What is this article about?

The challenges and priorities facing merchants in the evolving payments landscape over the next 12 months.

Why is it important?

It highlights key trends, such as open banking, tokenisation, and fraud prevention, which are crucial for merchants to remain competitive and secure.

What’s next?

Merchants need to continue adapting to new payment methods, collaborate with industry peers, and stay agile in balancing innovation and regulatory compliance.

As the payments ecosystem continues to evolve with innovations like open banking, instant payments, and tokenisation, merchants are facing a host of challenges and opportunities. On September 19, Payments Intelligence hosted an insightful payments labs roundtable session with key players in the merchant space to discuss their strategies and priorities for the year ahead.

The discussion covered a wide range of topics, from the increasing diversification of payment methods to fraud prevention and regulatory concerns. The participants also examined the role of collaboration in overcoming shared challenges, all while adapting to changing consumer expectations.

Participants

Emerging trends in merchant payments: The next 12 months

The roundtable began with an exploration of emerging payment trends set to shape the industry. Sophie Chandler highlighted how the adoption of alternative payment methods is gaining momentum. “We’ve seen a shift from direct card payments to wallets like Apple Pay and PayPal, especially in markets like Germany and the UK,” Chandler explained. She noted that Holiday Extras had recently introduced Apple Pay and is working on a PayPal integration to accommodate customer preferences for frictionless, secure payment options.

Paul Fletcher from The Co-operative Group added that customer preferences for quick and easy payments are driving innovation in the e-commerce and grocery space. “We’ve recently implemented click to pay, a solution that allows one-click payments using network tokenisation, ensuring security while enhancing the customer experience,” he explained. This move reflects the growing need for merchants to offer a variety of payment methods, especially in high-frequency transaction environments like grocery retail.

Olga Gunchenkova echoed these trends, noting that open banking and instant payments are gaining traction across Europe, particularly in markets like the UK, Germany, and Sweden. “Open banking allows us to streamline deposits and withdrawals, making the customer journey faster and more seamless,” she said. With over 10% of withdrawals at Flutter International now occurring through open banking, the shift from traditional card payments is “undeniable”.

The impact of new payment methods on fraud prevention

Fraud prevention was a key concern raised by all participants. Fletcher pointed out that although fraud isn’t as prominent in the Co-op’s grocery and funeral care services, the integration of new payment technologies, such as tokenisation, is crucial to maintaining security. “Click to pay uses network tokens, which ensures customer card details are not exposed during transactions. This significantly reduces the risk of fraud,” Fletcher stated. These network tokens replace sensitive card information with a secure, randomly generated identifier, making it nearly impossible for fraudsters to gain access to the original card details, thus enhancing the overall security of each transaction.

