respect of 3. the Commission state in a draft EU wide Regulation:

“This proposal, which covers crypto-assets outside existing EU financial services legislation, as well as e-money tokens, has four general and related objectives.

The first objective is one of legal certainty. For crypto-asset markets to develop within the EU, there is a need for a sound legal framework, clearly defining the regulatory treatment of all crypto-assets that are not covered by existing financial services legislation.

The second objective is to support innovation. To promote the development of crypto-assets and the wider use of DLT, it is necessary to put in place a safe and proportionate framework to support innovation and fair competition.

The third objective is to instil appropriate levels of consumer and investor protection and market integrity given that crypto-assets not covered by existing financial services legislation present many of the same risks as more familiar financial instruments.

The fourth objective is to ensure financial stability.”

The proposed MiCA Regulation includes strong sanctions (e.g. name and shame, profits disgorgement and administrative fines of up to 15% of turnover) for breach. However, the benefit of a harmonised framework to access the whole EU market are significant.

The UK Financial Conduct Authority (FCA), the European Securities and Markets Authority (ESMA) and the European Banking Authority (EBA) have looked at some of these issues already (see FCA guidance on crypto-assets, ESMA’s advice on initial coin offerings and crypto-assets & EBA’s report with advice for the European Commission on crypto-assets). In addition, in May 2020 the European Central Bank (ECB) issued a good technical paper on global stablecoins.

Given the scope of MiCA this article can not consider more than a small part of its intended application, particularly as it impacts stablecoins, but the impact on so called initial coin offerings will be very significant (including in respect of utility tokens).

With MiCA, the European Commission intends to include stablecoins within the scope of the bespoke MiCA regime on crypto-assets (to the extent not already regulated) and to modify the e-money regime to include a new type of e-money:

“‘electronic money token’ or ‘e-money token’ means a type of crypto-assets whose main purpose is to be used as a means of exchange and that purports to maintain a stable value by being denominated in (units of) a fiat currency”

Other stablecoins are likely in scope as ‘asset-referenced tokens’, defined in the draft Regulation as:

“a type of crypto-assets whose main purpose is to be used as a means of exchange and that purports to maintain a stable value by referring to the value of several fiat currencies, one or several commodities or one or several crypto-assets, or a combination of such assets”

For stablecoins that do not fall within the above definition or the e-money token definition i.e. algorithmic stablecoins the issuers must still publish a white paper, notify the regulator and may not refer to their coins as being ‘stable’:

“So-called algorithmic ‘stablecoins’ that aim at maintaining a stable value, via protocols, that provide for the increase or decrease of the supply of such crypto-assets in response to changes in demand should not be considered as asset-referenced tokens, as long as they do not aim at stabilising their value by referencing one or several other assets.”

Once implemented, stablecoin (being a type of ‘asset-referenced token’) issuers not already regulated as credit institutions or e-money institutions will now need to be authorised and to publish a white paper approved by their home state regulator (in principle this is similar to the prospectus obligations for public offers of securities).

Interestingly, issuers of ‘significant e-money tokens’ and ‘significant asset-referenced tokens’ will be directly regulated by the EBA rather than national regulators and will have additional obligations in respect of capital, interoperability and liquidity management. Libra Coin is therefore likely be regulated by the EBA if it establishes itself within or markets its services within the Union.

The proposed territorial scope of MiCA requires either a European establishment or some solicitation or targeting of EU customers.

Whilst the focus here is EU law, in the USA regulatory acceptance of stablecoins continues to develop. The Office of the Comptroller of the Currency (OCC) states that US national banks and federal savings associations are now officially permitted to engage with fiat-backed stablecoins. The Securities and Exchange Commission (SEC) also released a statement stating that stablecoins are not necessarily securities and supporting the OCC position. In an interpretive letter by the OCC, US banks can provide “services in support of a stablecoin project,” which may include holding stablecoin reserves, as long as the bank has “instituted appropriate controls and conducted sufficient due diligence” and in situations where the coins are held in “hosted wallets.”

Gibraltar has been a pioneer within Europe in the regulation of DLT for some time.

A deeper dive

To understand how DeFi shakes up existing models for intermediation, and presents new challenges for financial market regulators, I am going to look at three well known examples:

- MakerDao’s Dai crypto collateralised stablecoin

- Facebook Libra payment and fiat backed stablecoin project

- Synthetix derivatives platform

This summary concludes with some thoughts on the future role of regulators in a DeFi world.

