Payments in 2025 will be shaped by AI, instant payments, CBDCs, embedded finance, and sustainability.

The payments industry in 2024 saw rapid evolution, marked by the growing adoption of real-time payments, advances in AI-driven fraud detection, and significant progress in Central Bank Digital Currencies (CBDCs). These developments have set the stage for an even more dynamic year ahead as technology continues to reshape how businesses and consumers interact with payments.

As competition intensifies and regulatory landscapes shift, staying ahead of emerging trends has never been more critical. Understanding what’s on the horizon in 2025 will help payments professionals anticipate changes, seize opportunities, and navigate challenges in a fast-paced ecosystem.

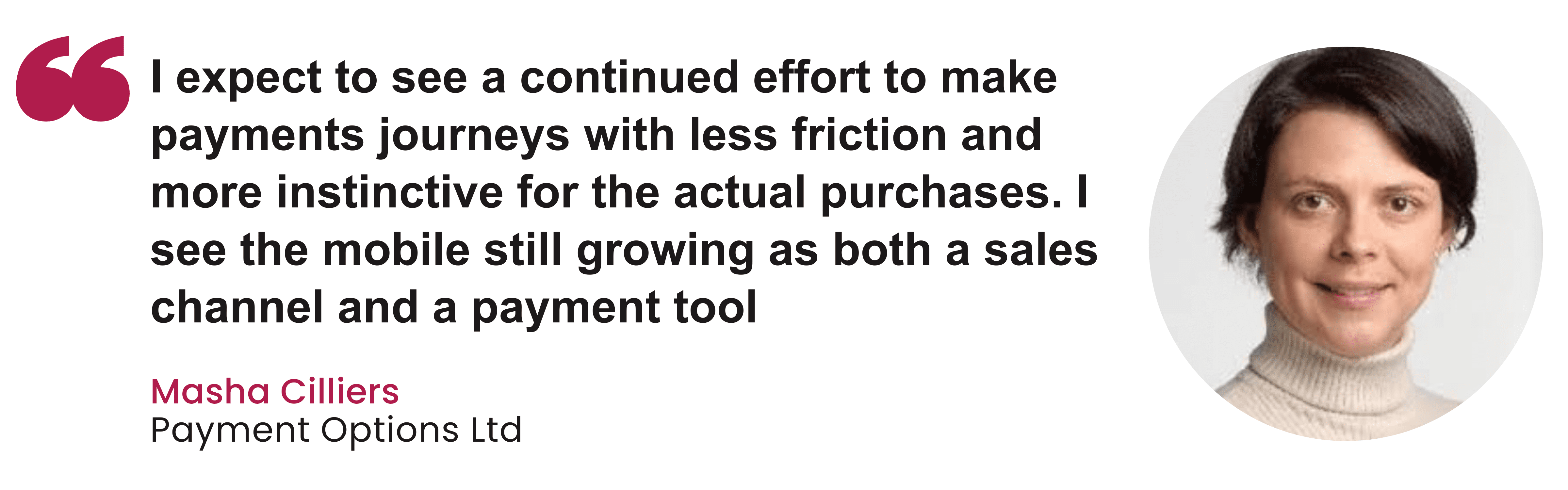

Businesses are prioritising smoother, more intuitive payment experiences to meet consumer expectations. According to Masha Cilliers, Founder and Principal Consultant at Payments Options, the focus in 2025 will be reducing friction in payment journeys and ensuring they align with specific customer needs.

Cilliers added that she expects businesses to pay further attention to the orchestration or architecture of their payment process—not only to include the ‘trendy’ payment choices but to do so in a clever way which makes the most sense for each business.

Rather than a fully converged ecosystem, Cilliers predicts an increasingly competitive market where payment methods will continue to vie for dominance. This competition is shaping a dynamic landscape, from cards competing with instant payments to wallets facing off against real-time transfers.

“The market is huge and now recognised as such, so there’s a lot more interest in investing and succeeding in it,” she explained. “For example, cards versus instant payments, wallets versus real-time transfers, BNPL versus store credits, and other financing options.”

Semper Advisory Ltd Director Simon Burrows says: “I’ve always said that changes to the payments landscape are evolutionary, not revolutionary, and are almost always driven by user adoption rather than being mandated centrally. In 2025, I think Open Banking (which really needs a new name) will continue building rapid momentum as businesses and consumers adopt new use cases and look to avoid high and value-based interchange fees.

