The world of business payments is awash in deadlines, mandates and other milestones that will make this arguably one of the more impactful years in banking since the financial crisis of 2008. And most of that impact will be in the world of real-time payments and associated messaging protocols. It’s a tough calendar to track and prepare for as new instant payments regulations are considered in the EU, real-time payments get a boost in the US with the July launch of the FedNow service and ISO 20022 takes hold in the UK. Real-time is not the only significant event, and you’ll see that reflected in this collection here. We’re tried to gather all the available information for significant events and then we’ve enlisted Bottomline’s subject matter experts to check in with advice on how banks can best prepare for them. We’ll start in the UK, where the long-awaited and oft-postponed ISO 20022 has truly landed.

ISO 20022 has almost as many deadlines as there are payments platforms and countries that use them. For the uninitiated it is a data-rich, machine learning-driven messaging format that is most useful when riding alongside real-time, or instant, payments and settlements. It is essential (read mandated) when real-time payments are combined with cross-border payments. In the UK, March 20 was a significant milestone with the beginning of the SWIFT Co-existence Period for CBPR+ and the hard cutover to ISO 20022 for the Target 2 payments platform.

As Edward Ireland, Bottomline’s head of product for messaging and connectivity says, “we are now into a world in which ISO 20022 is globally ‘normal’ for payments. It’s certainly not the final chapter for implementing ISO 20022 but it is the beginning of it. We now know what it means to use the defacto standard for payments messaging. For financial institutions this means careful consideration of what they need to do to manage and leverage this new standard. How do you get ready for the new structure and granularity of information shared? What new data do you need to and want to process and use? How will you use ISO 20022 to make the bridge between different payment rails and protocols? Now is the time to engage and start answering these questions.”

UK: Confirmation of Payee

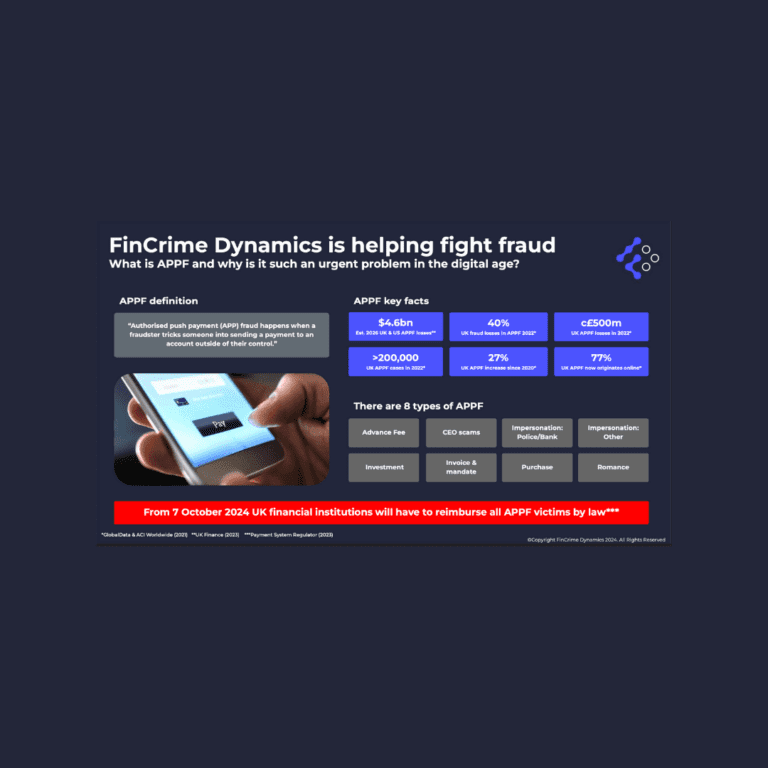

As we said earlier, it’s not all about payments in the UK. Protecting them is on the docket as well. Confirmation of Payee has its own set of deadlines that will be relevant to banks as well as corporates. We like Barclays definition of the service: “CoP is a service that checks account and reference details when a new CHAPS, Faster Payment or standing order is set up. This helps to make sure payments aren’t sent to the wrong account by mistake.” It was designed as a hedge against authorized push payment fraud. According to UK Finance, losses for APP fraud stood at £583 million in 2021; up 22 per cent from 2020. In a sign CoP could be working, the first half of 2022 saw £249 million in APP losses. In May of last year, the Payment System Regulator issued specific directions to about 400 payment service providers (PSPs) to implement a system to offer CoP to their customers. The upcoming October 31, 2023 deadline mandates CoP usage by a group of 32 institutions mixed among large banks (Citi), building societies (Yorkshire) and fintechs (Revolut). Group 2, which is mostly the balance of banks and PSPs, will come online October 31, 2024.

Although October might look like plenty of time to hit a deadline, Bottomline’s senior product manager Mark Bish says banks will delay onboarding at their own peril. “My understanding is that there is a fair amount of Group 1 banks that haven’t started the onboarding process as yet. This means they’re giving themselves a real challenge in complying with the Payments Systems Regulator’s directive. I would say they need to decide to move forward, pick their provider and get a project plan in place or they’re not going to hit the October deadline. They’re under a lot of pressure, which I understand. But October will come up very quickly.”

