Designing a future-ready payment hub means building modular, interoperable systems that integrate AI, digital currencies, smart contracts and scalable infrastructure to support new payment models.

Imagine starting with a blank canvas: how would you design a next-generation payment hub capable of meeting the demands of the next quarter-century?

In today’s fast-changing market, where emerging trends and technologies stand to reshape how we move money, what principles should guide the design of a new payment hub?

Artificial Intelligence, Central Bank Digital Currencies (CBDCs), stablecoins, micropayments, smart contracts and programmable money. Today’s industry is rife with buzzwords. But what do they actually mean, and how should each influence the design of a next-generation payment hub? This article demystifies the jargon and unpacks the concepts to tease out the capabilities essential for a future-ready payments infrastructure.

Artificial Intelligence

There are several areas where AI and payments intersect. Firstly, AI is already beginning to influence payment initiation. OpenAI has introduced functionality enabling a chat to evolve into a shopping session, complete with checkout and payment (using card rails -currently powered by Stripe- or account-to-account, as is the case in the UPI-powered Indian pilot). Users increasingly turn to AI as their primary tool for search, information gathering and synthesis -and now shopping. Conversational interactions will gradually augment traditional GUI-based interactions. From there, conversational payments and agent-initiated transactions are just around the corner.

The other major area where AI is influencing payments lies in back-end systems and processes. AI is already improving fraud detection and compliance screening, identifying new patterns, reducing false positives and automating manual tasks. As AI capabilities mature, machines will increasingly replace human intervention in the back office. From customer callbacks to repairs and manual entry of payment details, the potential for automation -and ultimately cost saving- is huge.

A next-generation payment hub must be able to call out to future AI systems (for example, to enrich or automatically repair a payment) and should, at a minimum, provide a set of APIs that AIs can invoke to retrieve payment details and carry out formerly manual tasks such as approving or amending a payment. APIs for payment initiation are also essential, but the direct interactions with AI agents should be treated as part of the channel domain and therefore outside the scope of this discussion.

As IT projects and systems integration increasingly rely on AI capabilities, our next-gen payment hub should include specifications and documentation that are easily digestible by an AI responsible for coding an interface (e.g., between a core banking system and the payment hub) or for developing and executing test cases.

Central bank digital currency (CBDC)

The scale of the undertaking is immense. The ECB has estimated that its own budget for the digital euro would be well north of a billion euros, while a tier-one commercial bank has estimated -off the record- that the digital euro would consume about one year of its entire IT spend.

What is CBDC, and how does it differ from electronic fiat currency? In short, CBDC is central bank money (like cash), as opposed to commercial bank money (issued by commercial banks under fractional reserve banking). It is also worth noting that while CBDC and blockchain are often used in the same breath, CBDCs can be implemented using mechanisms other than blockchain or other distributed ledger technology (DLT). Indeed, DLT’s scalability, throughput speed and energy efficiency are questionable. (Note: CBDC’s ability to support programmable payments, potentially associated with smart contracts, is addressed later in this article.)

There are two aspects of CBDC to consider: the “bean counting” and the actual transacting. The accounting aspect -while no simple undertaking- falls outside the purview of our next-gen payment hub (in much the same way that account management and payment functionality are separated in traditional architectures). The payment hub’s role will be to communicate with whichever system within the bank manages CBDC accounting or wallet management. It must therefore be capable of flexibly addressing multiple accounting or wallet systems (as many banks will likely implement separate systems for fiat versus digital currency).

When it comes to managing payments in CBDC, the role of our future payment hub is broader and more complex than it initially appears. As a digital equivalent of cash, CBDCs are expected to support a wide range of use cases, including P2P, point-of-sale, e-commerce, account-to-account (A2A) and even offline transactions. In some respects, CBDC transactions resemble traditional A2A payments (for example, the Digital euro foresees a specific Digital Euro Account Number or DEAN, and the current draft rulebook explicitly includes standing orders as a feature). Conversely, other aspects of the digital euro rulebook are more akin to today’s card rails. Examples include the support for POS/e-commerce use cases (leveraging the Nexo ISO 20022-based card standard), pre-authorisations and even the issuance of physical cards.

