What is this article about?

The results of The Payments Association’s consumer behaviour survey focussing on payment preferences and trends.

Why is it important?

It highlights key insights into how different demographics prefer to pay, providing valuable information for businesses and policymakers.

What’s next?

The findings will help guide future decisions on payment methods and innovation in the financial sector.

Table of Contents

In August, The Payments Association conducted a targeted survey to better understand the evolving payment preferences of UK consumers. The YouGov analysis institute conducted the survey, which engaged 2,069 participants and was undertaken between 19-20 August and representative of all UK adults 18+.* The findings provide a nuanced picture of how diverse demographic groups manage everyday transactions—whether through cash, cards, or emerging digital payment methods. The insights gathered offer payments professionals a comprehensive view of the trends shaping the current landscape, highlighting key variances in behaviour across age, region, and income.

For payments leaders, these findings are not just informative but essential for shaping future strategies. As digital solutions gain traction and the use of cash declines, understanding the underlying factors driving these changes is crucial. The results offer a clear direction for industry stakeholders, outlining opportunities for innovation while ensuring that financial inclusion remains a priority. This data-driven analysis will help guide the development of payment systems that are adaptable, inclusive, and aligned with the needs of today’s diverse consumer base.

* All figures, unless otherwise stated, are from YouGov Plc. Total sample size was 2069 adults. Fieldwork was undertaken between 19th – 20th August 2024. The survey was carried out online. The figures have been weighted and are representative of all UK adults (aged 18+)

Overview

The survey reveals clear trends in how UK consumers are adapting to changes in payment technologies. Contactless debit cards are the most widely used method for everyday transactions, particularly among younger consumers and women. Mobile wallets, such as Apple Pay and Google Pay, are also gaining popularity, especially with younger demographics, while cash use remains prevalent among older generations and lower-income groups. This shift towards digital payments highlights the growing reliance on convenience and speed.

Despite the increasing popularity of digital payments, cash remains a significant part of the payment landscape for many. Older consumers, lower-income households, and those in certain regions continue to favour cash, using it regularly for budgeting and financial control. There are also regional differences in payment preferences, with higher rates of cash usage in Northern Ireland and the Midlands, contrasting with greater digital adoption in London and the South East.

The data also indicates that while new technologies like wearable payment devices and cryptocurrencies are on the rise, their adoption remains limited. Most consumers have not yet integrated these methods into their daily routines, preferring more established digital or traditional payment methods. These findings paint a picture of a payment landscape in transition, where innovation is rapidly transforming consumer behaviour, but long-standing habits and preferences still play a crucial role.

Industry commentary

Frequency of using cash for everyday purchases

Cash remains an important payment method for many consumers despite the rise of digital alternatives. The frequency of cash usage is shaped by factors like convenience, budgeting preferences, and access to digital payments. Understanding how often consumers use cash provides insight into its enduring role in everyday transactions amid a shifting payment landscape.

Findings analysed

The data on cash usage highlights key differences across demographic groups. While 22% of respondents use cash more than once a week, 6% never use it, illustrating a divide in financial habits. This gap may be influenced by access to digital payment methods, personal preferences, or a reliance on cash for budgeting. As digital payments grow in popularity, those who depend on cash, particularly in rural or lower-income areas, could face potential exclusion if cash becomes less accessible.

Gender and age are notable factors in cash usage. Men (41%) use cash more frequently than women (33%), potentially due to different spending patterns or industries where cash is more common. Older individuals (55+) are also significantly more likely to use cash regularly (45%) compared to younger people (18-24) at 36%. This generational divide suggests that older adults, more familiar with cash, could face challenges as payment options shift toward digital alternatives.

Regional and social class differences also stand out. Northern Ireland has the highest rate of cash usage (58%), while the South has the lowest (30%). Cash use is more frequent among lower social grades (42% in C2DE) than higher ones (33% in ABC1), reflecting financial habits linked to managing tight budgets. Similarly, unemployed individuals (38%) and retirees (46%) rely more on cash compared to full-time workers (30%), indicating that those with fixed or lower incomes may find cash essential for daily management. These patterns underscore the potential for financial exclusion if the shift to cashless systems doesn’t consider these groups.

Key insights

- Cash usage frequency: 22% of respondents use cash more often than once a week, while 15% use it once a week. However, 6% of people never use cash, showing a divide in cash usage habits.

- Gender differences: Men (41%) are more likely to use cash at least once a week compared to women (33%), indicating a higher reliance on cash for frequent purchases among men.

- Age and cash: Cash usage increases with age, with 45% of people aged 55+ using it at least once per week. In contrast, younger people (18-24 years) are less frequent cash users, with only 36% using it weekly.

