Regulation Roadmap Q3

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

January 13 2025

by Payments Intelligence

What is this article about?

The impact of the UK Digital Assets Bill on PSPs, highlighting legal uncertainties, operational challenges, and strategic opportunities.

Why is it important?

It addresses how evolving regulations shape the digital asset landscape, influencing innovation, compliance, and global competitiveness.

What’s next?

PSPs must adapt by enhancing compliance, leveraging new frameworks for innovation, and collaborating to shape practical regulatory solutions.

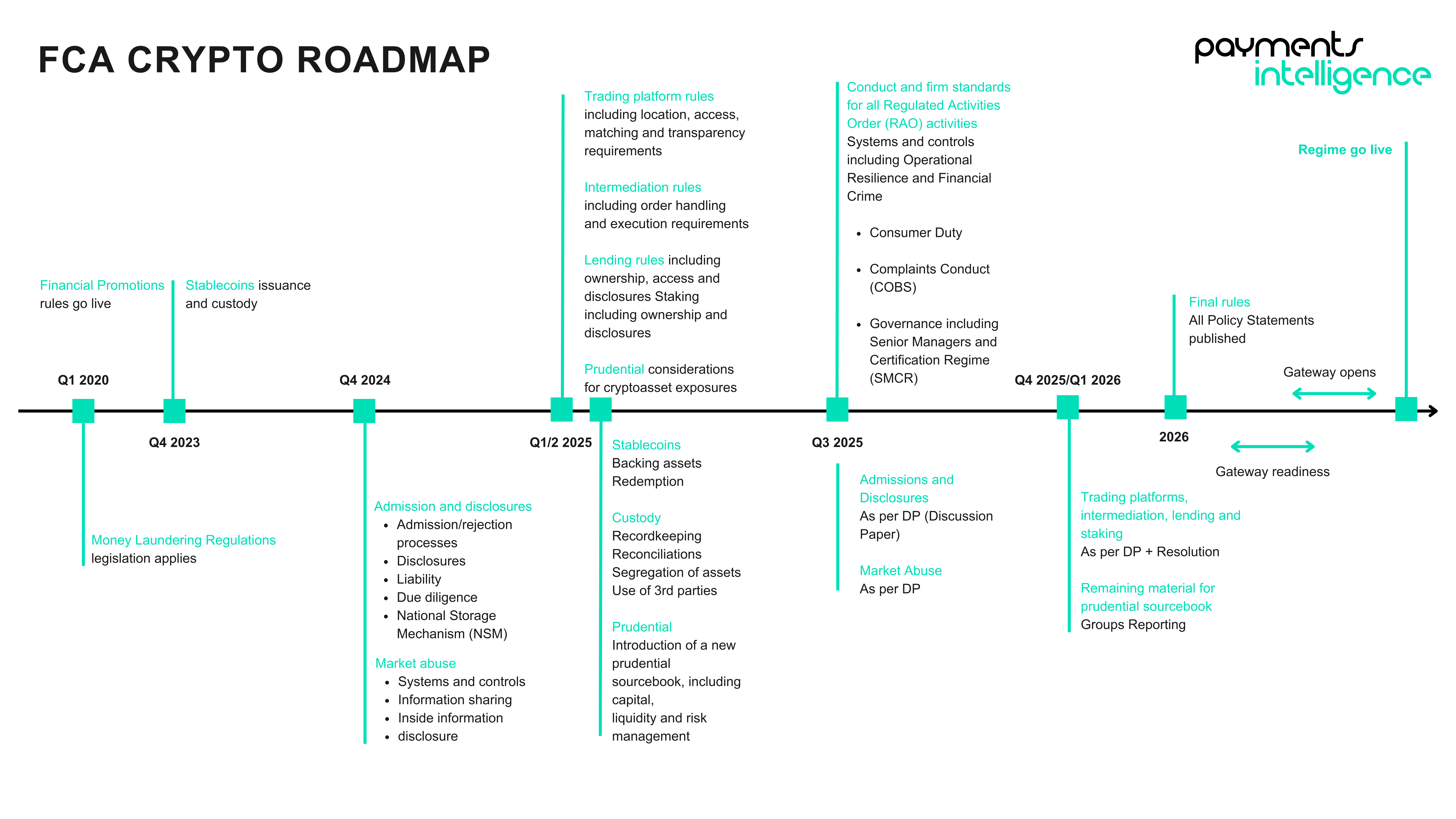

As is the nature of the regulation, the regulatory landscape for digital assets in the UK is proving to mark a pivotal moment for the payments sector. The introduction of the Digital Assets Bill and the Financial Conduct Authority (FCA)’s ongoing efforts to regulate cryptoassets demonstrates the regulator’s intentions to further define just how digital assets are governed and traded.