“Business banking and payments are still antiquated, but digital payment methods will continue to grow as more companies adopt cloud-based systems and off-the-shelf payment and treasury management solutions.”

Widespread adoption of embedded finance

Embedded finance is rapidly reshaping the payments landscape, enabling non-financial companies to integrate seamless financial services directly into their platforms. This shift is more than just a trend—it’s a game-changer for how businesses interact with customers, creating entirely new revenue streams and transforming the customer journey. It’s growing as a sector. Embedded Finance’s market value in the United States is projected to surge to over $230 billion by 2025, according to data from Lightyear Capital.

By embedding financial services, businesses can offer experiences beyond simple transactions. For example, retailers can introduce tailored financing options like buy-now-pay-later (BNPL) directly at checkout, boosting sales conversion rates while improving accessibility for customers. Similarly, travel companies can bundle payment plans or insurance options within booking platforms, ensuring a frictionless and all-inclusive customer experience.

The impact on customer loyalty is profound. With embedded finance, brands can maintain control over the customer relationship, offering convenience that keeps users engaged and reduces the risk of losing them to external payment providers. According to recent studies, 85% of European firms view embedded finance as a critical metric for success in retaining front-end customer interactions and increasing brand touchpoints.

Moreover, this model is driving innovation in sectors like healthcare and logistics, where integrated payment solutions are streamlining processes and making services more accessible. Businesses that adopt embedded finance strategically can position themselves as indispensable parts of their customers’ daily lives.

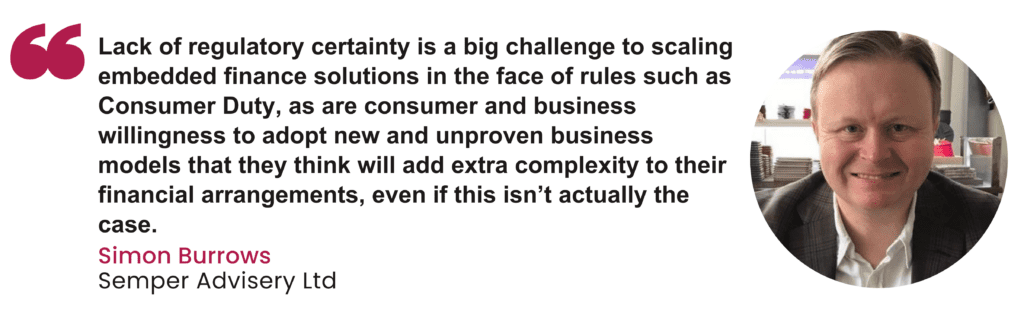

To unlock this potential, companies must focus on partnerships with technology providers that ensure scalability and compliance. However, the challenge of navigating complex regulatory requirements remains significant. As Cilliers explains: “The largest challenge is understanding the regulation and finding regulated partners to guide your company in building compliant and profitable embedded finance solutions.”

Embedded finance is not just about adding payment options—it’s about reimagining how businesses serve their customers and create value. Those who invest in its potential now will secure a competitive edge in an increasingly interconnected financial ecosystem.

Burrows believes there will be an increase in “new and interesting” examples of embedded finance in the coming months, however providers should continue to be “extremely wary of the potential regulatory challenges that may emerge”. “I believe the combination of embedded finance and Open Banking (both Account Information and Payment Initiation services) will drive more new ways of doing things,” he adds.

Accelerated use of AI in payments

Artificial Intelligence (AI) has quickly become a cornerstone of payment operations over the past 12 months, and its influence is expected to grow further in 2025. Enhancing everything from fraud prevention to personalised payment experiences. As payment providers and businesses harness AI’s potential, they are unlocking faster, smarter, and more secure ways to serve their customers.

A survey conducted this year indicates that 85% of senior payment professionals identified fraud detection as the most significant use case for AI, aligning with the banks’ focus on implementing generative AI for improved fraud detection and securing payment data.

One of AI’s most transformative roles is in fraud detection and prevention. By analysing vast amounts of transaction data in real-time, AI can identify unusual patterns and flag potential threats with far greater speed and accuracy than traditional systems. This reduces losses for businesses and builds consumer trust in payment platforms.

