Private-sector banks have expressed concerns that CBDC threatens their businesses because it would undermine their role as intermediaries. However, this assumes that CBDC would compete with bank deposits; such an argument is preposterous. If CBDC were to be held outside accounts, it would not be rehypothecated, so it would not earn interest. Parties seeking a return would be better off depositing money with a financial institution. But the concern about disintermediation belies an existential question: why do households and businesses deposit money with banks, anyway? Is it really about putting their money to work, the classical motivation for banking, or is it actually about access to payment services? Are banks failing to deliver value to their customers that could not just as easily be delivered by telecommunications providers or other technology firms operating at the behest of central banks instead?

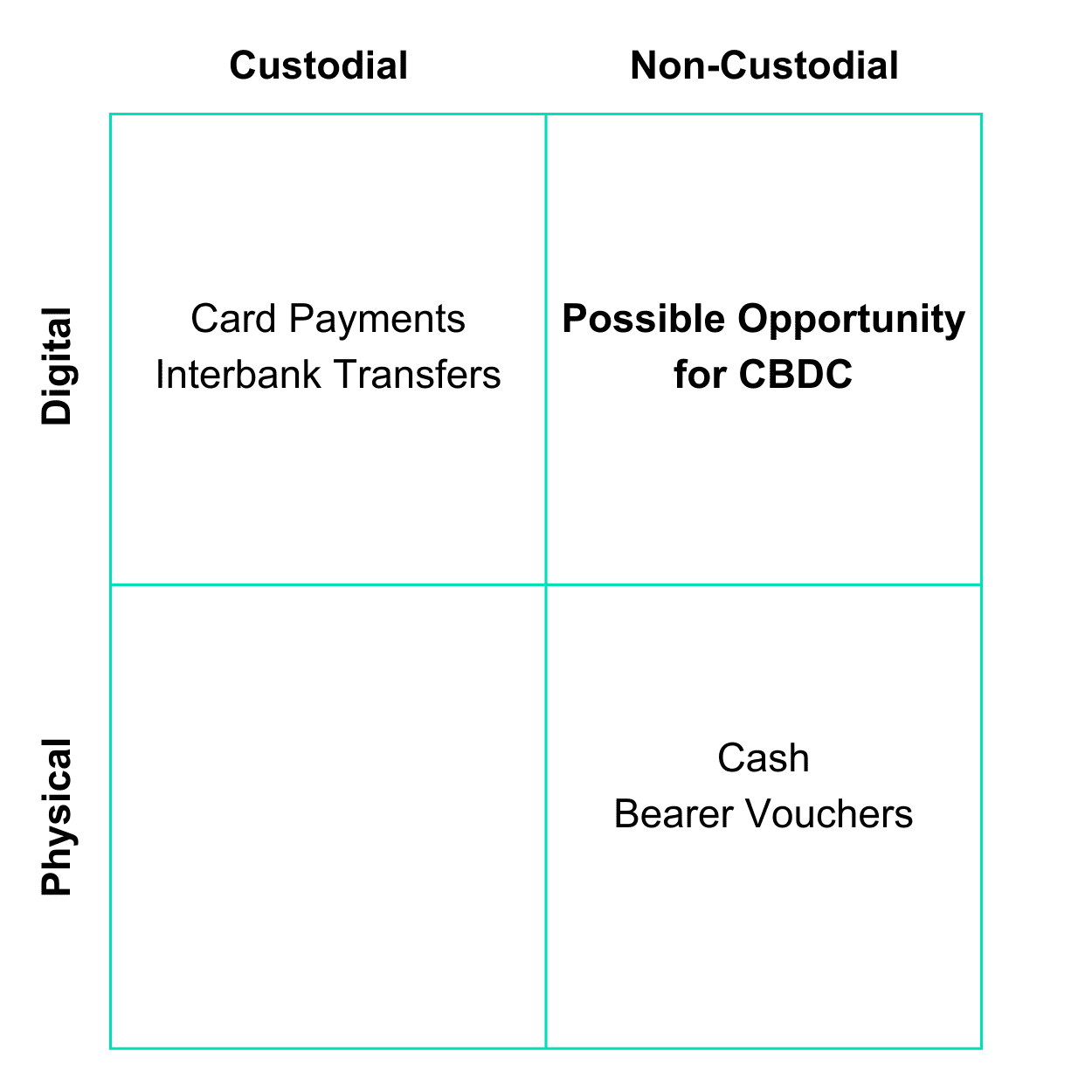

The foundational raison d’etre and precondition common to all digital currency is the idea that digital assets can be held directly, outside of custodial accounts. An account by any other name would lack the most salient feature of this new innovation. And indeed, many of the so-called “wallets” proposed by banks and technology firms are just that. If a payer must invoke his or her asset custodian in a transaction, then the custodian must have possession, control, or both. To the extent this is true, the value of digital currency is lost, and sceptical groups such as the UK House of Lords are right to ask whether CBDC really is a solution in search of a problem.

The foundational raison d’etre and precondition common to all digital currency is the idea that digital assets can be held directly, outside of custodial accounts. An account by any other name would lack the most salient feature of this new innovation. And indeed, many of the so-called “wallets” proposed by banks and technology firms are just that. If a payer must invoke his or her asset custodian in a transaction, then the custodian must have possession, control, or both. To the extent this is true, the value of digital currency is lost, and sceptical groups such as the UK House of Lords are right to ask whether CBDC really is a solution in search of a problem.

Financial crime 2026 pulse report

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Regulation Roadmap Q3

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Consumer behaviour 2026 report

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.