PAY360 2025 unpacked: Key survey findings shaping the future of payments

This report presents data-driven insights from a major industry survey, highlighting the key trends, risks, and priorities shaping payments in 2025.

January 3 2025

by Payments Intelligence

What’s the article about?

A roundtable discussion among merchants addressing the evolving challenges of fraud in their operations across various sectors.

Why is it important?

It highlights the necessity of advanced fraud detection and greater industry collaboration.

What next?

Improving regulations, using technology for detection, and fostering industry-wide cooperation.

On 19 November 2024, merchants from across sectors gathered in London as part of The Payments Association’s Financial Crime 360 (FC360) series to address the ever-evolving challenge of fraud in their operations. From payment fraud and chargebacks to cybercrime and emerging AI-driven threats, the roundtable provided a dynamic platform for merchants to share their experiences, strategies, and concerns. This session drew participants from diverse industries, including retail, travel, telecommunications and hospitality, each grappling with unique yet interconnected fraud challenges.

As fraud continues to grow in sophistication, merchants are increasingly at the forefront of the battle against financial crime. Fraudsters, armed with advanced technologies and professional networks, are exploiting gaps in systems and consumer behaviour. The discussion underscored the pressing need for end-to-end visibility, improved fraud detection technologies, and greater collaboration across sectors.

Participants:

The discussion began with a stark overview of fraud trends, highlighting how criminals are continually adapting their methods to exploit new vulnerabilities. Participants noted that while unauthorised fraud, which accounted for annual losses of £709 million, such as remote purchase, remote banking and lost and stolen cards, has remained relatively steady, authorised fraud—particularly investment, purchase, impersonation and romance scams—has surged in recent years to £460 million.

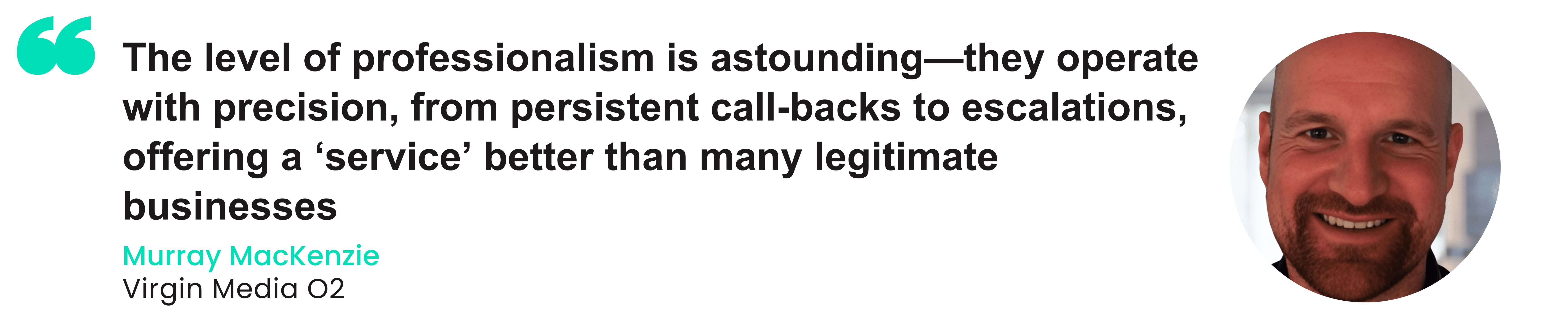

Mark McMurtrie (TPA) opened the session by presenting data showing how fraud tactics have shifted from physical card theft to more sophisticated digital scams. “Criminals are professionalising their operations, constantly evolving to exploit the weakest links in our systems,” he explained. This sentiment was echoed by Murray MacKenzie (Virgin Media O2), who described the rise of international scam call centres: “The level of professionalism is astounding—they operate with precision, from persistent call-backs to escalations, offering a ‘service’ better than many legitimate businesses.”

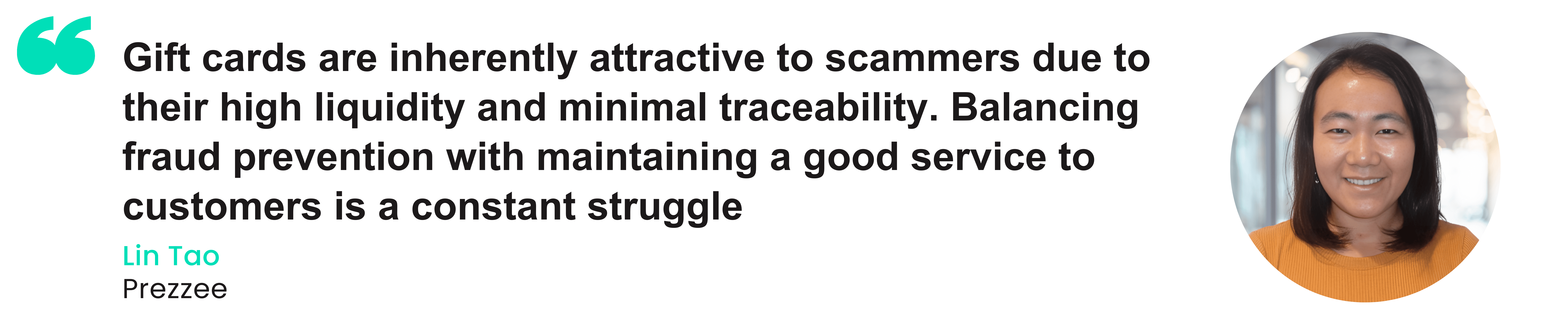

The unique challenges of certain sectors came to light during the conversation. Lin Tao (Prezzee) highlighted the disproportionate risk her industry faces: “Gift cards are inherently attractive to scammers due to their high liquidity and minimal traceability. Balancing fraud prevention with maintaining a good service to customers is a constant struggle.” Similarly, David Kershaw (TFL) described how fraudsters constantly look for vulnerabilities. “We are investing in new technologies to prevent fraud taking place on our network,” he said.