On the growth and potential of AI, Cilliers said: “I am particularly excited in leveraging AI for fraud management to help find patterns before they become a bigger problem for your company. That includes both first and third party fraud. I would like to see more AI use in building instinctive and contextual checkout process for each customer, but I think that this is a longer term task.”

AI is also revolutionising customer engagement. Payment providers are using machine learning to deliver tailored experiences, such as personalised payment plans, dynamic offers, or AI-driven customer support. These innovations strengthen user loyalty and drive higher conversion rates.

Moreover, AI is enabling greater efficiency in cross-border payments, addressing pain points like delays and high costs. The power of AI in helping to optimise processes and reduce manual intervention is also a trend expected to continue into the next year.

As adoption accelerates, businesses that leverage AI effectively will be able to innovate faster, respond to threats more proactively, and meet evolving customer expectations in an increasingly competitive marketplace.

Burrows backs “AI to shift the needle in fraud prevention”, and significantly improve the quality and speed of analysis at scale. “This will be counter-balanced by additional fraud created by those AI algorithms. It will be fascinating to watch the battle of the algorithms, but the industry must not forget the real-world consequences of fraud and its negative impact on people’s lives,” he says.

“Superficially the overall customer experience in payments should improve thanks to AI, however, when things go wrong, the impact may well be magnified particularly with the additional complexity of trying to obtain support from a real person rather than a bot,” he explains.

CBDCs continuing to gain traction

Central Bank Digital Currencies (CBDCs) are set to take a significant step forward in 2025, as more countries move from pilots to implementation. With major economies like the EU, China, and India leading the way, CBDCs are reshaping the payments landscape by introducing government-backed digital currencies designed for greater efficiency, inclusivity, and control.

The development of CBDCs is a long-term trend, with many projects not expected to be completed until 2026 or later. For example, the digital euro is projected to launch between 2026 and 2029.

For payment providers, CBDCs present both opportunities and challenges. On one hand, they could streamline cross-border transactions, reducing costs and settlement times. On the other hand, they may disrupt existing payment infrastructures, requiring firms to adapt their systems and develop new strategies to remain relevant in a CBDC-driven world.

Cilliers believes the excitement around CBDCs, especially across the Atlantic is justified. “I am looking forward to seeing how that translates in specific and easy to understand use cases here,” she said. On the potential challenges of implementation, she added: “The challenge with the regulation is that it can vary hugely geographically, so finding interoperability of business models is currently a big problem in my mind.”

Central banks view CBDCs as promising for improving cross-border payment efficiency, potentially outweighing other innovations like linking real-time payment systems or using stablecoins.

Additionally, CBDCs promise to enhance financial inclusion by providing unbanked populations with direct access to digital payment systems, bypassing traditional banking requirements. This could open new customer segments for innovative firms ready to support CBDC adoption.

Businesses that stay informed about regulatory developments and assess how CBDCs will integrate into their services will likely be the first to benefit from the trend.

Sustainability in payments to become a prime focus

Sustainability is no longer a niche concern—it’s becoming a defining priority for the payments industry. In 2025, firms will face increasing pressure from consumers, investors, and regulators to adopt environmentally friendly practices and demonstrate their commitment to reducing carbon footprints.

The growth of sustainable solutions in payments and consumer demand for businesses to adopt them in the finance industry is expected to continue rising in 2025 and beyond. Major banks like Barclays, BBVA, and HSBC are responding by making significant commitments to sustainable financing, with Barclays aiming to facilitate 150 billion British pounds in social and environmental financing by 2025.

Payment providers have responded to the demands of consumers by introducing innovative solutions, such as biodegradable or recycled payment cards, and embedding carbon-tracking tools within digital payment platforms.

Moreover, the industry is exploring greener technologies, such as blockchain networks with lower energy consumption, and optimising operations to minimise waste. These efforts align with growing regulatory demands for environmental transparency and compliance, creating both challenges and opportunities for businesses.

Sustainability initiatives also offer competitive advantages. Companies that take proactive steps toward eco-conscious practices can enhance their brand reputation and attract a growing segment of environmentally aware customers.

This is exemplified in South America especially, specifically Peru, where 86% of consumers valued ethical and environmentally brands in March. As sustainability continues to gain momentum, payment firms must embed it into their strategies to stay ahead in a rapidly evolving market.