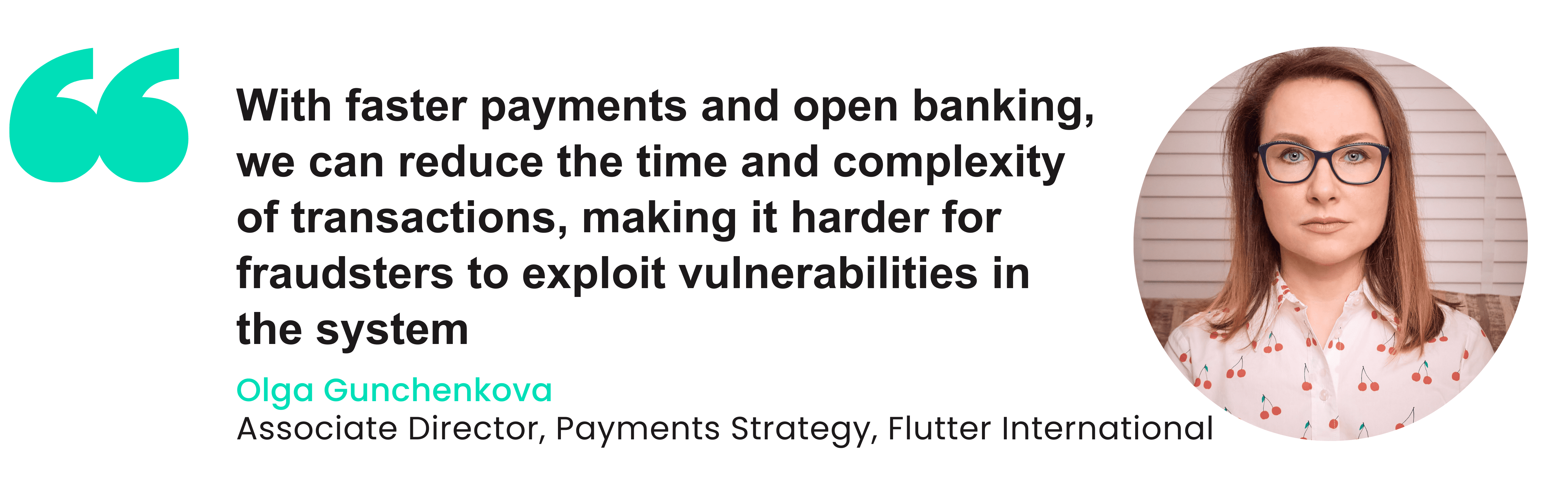

Gunchenkova added that instant payments through open banking are also helping to reduce fraud, particularly in high-volume industries like gaming. “With faster payments and open banking, we can reduce the time and complexity of transactions, making it harder for fraudsters to exploit vulnerabilities in the system,” she explained. However, despite the advantages of instant payments, merchants still face challenges around securing these transactions, especially with the increasing sophistication of fraudsters who are quick to adapt to new technologies. The need for continual updates to fraud detection algorithms and stronger customer authentication methods remains critical.

Moreover, Chandler discussed the role of AI in combatting payment fraud. “AI allows us to analyse real-time data and detect anomalies that human oversight might miss. It’s become an essential tool for spotting patterns that could indicate fraudulent activity,” she noted. By automating this process and making it more efficient, AI-driven fraud prevention systems help reduce both false positives and the overall risk of fraud, allowing merchants to provide a safer and more seamless customer experience.

Regulatory challenges and the future of digital payments

As payment methods evolve, so do the regulations governing them. Fletcher noted that the opacity of scheme fees remains a major challenge for merchants. “There are over 300 different card scheme fees, and it’s often difficult to understand what we’re being charged for,” he said. Gunchenkova agreed, emphasising that lack of transparency in fee structures creates difficulties for merchants trying to optimise costs. The need for clearer breakdowns of these fees was a recurring theme, with all participants highlighting how complicated it is for merchants to make informed decisions about their payment strategies when the cost structures remain so unclear. The rising costs, particularly for non-tokenised transactions, add an additional layer of complexity for businesses trying to balance security with affordability.