The Bill has sparked debate within the industry over its practical relevance for industry players, with many viewing it more of an academic exercise as opposed to a transformative shift. On the contrary, the FCA’s recent discussion papers, including those on admissions, disclosures and market abuse regimes, signal a more immediate impact on firms operating within the space.

Recently, The Payments Association (TPA) released its response to the Bill, in which it highlighted several key challenges that could hinder its ability to deliver practical benefits to the payments industry. The majority of these challenges primarily stem from the Bill’s approach to the legal uncertainty that shrouds the space as well as the broader implications for the UK’s position in the global regulatory landscape.

One of the primary concerns raised by TPA is the introduction of a third category of personal property for digital assets. While intended to clarify ownership rights, this approach risks prolonging uncertainty as courts struggle with defining and applying new legal principles.

The concern is regarding the period of adjustment and whether this leaves firms exposed to operational and compliance risks, particularly in the absence of established precedents. For PSPs, this uncertainty complicates contract negotiations and the enforcement of rights. This could slow innovation and hike costs.

According to the TPA response, the Bill’s approach could set the UK apart from other major common law jurisdictions, including Singapore and Australia. Both countries have opted to integrate digital assets into existing property law frameworks instead of creating separate categories.

Industry insiders are concerned that divergence from these jurisdictions could damage the UK’s reputation as a global hub for its digital asset businesses. These businesses often favour jurisdictions with more aligned and predictable legal standards, which could significantly impact PSPSPs’ cross-borderspirations or operations.

An unintended consequence of establishing a new legal category may inadvertently weaken the UK’s position in space. Firms may choose to opt for jurisdictions with simpler, harmonised approaches, deterring investment and innovation in the UK’s payments ecosystem; this would, in turn, undermine the government’s broader goal of fostering international competitiveness.

The practical implications of this should present several considerations for PSPs. Most of these centre on how firms handle digital assets, particularly stablecoins, as well as the operational and legal adjustment needed to navigate the changing landscape.

Stablecoins, as a subset of digital assets, have been a focal point of both the Bill and the FCA’s regulatory discussions. While the Bill aims to provide clarity by recognising digital assets as a distinct form of personal property, which could enhance legal certainty in ownership and enforceability of stablecoins, PSPs should be aware of several implications:

Under the Bill’s framework, stablecoins may now be explicitly classified as personal property. As this recognises their status in English law, it also introduces new responsibilities for PSPs acting as custodians. It is advised that firms ensure their custody arrangements, contracts and terms of service are aligned with these legal definitions in the interest of avoiding disputes while strengthening consumer trust.

On Redemption Rights, stablecoins often promise redemption at a fixed value, for example, 1:1 with fiat currency. Under the Bill, PSPs will be required to review their obligations under this evolving legal framework to confirm their ability to deliver on redemption guarantees. This will require operational safeguards and possibly stricter liquidity management to meet new compliance benchmarks.

Similarly, regarding cross-border operations, the bill’s divergence from other common law jurisdictions may complicate matters from the enforcement of stablecoin-related contracts perspective. A requirement of firms will be to adapt legal documentation and policies to manage differing jurisdictional requirements, adding further complexity to operations.

Important legal risks are introduced by the introduction of a third category of personal property. Most notably, the three areas are contractual uncertainty, asset recovery challenges, and consumer claims. In the context of the former, as courts establish precedents for digital assets as a third property category, PSPs may encounter ambiguity in how contracts involving stablecoins and other digital assets are interpreted. This could lead to disputes over ownership, custody, and liability in cases where the legal framework is yet to be fully tested.

