Diana Carrasco Vime, head of the Digital Pound Project at the Bank of England, discusses the vision behind the digital pound and its potential to transform retail payments while maintaining trust and financial stability.

Why is the Bank of England exploring a digital pound, and what existing problems in the payments landscape are you aiming to solve?

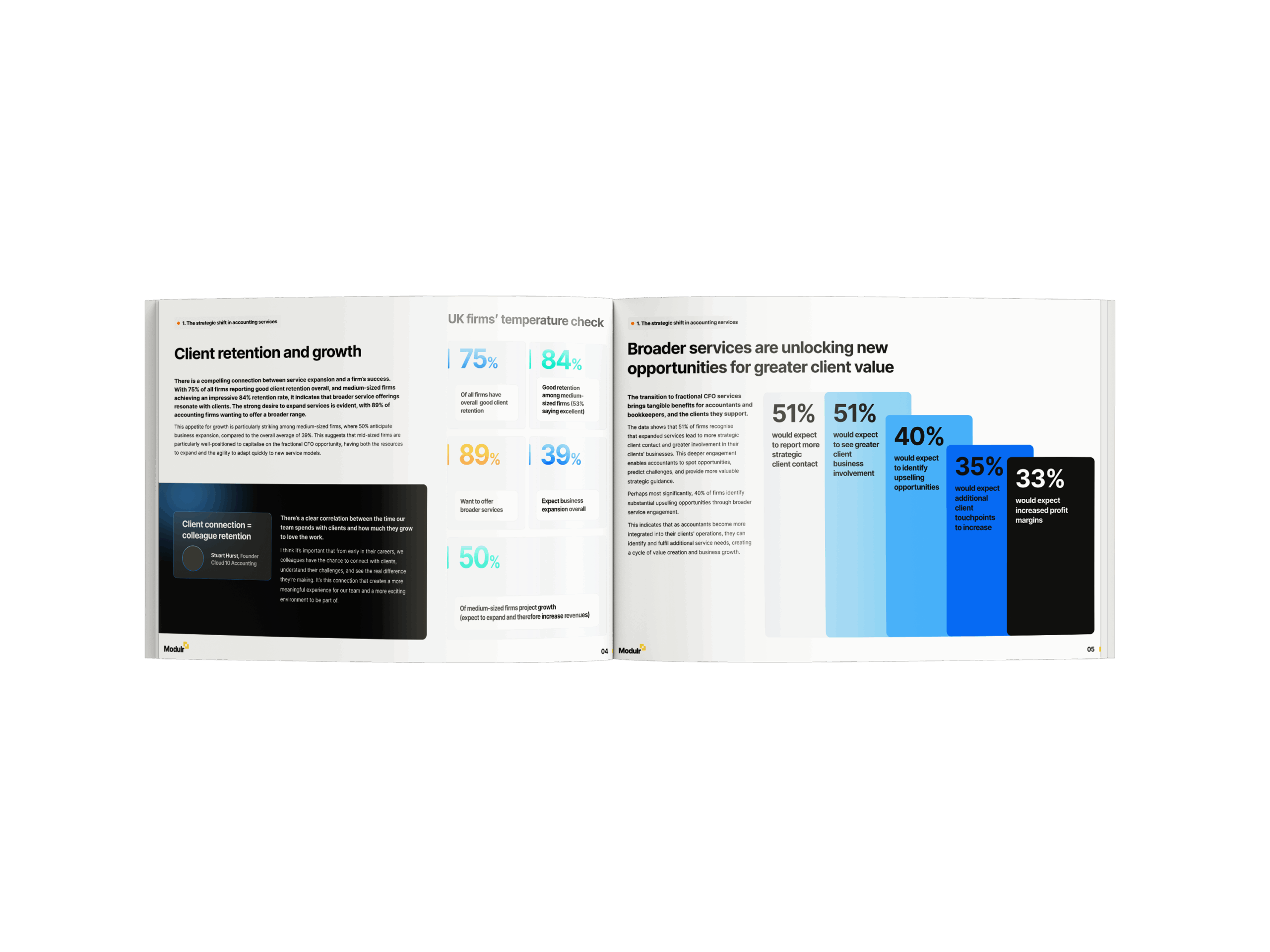

Diana Carrasco Vime: Exploring a digital pound is a strategic step to ensure the UK’s retail payments remain stable, innovative, and fit for an increasingly digital economy. How people pay for things is changing—cash usage is declining, and digital transactions are becoming the norm in many sectors. Innovation in retail payments depends on foundational infrastructure that enables payment service providers to develop new solutions. Commercial banks have the potential to drive this innovation, but if they don’t deliver, central banks may find themselves as the only game in town. By exploring a digital pound, the Bank aims to ensure public money remains a trusted, accessible foundation in the digital economy.