1. Makerdao Dai

I have previously published a series of articles that looked at the rise of stablecoins and in that I considered the novel stablecoin Dai.

In brief, the Dai is an ERC-20 protocol operated by Makerdao, a decentralised autonomous organisation (DAO). This is intended to mean that all of the developers and promoters are able to agree how to manage how the protocol works given the intended use-cases for Dai based on their holdings of a governance token — i.e. it is not centrally controlled and managed by a legal ‘person’.

Dai is an ethereum based smart contract which collateralises crypto assets (originally ETH only) holdings in a wallet using a smart contract (the assets are locked-up for collateralisation purposes only and are not deposited i.e. transferred to a financial institution or company). Dai is not therefore backed by fiat reserves held in a bank unlike many other stablecoins. The current position of all dai contracts can always be be seen on-chain and independent audit is not required.

A person acquiring dai enters into a smart contract called a Collateralized Debt Position (CDP) which ascertains the current value of their locked assets and then provides the maximum Dai ‘loan’ available (currently 1:1.5 of assets collateralised — so a Dai purchase of $100 would require, e.g., ETH of $150 in collateral) and the price at which the repayment obligation would be automatically triggered (liquidation price) unless further collateral is locked up to maintain the collateralisation ratio.

The protocol uses a ‘Stability Fee’ as the charge for having an open CDP and this charge pays for the protocol’s operation and can also be used to encourage the issuing and redemption of Dai by making it cheaper or more costly to have open CDPs.

Under the Dai structure governance is managed by MakerDao and they do this ostensibly using a governance token (MKR) which is separate to the Dai tokens. The MKR token holders also act as the guarantors of the stability of the system in times of systemic stress (sort of like a lender of last resort).

During good times the MKR holders benefit from activity on the protocol since the stability fee is being used to acquire MKR tokens in circulation (providing demand for MKR) but in the event of a catastrophic event (flash crash) requiring additional liquidity new MKR would be be issued and sold to meet CDP contract obligations where a1:1 ratio was breached i.e. the ETH held as collateral was realised below the price of the Dai issued against it. The backstop function would push the price of MKR down and act as a dilution for existing holders.

The Dai structure also requires the use of automated trading bots (Keepers) to arbitrage away any premium or discount from the $1 peg to help maintain price stability. A Keeper is “an independent (usually automated) actor that is incentivized by arbitrage opportunities to provide liquidity in various aspects of a decentralized system. In the Maker Protocol, Keepers are market participants that help Dai maintain its Target Price ($1): they sell Dai when the market price is above the Target Price, and buy Dai when the market price is below the Target Price.”

Keepers also participate in auctions of ETH from any liquidated CPDs but in times of great stress their role in maintaining the peg and in acting as buyer of liquidated ETH comes into question. In addition, the reliance on the Ethereum network (which is still pending major upgrades to support greater transaction speed and capacity) means that any bandwidth problems on the ethereum network make it very hard for the Makerdao protocol to function effectively (i.e. liquidate in time or sell eth quickly or at market price).

Makerdao does have a number of issues that arise from its decentralised nature:

- Governance: there continues to be concerns about the lack of transparency in the running of the project and the role of key senior people within the project vs the role of MKR holders (see: Foundation plots its own demise).

- Price Stability: Dai continues to struggle to maintain a consistent peg (e.g. a variance less than 1–2%) against the dollar (see https://defirate.com/makerdao-shutdown-concerns/ and https://www.coindesk.com/makerdao-defi-dai-broken-peg).

Brief UK & European regulatory analysis of Makerdao Dai

Makerdao Dai is almost impossible to classify within existing financial services regulatory frameworks in the UK & Europe.

The Dai lending platform is fascinating because it does not fall within the regulatory regime that would most likely be applicable namely a consumer credit (B2C) provider or a P2P lending platform facilitator. This is both because of its DAO structure but, more importantly, because with Dai the organisation facilitating the collateralisation of assets is not the lender and the CPD structure does not intermediate two parties to a loan – there is in effect no ‘person’ acting as the lender under the maker protocol.