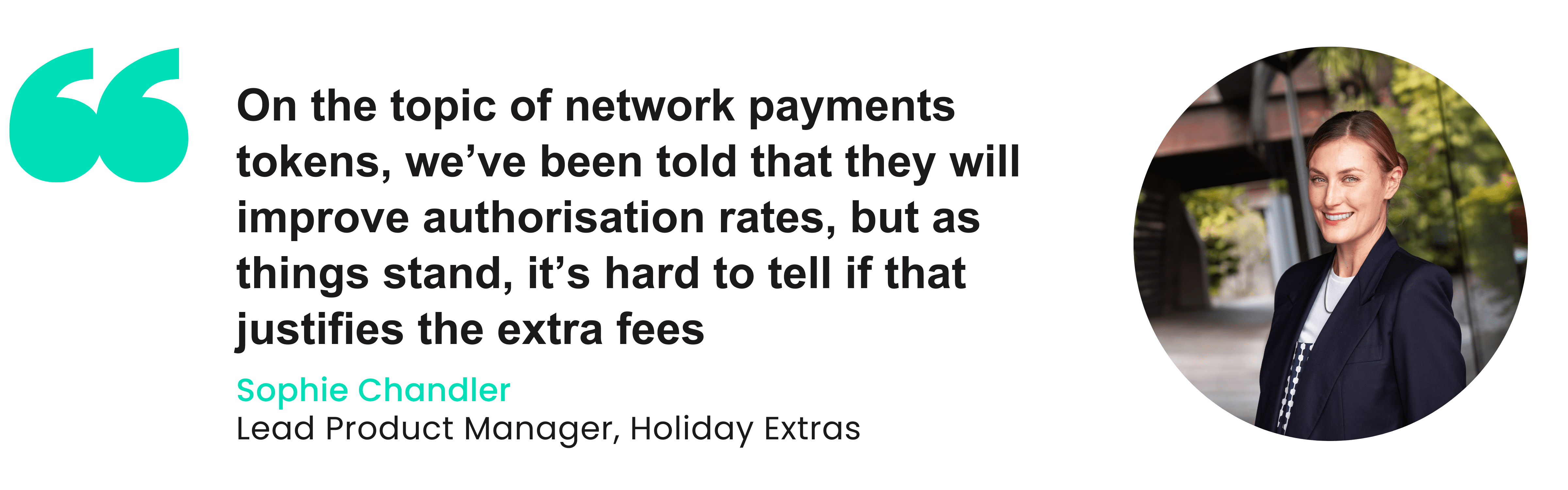

Chandler raised concerns about the additional fees associated with the introduction of network payment tokens, questioning whether the promised benefits, such as improved authorisation rates and enhanced security, justify the added cost. “We’ve been told that network tokens will improve authorisation rates, but it’s hard to tell if that justifies the extra fees,” she remarked. Both Chandler and Fletcher voiced apprehensions about whether merchants will truly see a return on their investment as these tokens become more widespread. The potential for mandatory adoption of these systems adds to the uncertainty, especially as many merchants are still grappling with the costs of compliance with existing regulatory requirements like PSD2 and SCA (strong customer authentication).

The conversation also turned to the future of digital currencies, particularly the Bank of England’s proposed digital pound. Fletcher saw the digital pound as an inevitability that merchants will need to adapt to but raised questions about the practicalities of integrating it into existing systems, especially for large organisations that rely on batch processing. While the potential for instant payments and reduced reliance on traditional payment rails is promising, it also poses significant challenges, especially for treasury departments that are not equipped to handle real-time flows. Chandler was more optimistic but noted that widespread adoption would require extensive consumer education and infrastructure upgrades to ensure both customers and businesses are prepared for such a shift. All participants agreed that while a digital currency could bring significant benefits, the road to implementation would be long and complex, requiring coordination between regulators, merchants, and technology providers.

Promising technologies for merchant innovation

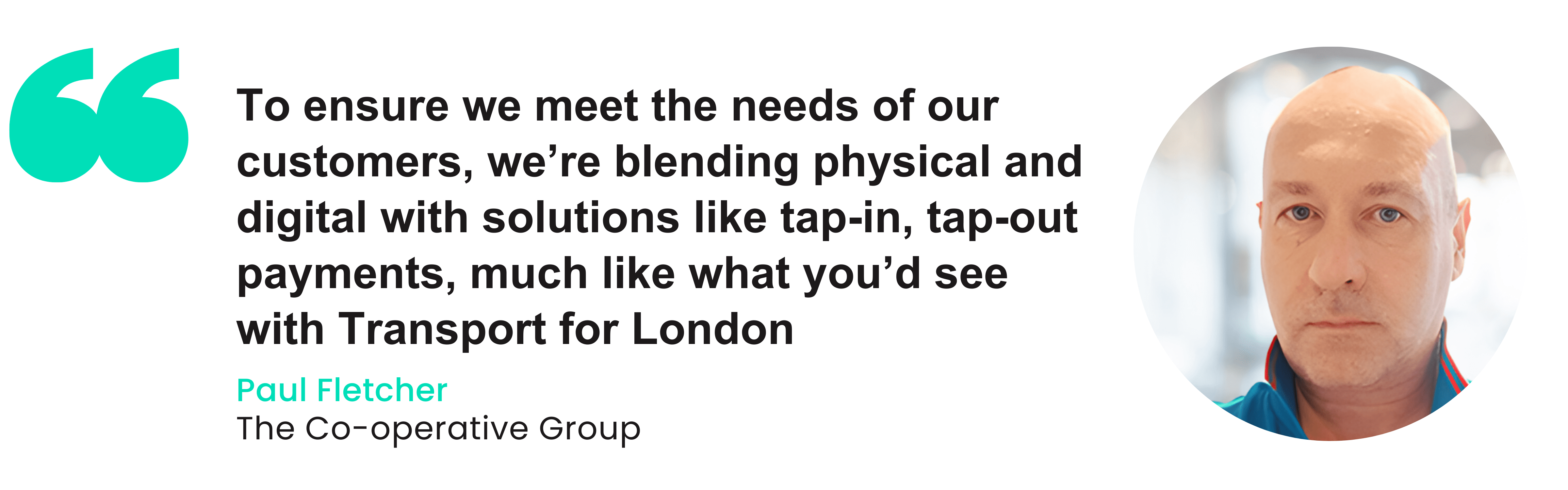

As the conversation shifted to innovation, Fletcher highlighted the potential of frictionless payments in the retail space. The Co-op is experimenting with cashier-less stores, where AI and machine learning enhance the shopping experience by allowing customers to make payments without queuing at tills. “We’re blending physical and digital with solutions like tap-in, tap-out payments, much like what you’d see with Transport for London,” he said. This approach leverages the convenience of contactless payment systems while ensuring customers have a seamless and efficient shopping experience, which is particularly relevant in convenience-driven sectors like grocery retail. Fletcher also mentioned the role of AI in optimising inventory management, linking real-time payments with stock levels to create a more responsive and data-driven retail environment.