EU Instant Payments Proposals

On the continent all eyes are on the proposed instant payments regulations handed down late last year. By now the four pillars of this proposal have been in the market for about six months, giving various entities time to support or express opposition. Those pillars are: 1) Making Euro payments universally available 2) Make them affordable for consumers; 3) Mandate verification between the source identification and the payee; and, 4) Cross-check the customers with sanctions screening lists.

Those pillars have been almost unanimously supported. The timing has been an issue for financial institutions struggling with a slow economy. Frederic Viard, Bottomline’s Director of Global Marketing, Financial Messaging, told us that if the proposals are approved by the EU Finance Commission in September, it means that April 2024 is the date by which banks need to be able to receive instant payments in euros and September 2024 is the date by which they need to be able to send them. The European Banking Federation, which represents banks and PSPs in the EU, has proposed scaling back the implementation suggesting in a February 6 position paper that “the legal requirements should be limited to mandating reachability and to mandating the sending of single payment transactions through one online channel in the euro area.”

According to Viard, banks with legacy infrastructure face the most urgency to prepare for the inevitability of instant payments. They could decide to build new digital infrastructure in house or collaborate with partners to move to the necessary SaaS-based environment.

“Even then you will need to undertake a substantial integration project because you need to make your system’s back end able to connect so that you can optimally manage liquidity management,” he says. “It’s a big project and goes beyond taking a payment and making it faster. You must change the architecture because you need to be on 24/7 and then manage the orchestration necessary to make it efficient. Another option would be to rely on a third-party sponsor bank, acting on your behalf. This might be easier in terms of integration, but costs might be significant.”

FedNow’s July launch

In the US the action has been and will continue to be centered around the Federal Reserve’s FedNow platform. The Fed had previously set a window of May – June to launch. That has now been firmed up to launch in July. The most recent communication from the Fed happened just last week (March 30), when Allison Baller, vice president of FedNow industry readiness, told attendees at the Northeast Acquirers Association conference in Boston that the launch will have a “default limit” (as expected) of $100,000. According to the Fed this limit can be adjusted by banks using the service. In addition, the Federal Reserve “will evaluate the credit transfer limit on an ongoing basis and adjust as appropriate.” That limit currently sits at $500,000 compared to the $1 million transaction limit set by The Clearing House.

According to Digital Transactions, “Baller expects a subset of the approximately 120 financial institutions in the FedNow pilot to go live in July with another group she characterized as fast followers later. The pilot, which began in 2021 after more than 110 organizations expressed interest in it, included financial institutions of all sizes, but the initial group for the commercial service may not include smaller ones, Baller said. While they may need more time, “They helped shape the product,” she said.

Bottomline’s Vice President and Head of Product Management for Digital Banking Solutions Jessica Cheney has been involved with the Fed launch through its partnership program. She told us recently that the time for waiting for the Fed to launch is over.

“We’re beyond that wait-and-see period of time,” she said. “We know what the message sets are. We know what the production or live dates are going to be. We know pricing. We know who their technology partners are. We know that demand for real-time or instant payments is here and growing, so, putting all those things together, I really don’t see what we should wait for. The longer you wait, the less you will be seen as a progressive payments’ innovator, and the more you’ll be seen as a technology laggard and beaten to the punch by your more aggressive competitors.”

COVID finally fading

Although it isn’t tied specifically to business payments there is evidence that the COVID-19 crisis is less affecting consumer and business behavior. Two milestones point to the crisis’ being downgraded and even ending. On March 28 the County of Los Angeles officially ended its COVID restrictions and on the 30th the World Health Organization revised its vaccine advice to exempt teens and young children.

According to Bottomline’s Paymode-X VP of solutions marketing Paul McMeekin, it’s time to adjust. “For accounts payable teams and finance functions post-pandemic, it’s all about making the new normal work for you,” he says. “Remote work is here to stay, automation is growing in sophistication, and the way we processed invoices and payments before the world turned upside down is no longer tenable. That means accepting that the old ways don’t work and truly embracing process improvements, improved awareness and prevention of fraud risks and figuring out how your team works best.”

Log in to access complimentary passes or discounts and access exclusive content as part of your membership. An auto-login link will be sent directly to your email.

We use an auto-login link to ensure optimum security for your members hub. Simply enter your professional work e-mail address into the input area and you’ll receive a link to directly access your account.

Instead of using passwords, we e-mail you a link to log in to the site. This allows us to automatically verify you and apply member benefits based on your e-mail domain name.

Please click the button below which relates to the issue you’re having.

Sometimes our e-mails end up in spam. Make sure to check your spam folder for e-mails from The Payments Association

Most modern e-mail clients now separate e-mails into different tabs. For example, Outlook has an “Other” tab, and Gmail has tabs for different types of e-mails, such as promotional.

For security reasons the link will expire after 60 minutes. Try submitting the login form again and wait a few seconds for the e-mail to arrive.

The link will only work one time – once it’s been clicked, the link won’t log you in again. Instead, you’ll need to go back to the login screen and generate a new link.

Make sure you’re clicking the link on the most recent e-mail that’s been sent to you. We recommend deleting the e-mail once you’ve clicked the link.

Some security systems will automatically click on links in e-mails to check for phishing, malware, viruses and other malicious threats. If these have been clicked, it won’t work when you try to click on the link.

For security reasons, e-mail address changes can only be complete by your Member Engagement Manager. Please contact the team directly for further help.