From a credit regulation perspective, it is very difficult to understand how a regulator could apply regulatory powers and supervisory capability to a technology protocol that enables lending against assets without a lender (i.e. based almost entirely on an aggregate market value of assets mediated by way of a smart contract only).

It is however possible that the Makerdao Dai would fall within the proposed new EU MiCA regime as an ‘asset-referenced token’ — though there is a credible position that it is algorithmic since the collateral and the price of the token are only indirectly related (it is not a 1:1 peg based on movements in an underlying crypto asset).

EU MiCA regulation will apply to existing stablecoins already issued and widely in use in the market if there is a sufficient European nexus. However, Makerdao may be deemed to be responding to EU end user interest only and not carrying out advertising and marketing within the EU i.e. it may remain outside of its territorial scope.

In the case of the maker protocol the defence to arguments about potential regulatory supervision as a credit product is less about de-centralisation per se and more about the underlying nature of the loans and the coins. This means that Makerdao does not need to prove it is a sufficiently decentralised DAO to fall outside of the regulation of certain credit platforms and operators. It just needs to show it is not a lender and nor does it intermediate lending and borrowing between legal persons (a smart contract and a crypto wallet are not legal persons).

2. Libra

The Libra Association, which is linked to Facebook, have been developing a multi-asset token which allows one or more cash and cash equivalent assets to be used within a protocol. The intention is to provide easier and cheaper payments and settlement including to people where banking services are very limited and cross-border payments are difficult.

Their ambition is to enable “a simple global payment system and financial infrastructure that empowers billions of people…Our objective is for the Libra payment system to integrate smoothly with local monetary and macroprudential policies and complement existing currencies by enabling new functionality, drastically reducing costs, and fostering financial inclusion.”

In the evolution of Libra it has become clear that the global power and consumer reach of Facebook, and the market strength of Libra members, means that their ambition to create a new global payments system is being taken very seriously. There has been considerable nervousness by Governments and central banks who do not wish to have a competitive global currency outside of their control or that of the IMF (with its multi-currency Special Drawing Rights).

Libra have also apparently applied for for a payment system license from the Swiss Financial Market Supervisory Authority (FINMA).

In 2020, Libra published a revised white paper to try to deal with many of the concerns being raised. In it they state:

“Four key changes have been made to address regulatory concerns that deserve specific attention, each of which is addressed briefly below and then in more depth in the updated white paper:

Offering single-currency stablecoins in addition to the multi-currency coin.

Enhancing the safety of the Libra payment system with a robust compliance framework.

Forgoing the future transition to a permissionless system while maintaining its key economic properties.

Building strong protections into the design of the Libra Reserve.”

It seems clear Libra are now saying to central banks: let us manage the cross-border issuance, technology, clearing and settlement issues for digital use of your fiat currencies. This also ties in well to developments of central bank digital currencies.

So what is it?

In its current form Libra is intended to be a number of tokens (Libra Coins) representing underlying “cash or cash equivalents and very short-term government securities denominated in the relevant currency” and the Coins can either be single currency or multi-currency backed Coins:

“….While our vision has always been for the Libra network to complement fiat currencies, not compete with them, a key concern that was shared was the potential for the multi-currency Libra Coin (≋LBR) to interfere with monetary sovereignty and monetary policy if the network reaches significant scale and a large volume of domestic payments are made in ≋LBR. We are therefore augmenting the Libra network by including single-currency stablecoins in addition to ≋LBR, initially starting with some of the currencies in the proposed ≋LBR basket (e.g., LibraUSD or ≋USD, LibraEUR or ≋EUR, LibraGBP or ≋GBP, LibraSGD or ≋SGD).,,,≋LBR will not be a separate digital asset from the single-currency stablecoins. Under this change, ≋LBR will simply be a digital composite of some of the single-currency stablecoins available on the Libra network. It will be defined in terms of fixed nominal weights, such as the Special Drawing Rights (SDR) maintained by the International Money Fund (IMF).”

The European Union have previously expressed significant concerns about the impact Libra could have on financial markets and it is clear that they are trying to work out how it should be regulated. The most obvious existing regulatory framework for a fiat backed stablecoin is the e-money regime (in the US this is often called prepaid).