We are in the design phase, working closely with a range of stakeholders to determine whether a digital pound might add value, protect financial stability, and support innovation. No decision has been made. And we have been clear that any introduction would require public consultation and parliamentary approval. Ultimately, exploring a digital pound is about preparing for the future— ensuring the UK’s retail payments system continues serving people and businesses as payments evolve. If introduced, it would sit alongside existing money and payment methods, complementing rather than replacing them.

How could a digital pound change how consumers and businesses transact? What new opportunities might it unlock?

DCV: A digital pound may support innovation in retail payments by enabling payment providers to develop new offerings that improve convenience, efficiency, and accessibility. It would be part of our broader push to support retail payments innovation, ensuring the UK’s infrastructure remains fit for the future. A digital pound could help unlock faster, more affordable, and widely accessible services that complement existing options for consumers and businesses. We are also launching the digital pound lab to test real-world use cases, ensuring the private sector plays a central role in shaping how a digital pound might work in practice.

The Bank has emphasised working with the private sector. What role do fintechs and payments firms play in this ecosystem?

DCV: A digital pound would be a public-private platform for innovation, where the Bank provides the foundation while industry participants develop new services for consumers and merchants. The Bank is not focused on consumer-facing applications; private sector firms would create wallets, payment solutions, and commercialised business models that bring a digital pound to life. Collaboration is essential. For example, the digital pound lab, launching later this year, will enable hands-on experimentation, helping fintechs and businesses explore how a digital pound might integrate into their services. This approach ensures a competitive and innovative ecosystem that works seamlessly alongside existing payment solutions.

How do you see a digital pound coexisting with commercial bank money, stablecoins, and other payment methods?

DCV: A digital pound, if introduced, would sit alongside commercial bank money, properly regulated payment stablecoins, and other digital payment options. This could give consumers and businesses more choices and flexibility— complementing existing payment options while supporting continued stability and singleness of money. Interoperability is central to our design work, and we are conducting research and experimentation to ensure a digital pound, if introduced, would integrate seamlessly with existing financial infrastructure. This approach supports a thriving payments ecosystem where different forms of money work together.

What are the key considerations for ensuring widespread trust and adoption of a digital pound?

DCV: Trust is essential for any form of money, and a digital pound would only be introduced if it met the highest standards for privacy, security, and usability. Privacy would be guaranteed—the Bank and government would never have control over how people spend their money and privacy protections would be built in from day one. A digital pound must meet the highest security and fraud prevention standards, ensuring safe and reliable transactions while being easy to use and integrating seamlessly with existing payment systems for consumers and businesses.

What potential innovations could a digital pound enable that aren’t currently possible with existing payment methods?

DCV: A digital pound would provide a platform for payment innovation through entirely new propositions or by improving how existing payment services operate. We actively engage with the private sector to understand how a digital pound might support existing and emerging payment needs for consumers and merchants. The most exciting opportunities may be the ones we haven’t thought of yet—that’s why we’re inviting the industry to test ideas and help shape the future of retail payments as part of the digital pound lab, launching later this year.

How could a digital pound help improve financial inclusion and accessibility in the UK?

DCV: A digital pound may provide an easy-to-use, widely accepted way to pay—helping those without UK bank accounts or those who find digital payments challenging today. It could support payment service providers in offering more convenient, flexible digital payment solutions, ensuring more people can transact easily. Encouraging the development of new payment features, such as enhanced money management tools, could improve how people interact with digital payments. We are collaborating with payment firms, banks, fintechs, and consumer groups to explore how a digital pound might complement existing payment options and provide more choices for consumers and businesses.

How does the UK’s approach to digital currency compare with other jurisdictions, and what lessons can be learned from international efforts?

DCV: The global landscape for digital currencies is evolving, with central banks taking different approaches based on their domestic priorities. While some countries have paused their work, others continue to explore potential benefits. The UK remains committed to gathering evidence before making any decisions, ensuring that any digital pound, if introduced, would be based on clear policy and real-world needs. We are working closely with international partners to learn from their experiences and contribute to discussions on best practices, ensuring alignment with global financial stability and innovation goals.

What could the future payments ecosystem look like if a digital pound were introduced?

DCV: The future of payments will be increasingly digital, and the Bank’s priority is to ensure that money remains trusted, stable, and accessible throughout this transition. A digital pound could provide a stable, widely accepted foundation for innovations, supporting continued trust in money while meeting the evolving needs of households and businesses. Our ongoing work is focused on preparing for the future of payments, ensuring a resilient and innovative financial system that supports choice, flexibility, and security in a rapidly changing digital landscape.

")