We can therefore conclude that, from a payments perspective, CBDC is a hybrid of A2A and card models. Consequently, our future payment hub must incorporate both A2A-like and card-like functionality. Implementing separate siloes for these transaction types should be ruled out due to the well-known drawbacks intrinsic to siloed architectures. Within the Domain-Driven Design (DDD) paradigm, our next-gen payment hub should comprise granular Domain Services that can be orchestrated in different ways to support diverse use cases. Thus, aspects of CBDC payments common to A2A-like and card-like scenarios need only be built once (for example, checking the availability of funds is fundamentally the same for both A2A-like and card-like transactions). Such an approach, based on orchestratable Domain Services, enables the payment hub to meet the hybrid requirements of CBDC in the most efficient manner.

Stablecoins

Stablecoins resemble CBDCs in many respects, particularly from a value and exchangeability perspective. By definition one stablecoin equals one fiat unit which equals one CDBC unit, and all three should, in theory, be freely interchangeable. However, unlike CBDCs -which are the preserve of central banks- stablecoins can, depending on the applicable regulatory regime, be issued by commercial banks or even by non-financial actors (such as Amazon or Walmart).

There are two areas where stablecoins are tipped to change the payments landscape:

- (1) as a mechanism for interbank settlement

- (2) as a closed-loop mechanism for financial exchanges between non-bank actors (retail and corporate).

Let’s examine each in turn.

The first use case -interbank settlement- is supported by organisations like Circle, whose USDC has become one of the most widely used stablecoins. The primary value proposition is straightforward: an alternative to traditional clearing systems and correspondent banking, enabling instant, 24/7/365 payments at a competitive price point. More advanced functionality, such as programmable payments, is also on the horizon. (More on that later.) Tomorrow’s payment hub needs flexible smart-routing capabilities to determine which rails a payment should utilise -traditional clearing and correspondents versus stablecoin. The ability to easily select from a library of standard messaging formats and exchange protocols is also critical for quick connectivity to new networks, as is the capability to configure new exchange formats rapidly.

The second area in which stablecoins are set to transform payments is as an alternative to traditional payment methods, particularly in retail. By minting their own coins, large retailers like Amazon can avoid the costs associated with more traditional payment methods, such as cards, while profiting from deposits from customers funding their stablecoin wallets. However, banks’ role in such schemes is likely to be limited to supporting stablecoin wallet funding and defunding operations -so-called on/off ramp transactions- which can effectively be boiled down to outbound and inbound A2A payments.

Smart contracts & programmable money

While not entirely synonymous, programmable money usually (but not always) relies on smart contracts. Similarly, the concept of programmable money is often conflated with CBDCs and stablecoins. However, CBDCs or stablecoins can exist without programmability. This is why we have chosen to address smart contracts and programmable money separately, as a topic in their own right.

Smart contracts enable conditionality in payments. A typical use case is payment on delivery, where payment to the seller is made only upon delivery of the goods or services to the buyer. With obvious applications in e-commerce and cross-border trade, banks are ideally positioned to be at the heart of such models.

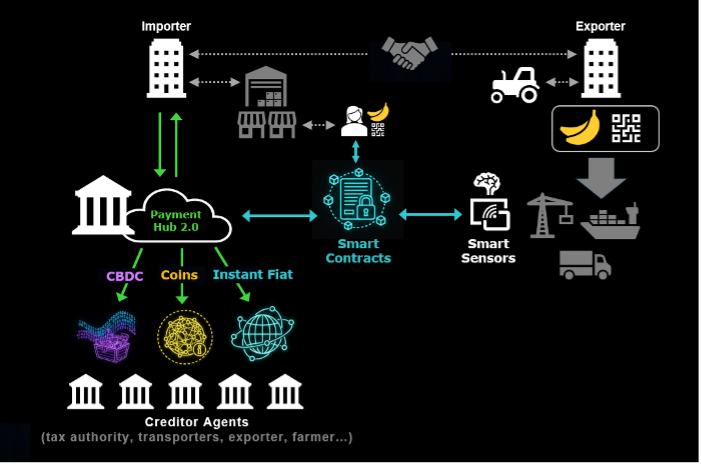

The payment hub of the future should be able to connect to smart contract infrastructure and hold or release payments based on the fulfilment of contract conditions. Consider the following example:

An importer of bananas enters into a trade agreement with an exporter. A smart contract is established to govern the movement of funds associated with this cross-border trade. In today’s trade finance world, a bank plays a key role as a trusted intermediary, providing a smart escrow service known as payment versus delivery (PVD). When the smart contract’s conditions are fulfilled (for example, receipt and inspection of cargo -potentially verified by smart sensors), the bank releases funds to the various parties involved. This includes the seller/exporter, the shipping agent, a local transporter, and the tax authority collecting import duties. The bank’s ability to orchestrate these payments and disburse them across different rails according to each party’s preferences cements its role as a central orchestrator.