The Bill’s new framework aims to enhance the ability of courts to trace and recover misappropriated digital assets. However, PSPs must ensure their systems and processes support this capability, which may involve implementing blockchain analytics tools and strengthening compliance with anti-money laundering (AML) and counter-terrorist financing (CTF) regulations. With stablecoins now clearly recognised as property, consumers may have greater legal recourse in disputes with PSPs. Firms must proactively review their terms of service and dispute resolution mechanisms to mitigate potential liabilities.

To address the implications of the Bill and the regulator’s crypto-regulatory roadmap, PSPs will need to make significant operational adjustments, including enhanced due diligence—the proposals for admissions and disclosures (A&D) and market abuse regimes (MARC).

The FCA’s proposals for admissions and disclosure (A&D) and market abuse (MARC) will require PSPs to ensure they’re conducting robust due diligence on both issuers and cryptoassets they support. This will also include verifying the legitimacy of assets, auditing their technical infrastructure, and assessing market risks simultaneously.

PSPs will also be required to align their compliance programmes with the FCA’s new standards for disclosures, transparency, and consumer protection. Providing accurate disclosures about stablecoin mechanisms, such as backing assets or redemption policies, will become a critical requirement under the Bill.

Given the likely scenario of the operational burden of implementing these systems capable of supporting new legal and regulatory demands increasing, PSPs are recommended to invest in blockchain analytics tools, automated compliance monitoring systems, and enhanced reporting capabilities.

The evolving legal definitions and compliance obligations will require PSP teams—particularly those in legal, compliance, and customer service roles – to be given targeted training to help them navigate the new complexities.

While the evolving regulatory landscape for digital assets poses significant challenges, it also opens up several strategic opportunities for PSPs to differentiate themselves, enhance their offerings, and secure a competitive edge in a growing market.

For example, introducing legal clarity and stricter oversight will benefit PSPs, who can position themselves as reliable and compliant custodians of digital assets. By actively engaging with the new frameworks, firms have the opportunity to instil greater confidence in consumers by addressing the longstanding concerns about some of the longer-term risks associated with digital asset transactions.

As legal clarity around digital assets improves, PSPs are uniquely placed to innovate and diversify their services, leveraging the new frameworks to offer tailored solutions to both consumers and businesses.

The regulatory advancements could possibly pave the way for firms to expand their reach into previously untapped markets, both geographically and demographically.

While the space is quickly evolving, cooperation between regulators, businesses, and industry bodies will be pivotal. Firms that position themselves as leaders in fostering collaboration and driving standards will emerge as leaders. This can be done by:

To adapt to the shifting goalposts surrounding the digital asset space, PSPs must adopt a proactive and strategic approach to navigate challenges and seize future opportunities.

In summary, firms should prioritise several key actions to prepare and build resilience in the sector. Firstly, they must invest in understanding and integrating the regulatory requirements into their operations. Conducting comprehensive due diligence on digital assets and implementing robust compliance frameworks will be critical to ensuring adherence to both the proposed admissions and disclosures regime and market abuse regulations. Establishing systems to support transparency—such as enhanced reporting tools and blockchain analytics—will not only meet regulatory expectations but also foster trust among consumers and partners.

Secondly, firms should actively engage with industry bodies and regulatory consultations. By contributing to the ongoing dialogue, firms can help shape practical and innovation-friendly frameworks while gaining early insights into regulatory shifts. Collaborative efforts, whether through trade associations or partnerships with other market players, can streamline compliance efforts and drive collective solutions to shared challenges.

Finally, PSPs must leverage the opportunities presented by these regulatory changes. Embracing legal clarity around stablecoins and digital assets allows firms to develop innovative offerings, such as secure custody solutions, faster cross-border payment systems, and tailored financial products. By positioning themselves as leaders in compliance and innovation, PSPs can differentiate their services, attract new clients, and strengthen their competitive edge.

Ultimately, the evolving regulatory environment is pivotal for PSPs to demonstrate their commitment to consumer protection, market integrity, and operational excellence. By taking decisive action now, PSPs can not only mitigate the uncertainties of this transition but also emerge as trusted and forward-thinking players in the future of digital finance.

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.

New research shows vulnerable customers are strong adopters of AI and digital banking, but are far more likely to experience failed payment journeys and poorer outcomes.

You need to be logged in to do this!