Under European law (Directive 2009/110/EC) e-money is:

“electronically, including magnetically, stored monetary value as represented by a claim on the issuer which is issued on receipt of funds for the purpose of making payment transactions as defined in point 5 of Article 4 of Directive 2007/64/EC, and which is accepted by a natural or legal person other than the electronic money issuer”

The FCA in the UK have advised that in their opinion many forms of fiat backed stablecoin could fall within this existing regulatory framework that effectively covers money deposits used to make payment transactions that can not be used for credit creation (i.e. outside of the fractional reserve banking system).

“We have observed tokens in the market where there are attempts to stabilise their value using a variety of mechanisms. These tokens are commonly referred to as ‘stablecoins’. However, while they may have a common purpose, they vary greatly in their structure and arrangement, making them inappropriate for any single classification. Therefore, not every ‘stablecoin’ will meet the definition of e-money, or a security token. For instance, it may be a derivative, a unit in a collective investment scheme, a debt security, e-money, or another type of specified investment. Or, it might fall outside our remit.

Many tokens are “backed with” fiat currencies, most commonly the United States Dollar (USD), but we have seen tokens backed with other fiat currencies, including the British Pound (GBP) or a basket of currencies. In some cases, this involves the issuer “pegging” the value to that currency — i.e guaranteeing the value of the token, while holding a reserve of fiat currency(ies) to ensure it can meet any claims. In other cases, the token gives the token holder an interest or right to the custodied fiat currency(ies), with the value of the tokens being directly linked to the value of the fiat currency held.”

However, currently the e-money test must be met:

“For example, a token that is backed with fiat currency, but can only be spent with the issuer will not constitute e-money, as it is not accepted by a person other than the issuer”

Libra state:

“The assets comprising the Reserve will be held by a geographically distributed network of well-capitalized custodian banks to provide both security and decentralization of the assets. Libra Networks will not directly interface with consumers, but will instead partner with a select number of Designated Dealers to extend liquidity to consumer-facing products, such as wallets and exchanges.”

So a token that is fiat backed but (i) is not accepted by third parties for payment transactions or (ii) such a token that does not represent a claim against the issuer falls outside of the current e-money regime. The new wider proposed definition of ‘e-money token’ in MiCA means that Libra is likely in scope once the new regime is implemented notwithstanding technical issues around who it is issued to and redeemable by and Facebook appear to have encouraged the proposed new regulatory regime for stablecoins.

It appears that Libra see themselves mostly as a payment network that allows settlement of liabilities between a variety of market operators without themselves acting a regulated financial institution for end-users. This is not unlike the situation that has persisted with MasterCard and Visa.

It is also likely Libra meets the definition of a payments system, which in the UK is defined as:

“a system which is operated by one or more persons in the course of business for the purpose of enabling persons to make transfers of funds, and includes a system which is designed to facilitate the transfer of funds using another payment system.”

Under EU law a payment system is defined as:

“a formal arrangement between three or more participants, not counting possible settlement banks, central counterparties, clearing houses or indirect participants, with common rules and standardised arrangements for the execution of transfer orders between the participants”

3. Synthetix

Synthetix allows users to create tokens and trade in a synthetic manner on specified real world assets using ERC-20 tokens. Currently these are cryptocurrencies (long and short), commodities, market indexes and forex.

These tokens are called synthetic assets (aka “Synths”). They can track the price of a range of underlying assets such as stocks, currencies, and commodities.

Synths are intended to allow a wide range of derivative type trading. The intention being to track, short or outperform price action in the underlying asset. At the moment they also offer binary options and they are currently developing the capability to offer futures and leveraged trading.

Synthetix effectively works using shared collateral pools and settlement of debt positions on a global debt register, the benefit :

“is that Synths can be converted between different flavours without a counterparty. The pool of all collateral holders essentially acts as the counterparty. So someone holding sUSD can convert that Synth into sAUD at the current exchange rate without needing to find someone who is holding sAUD to trade with. This, combined with our Synthetix.exchange platform, will allow users to quickly swap between different commodities and fiat currencies, paying only for gas and the Synthetix Network fee….So for example, if Alice mints the first sUSD she will represent 100% of the system. If Bob then mints the same amount of sUSD he will represent 50% of the debt in the system. In order to determine Alice’s debt when she wants to leave the system, we simply look at the cumulative change in debt since she entered the system and we apply this to her original percentage of the total debt.