In a world where fair trade has gained significant traction, one can imagine that each individual banana bears a QR code. When the end consumer scans the QR code, a smart contract is triggered, causing a micropayment to credit a small independent banana farmer. Such a micropayment could be an extension of the smart escrow service (thereby debiting the banana importer) or could function as a tip, paid by end consumers directly.

The ability to facilitate such use cases is crucial for the payment hub on our virtual drawing board. By leveraging their position of trust and embracing the relevant new technologies, banks can offer monetisable value-added services on top of commoditised payments. Our next-generation payment hub must include in its blueprint the ability to control payments lifecycles through interactions with external systems, such as smart contracting platforms. Because interfaces to smart contracts are unlikely to be standardised and because business use cases will be numerous, the payment hub needs sufficient flexibility to adapt to diverse scenarios.

Micropayments

Another emerging trend is micropayments: an increase in the number of payments accompanied by a decrease in their individual value. This shift is driven by both technological and societal factors. The rise of the Internet of Things (IoT) and pay-per-use models will challenge established models. Monthly all-inclusive subscriptions to services like Netflix or Spotify work well for many, but a pay-per-use model with associated micro payments may work better for the casual user (or those wishing to avoid subscription to multiple similar or overlapping services).

New entrants will emerge in a variety of industries seeking to capture market share by offering alternative payment models. Instead of traditional car financing or leasing, imagine a model where you pay by the kilometre. The price per kilometre might be higher than in a traditional model, but it will satisfy the requirements of certain users, such as those who wish to minimise periodic spending and/or drive relatively infrequently. History offers many examples of capital-rich actors effectively “advancing the money” and receiving delayed repayment for profit. We already mentioned car financing; other examples include fitness equipment (such as Peloton), home energy solutions like batteries, and consumer electronics.

As the number of payments is set to increase exponentially, so too must the performance of banks’ payment systems. The payment hub of tomorrow must be capable of handling colossal volumes of real-time, single-transaction throughput. The days of bulk processing large files are drawing to a close, as instant individual payments are replacing them across the economy. Systems able to scale to tens of thousands -and eventually several hundred thousand- transactions per second should be foreseen.

Interoperability

The boundaries between traditional payment silos are eroding and becoming increasingly porous. Domestic instant payments schemes are beginning to gain the ability to clear cross-border payments (consider Euro One-Leg-Out or BIS’ Nexus initiative). Traditional correspondent banking is therefore becoming interoperable with modern instant payment rails. Similarly, correspondent banking will need to adapt and become interoperable with stablecoin networks. The emergence of CBDCs adds yet another dimension to this interoperability, with banks required to provide facilities (on-ramp/off-ramp) for converting fiat to digital and vice versa.

Our next-generation payment hub needs to account for these new realities. A single monolithic “be-all/do-all” payment hub could theoretically provide an answer. However, this design falls short in several respects: such systems are notoriously difficult to maintain and ill-suited to phased implementation. Furthermore, they cannot be optimised for the specific non-functional requirements (NFRs) of different payment types and schemes. What’s needed is a modular solution in which components can be deployed, maintained and tuned separately while “bridges” between modules deliver the all-important cross-scheme interoperability.

Conclusion

Designing a next-generation payment hub is not merely an exercise in technology selection; it is a strategic response to a rapidly evolving financial ecosystem. From AI-driven automation to CBDCs, stablecoins, smart contracts, and micropayments, the forces reshaping payments are diverse yet interconnected. The common thread is flexibility: architectures must be modular and capable of orchestrating complex workflows across multiple rails and domains.

Ultimately, the payment hub of tomorrow is more than a system; it is an enabler of new business models and customer experiences. The architecture we choose today will shape whether banks remain the orchestrators of value or become mere participants in a broader ecosystem. As boundaries blur between incumbents and disruptors, who will lead the charge in setting the standards?