Biometric authentication becoming standard

Biometric authentication is on track to become the default method for securing payments in 2025. Valued at over $3.5 billion in 2020, it is forecast to reach nearly $8.8 billion by 2026. With advancements in technology and growing consumer familiarity, methods like fingerprint scanning, facial recognition, and voice authentication are becoming more reliable and widespread. These solutions are offering both heightened security and a seamless user experience, addressing two critical demands in today’s payments landscape.

For businesses, the adoption of biometrics presents significant opportunities to reduce fraud and improve customer satisfaction. By replacing passwords and PINs with biometric identifiers, payment providers can mitigate the risks associated with stolen credentials, enhancing trust in their platforms. Additionally, biometrics are enabling faster checkout processes, especially in environments where speed and convenience are crucial, such as retail and public transport.

However, the widespread adoption of biometrics also raises challenges. Payment firms must address concerns around data privacy and ensure robust systems to protect sensitive biometric data. Companies that can balance innovation with compliance and security will be well-positioned to lead as biometrics become the new standard in payment authentication.

The road ahead

As the payments industry prepares for 2025, the opportunities for innovation are immense, but so are the challenges. Trends like embedded finance, AI advancements, CBDC adoption, sustainability, and biometrics are set to redefine how businesses and consumers interact with payments.

However, firms must navigate regulatory uncertainties, rising cybersecurity threats, and the growing need for inclusivity. Success in 2025 will hinge on adaptability. Companies that embrace these trends, invest in cutting-edge technologies, and prioritise customer needs will remain competitive and help shape the future of payments.

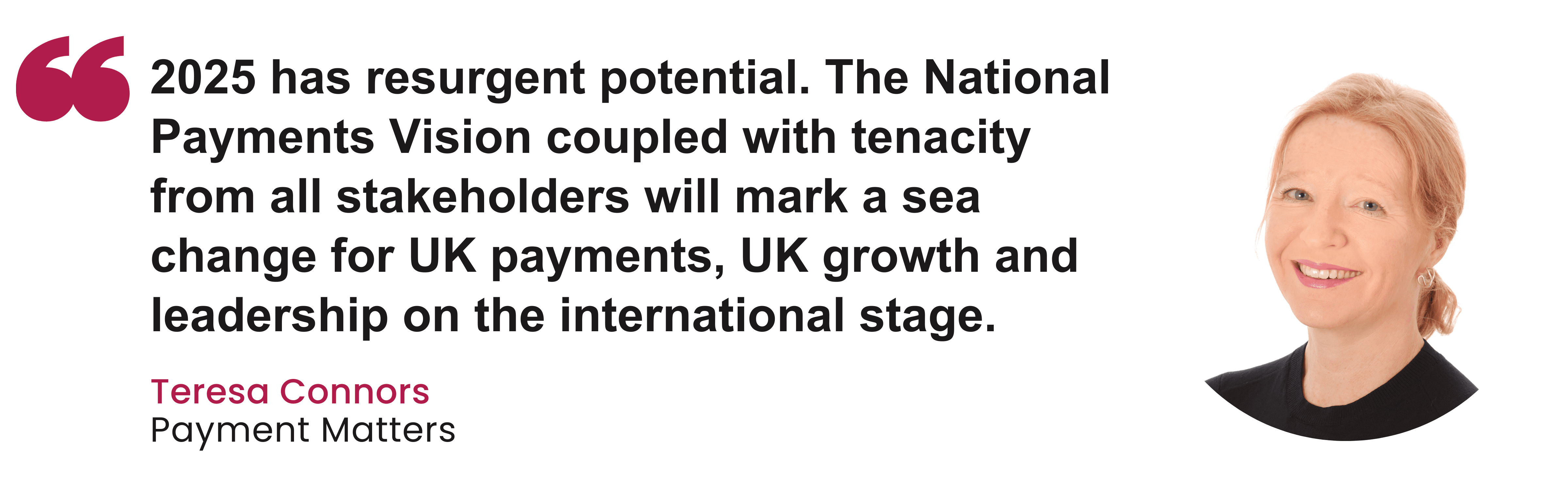

Cilliers added: I think that 2025 will be a year when we will see a lot more use cases for instant payments both in the UK and abroad. Recent regulation will also drive innovation in fraud management, which is an essential component for the success and consumer trust in this payment method.”

The road ahead is both dynamic and demanding, and those who act boldly today will lead the way tomorrow.