Chandler discussed the importance of payment orchestration, which allows merchants to integrate multiple payment providers, ensuring they can offer the best options to customers. “We’re currently exploring new orchestration platforms to ensure we’re flexible enough to meet customer demands,” she explained. Payment orchestration simplifies the payment process for merchants by routing transactions through the most efficient or cost-effective channels. This not only reduces downtime and improves transaction success rates but also enables merchants to switch between payment gateways and methods seamlessly, offering customers a wide variety of options without needing to overhaul existing infrastructure.

Gunchenkova pointed out that while innovations like open banking and payment orchestration are promising, it’s crucial for merchants to partner with technology providers that deliver on their promises. “Some providers claim to offer full payment orchestration, but many are just traditional PSPs rebranding themselves,” she cautioned. She stressed the importance of due diligence when selecting providers, ensuring that merchants are adopting solutions that are genuinely innovative and tailored to their specific needs rather than merely following industry buzzwords. Gunchenkova also highlighted the rise of real-time analytics tools that allow merchants to monitor transactions and customer behaviour in real-time, providing insights that can be used to improve everything from fraud prevention to customer experience.

Furthermore, all participants acknowledged the growing role of biometric authentication in enhancing payment security and user experience. “Biometric technologies, such as fingerprint and facial recognition, are becoming increasingly popular in mobile payments,” Fletcher noted. These advancements offer a higher level of security compared to traditional passwords and PINs while also making payments quicker and more seamless for consumers. Merchants who adopt these technologies can offer a frictionless experience that meets both the security demands of regulators and the convenience expectations of customers. However, Chandler added that the cost of implementing these technologies, as well as consumer privacy concerns, need to be carefully managed to ensure widespread acceptance and trust.

Collaboration as a key to addressing merchant challenges

One recurring theme throughout the discussion was the need for collaboration. Chandler noted the importance of sharing insights between merchants to better understand emerging technologies like network tokens and payment orchestration. “We’re not competitors here, so these discussions allow us to learn from each other’s experiences, especially when it comes to navigating complex fee structures and security concerns,” she said. By openly exchanging information, merchants can avoid common pitfalls, optimise payment strategies, and ensure they are prepared for regulatory changes.

Gunchenkova agreed, adding that collaboration can help merchants make more informed decisions about suppliers and technology solutions. “Getting real-world feedback from fellow merchants is invaluable when assessing new technologies,” she said. Payment innovations like orchestration and tokenisation may look promising during presentations but can fall short during implementation. Through shared experiences, merchants can identify which solutions are genuinely effective and avoid costly mistakes, particularly when it comes to integrating complex systems or navigating fees.

Fletcher emphasised the role of industry organisations like The Payments Association and the British Retail Consortium (BRC) in fostering collaboration and advocating for merchant interests. “These organisations help drive conversations on important issues like fee transparency and regulatory changes,” he said. By working through these associations, merchants can present a unified voice, influencing policies that benefit the broader industry while also gaining insights into how others in the sector are overcoming shared challenges.

Conclusion

The roundtable discussion underscored the fact that while the payments landscape is evolving rapidly, merchants must remain agile in adopting new payment methods and technologies. With the rise of open banking, tokenisation, and alternative payment methods, merchants are being challenged to meet growing customer expectations for seamless and secure transactions. The participants agreed that keeping pace with these innovations is crucial for maintaining a competitive edge, especially as consumers demand faster, more personalised payment options.

Simultaneously, the complexity of navigating scheme fees, regulatory compliance, and fraud prevention remains a significant challenge. The need for transparency around fees and better support from payment providers was a key issue raised by the merchants, who are increasingly seeking ways to optimise costs while maintaining security. Balancing innovation with compliance, particularly as new regulations and payment methods like the digital pound emerge, will require ongoing collaboration between merchants, regulators, and technology providers.

Ultimately, fostering collaboration—whether through industry organisations, peer networks, or partnerships with fintechs—was seen as essential to overcoming these challenges. By sharing knowledge and leveraging collective expertise, merchants can better navigate the rapidly changing payments landscape and take advantage of emerging opportunities. As the next 12 months unfold, staying informed, adaptable, and united will be critical for merchants aiming to thrive in the future of payments.

Read more Payments Intelligence

Financial crime 2026 pulse report

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Regulation Roadmap Q3

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Consumer behaviour 2026 report

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.