So while Alice may have initially represented 100% of the debt, after hundreds of other SNX holders have issued she may only represent 1% of the debt. In order to determine Alice’s debt when she exits we simply take all of these changes and total them and then find her current debt percentage. Once we know this and the total network debt we can determine her debt obligation in Synths to exit the system and unlock her SNX.”

Given that Synths are intended to track the price in underlying assets the protocol relies upon Oracles that use an algorithm that determines the price of an asset pulling data from various specified sources. Oracles therefore determine the value of Synths (since they move in relation to change in the underlying).

- Synthetix utilizes a SNX token as collateral to mint Synths.

- All Synths are overcollateralized at 800%.

- Transaction fees on Synthetix’s DEX go to SNX holders and Synth minters.

“Synths are minted when SNX holders stake their SNX as collateral using Mintr, a decentralised application for interacting with the Synthetix contracts….SNX holders are incentivised to stake their tokens and mint Synths in several ways. Firstly, there are exchange rewards. These are generated whenever someone exchanges one Synth to another (i.e. on Synthetix.Exchange). Each trade generates an exchange fee that is sent to a fee pool, available for SNX stakers to claim their proportion each week. This fee is between 10–100 bps (0.1% — 1%, though typically 0.3%), and will be displayed during any trade on Synthetix.Exchange. The other incentive for SNX holders to stake/mint is SNX staking rewards, which comes from the protocol’s inflationary monetary policy.”

It should also be noted that in respect of its binary options service they use a pari-mutuel structure which also avoids the need to match counterparties. All trades/bets go into a pool, and the pool is shared equally between those who make the winning selection.

Outside of Europe, there is a regulatory question as to whether these binary options would constitute regulated online gambling in some jurisdictions (in the UK binary options are regulated by the FCA and not the Gambling Commission as in the EU it is a regulated financial service activity). A previous ESMA ban on the offer of any binary options to retail customers has been implemented on a national basis across Europe.

Brief UK & European regulatory analysis of Synthetix

The regulatory analysis for Synthetix is very complicated since the activity of arranging the creation and trading of some derivatives is substantially regulated in the UK and Europe.

For the layperson it is worth highlighting an important distinction here. A digital asset may be entirely unregulated in its simple form, such as is bitcoin, in many jurisdictions.

However, when a person enables derivative contracts to be put in place in respect of an unregulated underlying asset, the packaging or creation of bilateral assets and liabilities related to movements in the unregulated underlying can itself be a regulated activity. That means the secondary market activity can be regulated notwithstanding that trading in the primary underlying asset is unregulated.

That said, it must also be pointed out that the mere bundling of digital assets together does not make them a regulated derivative contract:

- this means that a smart contract that entitled the possessor to ownership of a number of other digital assets (such as an index basket token) is not, in itself, thereby a regulated commodity contract; BUT

- depending on the structure (particularly if there is pooling and central management), such a product could be a regulated collective investment scheme or Alternative Investment Fund (within Europe) and could also fall within the proposed Markets in Crypto Assets regime.

Within Europe, the primary law that deals with whether a packaged derivatives product is a regulated derivative contract is the Markets In Financial Instruments Directive (MiFID) and associated legislation — these consist of a directive (MiFID 2) and a regulation (MiFIR). There is also subsidiary regulation such as the Commission Delegated Regulation 2017 that provides further guidance on in and out of scope derivative contracts.

Derivatives are defined in MiFID 2 as follows:

“(49) ‘derivatives’ means derivatives as defined in Article 2(1)(29) of Regulation (EU) No 600/2014;

(50) ‘commodity derivatives’ means commodity derivatives as defined in Article 2(1)(30) of Regulation (EU) No 600/2014;”

Under EU law, regulated derivatives includes:

“Options, futures, swaps, forward rate agreements and any other derivative contracts relating to securities, currencies, interest rates or yields, emission allowances or other derivatives instruments, financial indices or financial measures which may be settled physically or in cash”

It is a matter of legal irony that the definition of the term ‘derivative’ must itself be derived and is not clearly specified. As there is no technical definition of ‘derivative’ under European law it follows that the definition is more of a market term i.e. those things that the markets and its regulators generally consider to be regulated derivatives are in scope and those they do not are unlikely to be derivatives absent clear regulatory guidance.