Chargebacks emerged as a shared pain point across sectors, with merchants expressing frustration at how the process works. Katherine Bailey (Valor Hospitality Europe Limited) explained how customers manipulate chargeback systems to claim refunds for services they’ve already consumed: “The guests enjoy a stay or experience and then dispute the charges. The card issuers often side with the customer without consulting us, which is unfair and costly.” Gitika (TFL) shared a similar concern about how customers can manipulate the process for double compensation: “Sometimes, customers raise a refund and then also initiate a chargeback, essentially getting compensated twice. This is a loophole that needs to be closed.”

The topic concluded with participants agreeing that fraud is no longer limited to traditional theft or hacking. Instead, it encompasses increasingly complex schemes that exploit systemic gaps, from first-party fraud to sophisticated AI-driven scams. As Tao summarised, “Fraudsters are becoming more creative, and so must we. The challenge is not just detecting fraud but anticipating its evolution.”

A recurring theme during the roundtable was the challenge of balancing robust fraud prevention with a seamless customer experience. As consumer expectations for frictionless payments grow, merchants face the dilemma of introducing security measures that can inadvertently disrupt the user journey, risking customer dissatisfaction or abandonment.

MacKenzie highlighted this tension: “Customers demand a zero-friction experience, especially in e-commerce and retail. But the same customers expect us to safeguard their transactions from fraud. Meeting both expectations is like walking a tightrope.” He shared how his organisation had implemented a daily fraud review forum, bringing together directors from every department to ensure fraud measures were aligned with customer needs.

The conversation delved into the concept of “appropriate friction.” Kershaw emphasised the importance of tailoring security measures to the specific risks of each transaction. “We can’t treat a low-value bus fare the same as a high-value travel pass,” he explained. “It’s about introducing friction only where it’s warranted, like adding verification for transactions above certain thresholds.” Several participants agreed that selective, dynamic friction could both deter fraud and preserve the customer journey.

However, Bailey noted that industry-specific challenges often complicate this approach. “Hotels require pre-authorisations, which can confuse or frustrate customers, especially if it ties up their funds unnecessarily. We try to educate guests, but there’s always pushback when standard procedure to protect our revenue is perceived as a hassle,” she said.

Tao pointed out the role of technology in achieving this balance. “Orchestration layers that unify fraud detection systems are key,” she explained. “With a single capability evaluating risk across the entire customer journey, we can apply friction precisely when needed, rather than bluntly across all interactions.” Others echoed the need for integrated systems, which reduce redundancies and ensure fraud prevention tools work in harmony without disrupting the customer experience.

Education also emerged as a critical area for improvement. Bailey stressed the importance of educating both customers and internal teams: “Customers need to understand why certain measures are in place, and staff must know how to explain these processes effectively. Otherwise, friction is seen as incompetence rather than protection.”

The group also discussed the potential of consortium data platforms to enhance fraud detection. Bailey noted that while such platforms exist, they are often limited by narrow definitions of fraud or sector-specific focuses. “For example, what’s considered fraud in hospitality might not align with what retailers or transport operators experience. To be truly effective, consortiums need to accommodate the diversity of fraud types,” she said.

Merchants gathered in London to tackle evolving fraud challenges, highlighting technology and collaboration as key to staying ahead.

This report presents data-driven insights from a major industry survey, highlighting the key trends, risks, and priorities shaping payments in 2025.

Your quarterly overview of the key regulatory changes impacting payments—what’s happening, what’s coming, and what actions to take

AI is reshaping the fight against payment fraud, prompting financial leaders to adapt with smarter tools, better data, and cross-sector collaboration.

The Payments Association

St Clement’s House

27 Clements Lane

London EC4N 7AE

© Copyright 2024 The Payments Association. All Rights Reserved. The Payments Association is the trading name of Emerging Payments Ventures Limited.

Emerging Ventures Limited t/a The Payments Association; Registered in England and Wales, Company Number 06672728; VAT no. 938829859; Registered office address St. Clement’s House, 27 Clements Lane, London, England, EC4N 7AE.

Log in to access complimentary passes or discounts and access exclusive content as part of your membership. An auto-login link will be sent directly to your email.

We use an auto-login link to ensure optimum security for your members hub. Simply enter your professional work e-mail address into the input area and you’ll receive a link to directly access your account.

Instead of using passwords, we e-mail you a link to log in to the site. This allows us to automatically verify you and apply member benefits based on your e-mail domain name.

Please click the button below which relates to the issue you’re having.

Sometimes our e-mails end up in spam. Make sure to check your spam folder for e-mails from The Payments Association

Most modern e-mail clients now separate e-mails into different tabs. For example, Outlook has an “Other” tab, and Gmail has tabs for different types of e-mails, such as promotional.

For security reasons the link will expire after 60 minutes. Try submitting the login form again and wait a few seconds for the e-mail to arrive.

The link will only work one time – once it’s been clicked, the link won’t log you in again. Instead, you’ll need to go back to the login screen and generate a new link.

Make sure you’re clicking the link on the most recent e-mail that’s been sent to you. We recommend deleting the e-mail once you’ve clicked the link.

Some security systems will automatically click on links in e-mails to check for phishing, malware, viruses and other malicious threats. If these have been clicked, it won’t work when you try to click on the link.

For security reasons, e-mail address changes can only be complete by your Member Engagement Manager. Please contact the team directly for further help.