A contract that enabled a person to enter into a bilateral arrangement with another persons so as to trade, hedge or speculate on changes in an underlying digital asset could easily fall within the widely defined scope of derivatives. However, a contract (including a smart contract) that allowed a person access or to collateralise an underlying digital asset itself would not normally be considered a derivative contract within the meaning of that term in the financial markets.

For a good examination of the potential applicability of MiFID to cryptocurrency derivatives and commodities see the paper written by the Autorité des marchés financiers (AMF) in which they conclude:

“In conclusion, a cash-settled derivative whose underlying is a cryptocurrency can be considered to be a financial contract. Consequently, the regulations applicable to the marketing of financial instruments in France apply to cryptocurrency derivatives.”

Note the AMF take the view that settlement in crypto rather than cash does not affect this legal classification. The AMF do however allow for the possibility of physically settled crypto derivative contracts to be commercial contracts and not finance instruments i.e. to be out of scope.

In respect of the definition of ‘derivative’ contracts, ESMA is primarily responsible for providing clarity on these definitional matters. The Delegated Regulation (COMMISSION DELEGATED REGULATION (EU) 2017/591 of 1 December 2016) is also helpful in determining the meaning of commodity derivative contracts.

Is Synthetix regulated within Europe and the UK?

Assuming that many of the contracts traded on the Synthetix platform are considered cash-settled regulated derivative contracts subject to MiFID the question remains whether, even with that major assumption, the organisers of the platform are required to be regulated.

MiFID covers a wide range of operators that facilitate trades in regulated financial instruments. The most relevant for our purposes are Organised Trading Facilities (OTF). An OTF:

“is a multilateral system, which is not a regulated market or MTF and in which multiple third party buying and selling interests in bonds, structured finance product, emissions allowances or derivatives are able to interact in the system in a way which results in a contract….The creation of the OTF category was expected to bring systemic benefits, in particular aid the price formation process in bonds and derivatives as well as enhance the resilience of the systems being used for the trading of these instruments.

The conception for OTF is broad and includes a multitude of electronic platforms that were not so far subject to requirements applied to regulated markets and MTFs, for this reason an OTF is often perceived as a catch-all category of a trading venue.” (https://www.emissions-euets.com/trading-venues/organised-trading-facility-otf)

The UK financial services regulator (the FCA) have stated that:

However, this then gives rise to the question as to what is a multilateral system?

The FCA stated in a Consultation Paper on the MiFID II implementation (CP15/43):

“Multilateral systems may be contrasted with ‘bilateral systems’ where an investment firm enters into every trade on own account. […] Any system or platform is a multilateral system where more than one market participant has the ability to interact with more than one other market participant on that system or platform”

Article 4(19) of MiFID II defines a multilateral system as:

“any system or facility in which multiple third-party buying and selling trading interests in financial instruments are able to interact in the system”.

Whilst this definition is very broad it is not clear whether a system can be considered a multilateral system unless it involves a degree of facilitation and execution of matching trades between counterparties and the Synthetix venue is not, at least currently, a system to match trades between individual participants. However, the ban on binary options for retail customers in Europe clearly shows the regulatory intention is to prohibit such retail activity (and I would expect howsoever it is structured).

The argument against regulation for Synthetix under the current financial services frameworks is that:

(i) the smart contracts used to collateralise the derivative products are not a standard P2P contract — instead the person creating a Synth is lending against their own collateral and creating their own derivative contract. Whilst there are elements in its offering which may fall within a P2P analysis, mostly the trading is not strictly speaking P2P or bilateral. Legal questions remain in respect of its multi-lateral nature.

(ii) there is no centralised operator of a platform to arrange trades in the financial instruments. This is the DAO argument.

The complexity and range of the offering on the Synthetix platform, the regulated nature of many derivative contracts and the wide definition of an OTF means that the Synthetix team must defend themselves from regulatory attack by arguing strongly that they are not a person operating a trading venue or arranging deals in financial instruments.

This requires robust decentralisation in terms of governance, custody of assets, profit sharing, day to day management and all of the other aspects of an enterprise like this that is normally conducted using a regulated limited liability corporate vehicle.

Synthetix is holding almost $460 million in assets in its smart contracts, up more than 20x from a year ago, according to DeFi Pulse, and its token SNX is up more than 10x in that time to $3.2.”

The argument of decentralisation is also very important in the US albeit in a slightly different context relating to security tokens. The term, “sufficiently decentralized,” was minted by the SEC’s William Hinman in respect of the Howey Test in 2018. The Howey Test is very important for persons operating a token sale or offering to consider whether their token is a security. Hinman stated that if a network was “sufficiently decentralized…where purchasers would no longer reasonably expect a person or group to carry out essential managerial or entrepreneurial efforts….[then] regulating the tokens or coins that function on them as securities may not be required.”

In summary, the Synthetix platform does appear to potentially offer a multi-lateral trading venue for derivative contracts that could be considered within the scope of MiFID i.e. enabling multiple parties to buy/sell derivatives in a manner designed to result in binding contracts. However, the absence of matching individual participants in a trade and the algorithmic nature of the trades complicate this picture and mean it could still be outside of scope depending on the interpretation of each Member State regulator, national law and ESMA. EU law is also very fragmented and much in need of updating in respect of the definition and supervision of regulated derivatives.

In addition, the lack of a legal person operating the trading venue would make the regulation or prohibition of the platform very difficult and, to the extent that the regulators wish to capture it, will require looking through the DAOs for one or more individuals that the regulator believes is the effective controller of the venue. Failing that it is difficult to see what regulators can do other than an outright ban on such a platform and product (with all of the novel difficulties that arise from seeking to prohibit smart contract interactions and settlements not mediated through financial institutions).

To the extent that Synthetix is used to create asset-referenced tokens (including stablecoins) then, subject to consideration of whether they are potentially algorithmic tokens, it could be fully within scope of the proposed EU MiCA regime subject to territoriality requirements.

4. Future role of regulators in a DeFi world

The proposed MiCA changes in Europe are welcome in principle as they seek to reflect the need to deal with risks arising from rapid technological changes in the e-commerce, securities, trading and payments spaces.

However, with an increased use of DAOs, regulators will also need to approach the risks in DeFi in newer ways. Instead of always seeking to define the regulated activity and then the regulated person, they must consider how to regulate against negative outcomes even when there is no legal ‘person’ obviously responsible — doing this will require regulation or oversight on a more exceptional basis (i.e. responding to the risk of market harm to consumers) and this will present legal issues for the regulator unless they have clear super-powers to prevent harm to consumers (which they often do) and strong technical skills. As we are dealing with online activity, issues of territorial scope and enforcement will also always remain.

A regulator might wish to take steps to prevent a change in the code base for a protocol or even banning the use of a protocol in its territory based on the risk of significant harm to consumers (e.g. the developers seek to remove assets or unfairly devalue assets that were supposed to be protected for the benefit of the users of the protocol). Leaving aside the great and fascinating difficulties in enforcing changes or bans of decentralised protocols and smart contracts, this type of approach will require a restructuring of existing regulatory functions, tech resources and human resource capability with high tech rapid response units keeping track of DeFi markets and trying to step in when they deem it prudent.

It is likely that the arms-race between regulators and DLT technologists and entrepreneurs will accelerate. Regulated entities will be expected to police fiat on and off ramps and some of the activities taking place elsewhere on-chain but end users will expect to be able to use their wallets and smart contracts as they see fit (subject to normal human decency) i.e. a degree of freedom, discretion and privacy. The continued use of advanced sophisticated DAOs will also make application, interpretation and enforcement of the law difficult.

DeFi also requires a degree of pragmatism in recognising the appropriate limits of the potential for regulatory oversight when sophisticated consumers collateralise their crypto assets to trade exotic or higher risk products using smart contracts. For example, see the new SEC approach to whom is an accredited investor which now takes into account product knowledge and experience.

Perhaps advanced crypto end-users are not the average relatively unsophisticated (from a product perspective) man or woman on the street the regulator is tasked with protecting. Absent aggravating circumstances (e.g. bad faith use for money laundering, trafficking, child crimes and tax evasion) genuine DAO platforms used by good faith end users should not be prioritised for regulatory intervention or sanction.

Questions:

Will we end up with different prices for the same coins and tokens depending in the journeys through cryptoland they have undertaken?

Will use of a wallet for unregulated products and services make it difficult to use your wallet for regulated activities?

Will people keep different wallets for use in these different domains?

Are we moving towards a world where the only easy to conduct activities are Govt regulated activities?