- Social class influence: The C2DE group (lower social grades) uses cash more frequently, with 42% using it at least once a week, compared to 33% of the ABC1 group (higher social grades). Lower social grades show more dependence on cash for everyday purchases.

- Regional variations: Northern Ireland has the highest rate of cash usage, with 58% using it at least once a week, while the South has the lowest weekly usage (30%).

- Working status and cash use: Unemployed individuals (38%) and retirees (46%) are more frequent cash users compared to full-time workers (30%). This suggests that non-working populations rely more on cash for regular purchases.

- Marital status and cash frequency: Widowed individuals (33%) use cash more than once a week, the highest of any marital status group. Married individuals use cash less frequently, with only 21% using it that often.

- Children and cash use: Families with three or more children are the most frequent users of cash, with 44% using it at least once a week, while families with no children show lower cash usage frequency (37%).

- Parents’ cash habits: Parents with older children (17-18 years) and those with children over 18 years use cash more frequently than parents with younger children, with 45% of parents with adult children using cash at least once a week.

- Social media users and cash: Skype users are the most frequent cash users, with 48% using cash at least once a week, compared to LinkedIn users (29%). Social media preferences appear to correlate with how often people use cash.

Preferred payment method for everyday purchases

As consumers increasingly embrace convenience and speed, their choice of payment methods for everyday purchases reflects evolving habits and technological advancements. From contactless cards to mobile wallets, preferences are shifting towards more seamless digital solutions. However, traditional methods such as cash and credit cards still hold importance for certain segments of the population. Understanding the factors behind these choices provides insight into how consumers navigate the growing array of payment options available today.

Findings analysed

The data reveals clear trends in payment preferences, with contactless debit cards being the most popular (29%), especially among women (35%) compared to men (24%). This convenience appeals to quick transactions but may leave behind those less familiar with digital payments, such as older or rural populations. Mobile wallets like Apple Pay and Google Pay are also on the rise, with 175 claiming they are their preferred payment method for everyday purchases, particularly among younger people (29% of 18-24-year-olds), who are more comfortable with digital technology. However, the shift towards mobile payments may deepen the digital divide, excluding those without access to smartphones.

Cash remains important for 13% of respondents, particularly men (15%) and lower-income groups (C2DE) (19%), who may rely on it for budgeting. Credit cards are less favoured overall, with 6% preferring chip and pin and 9% preferring contactless credit cards, primarily among older individuals. Regional differences are evident, with the South favouring contactless payments more than Northern Ireland, while socio-economic factors also influence preferences. For instance, higher-income groups and full-time students are more likely to adopt mobile wallets, while unemployed individuals remain more reliant on cash.

Family dynamics also affect payment choices. Larger households (with three or more children) are more likely to favour debit cards (52%) and contactless debit card options (33%), drawn to the convenience these methods offer. However, if cash options dwindle, some families may struggle to adapt, particularly when using cash to budget or teach financial habits.

Key insights

- Contactless debit cards dominate: Contactless debit cards are the most preferred payment method (29%), with preference being particularly high among females (35%) compared to males (24%).

- Mobile wallets are gaining popularity: Mobile wallets, such as Apple Pay and Google Pay, are prefered by 17% of respondents, with younger users (18-24 years) showing the highest adoption at 29%.

- Cash still holds value among certain groups: Despite the rise of digital payments, 13% of respondents still prefer cash, with higher preference amongst males (15%) and those from lower social grades (C2DE) (19%).

- Credit card preference is low: Both chip and pin (6%) and contactless credit card (9%) methods are less preferred compared to debit cards.

- Social media usage correlates with payment preferences: Snapchat and LinkedIn users are the most likely to favour mobile wallets (27%), while WhatsApp users show a strong preference for debit cards (48%).

- Regional disparities in payment preferences: In the South, 35% of respondents prefer contactless debit cards, while Northern Ireland shows the lowest preference at 20%.

- Generational divide in payment methods: Younger people (18-24) are more likely to favour mobile wallets (29%), while older individuals (55+) are more inclined towards traditional methods like credit cards with chip and pin (9%).

- Affluence and technology adoption: Higher social grades (ABC1) are more likely to favour mobile wallets (21%) compared to lower social grades (C2DE) (12%).

- Employment status influences payment choices: Unemployed individuals are more likely to claim cash is their preferred method (24%) than full-time workers (10%). Full-time students show the highest preference for mobile wallets (26%).

- Family dynamics impact payment preferences: Households with three or more children prefer debit cards (52%) overall, particularly contactless debit cards (33%), compared to households without children.

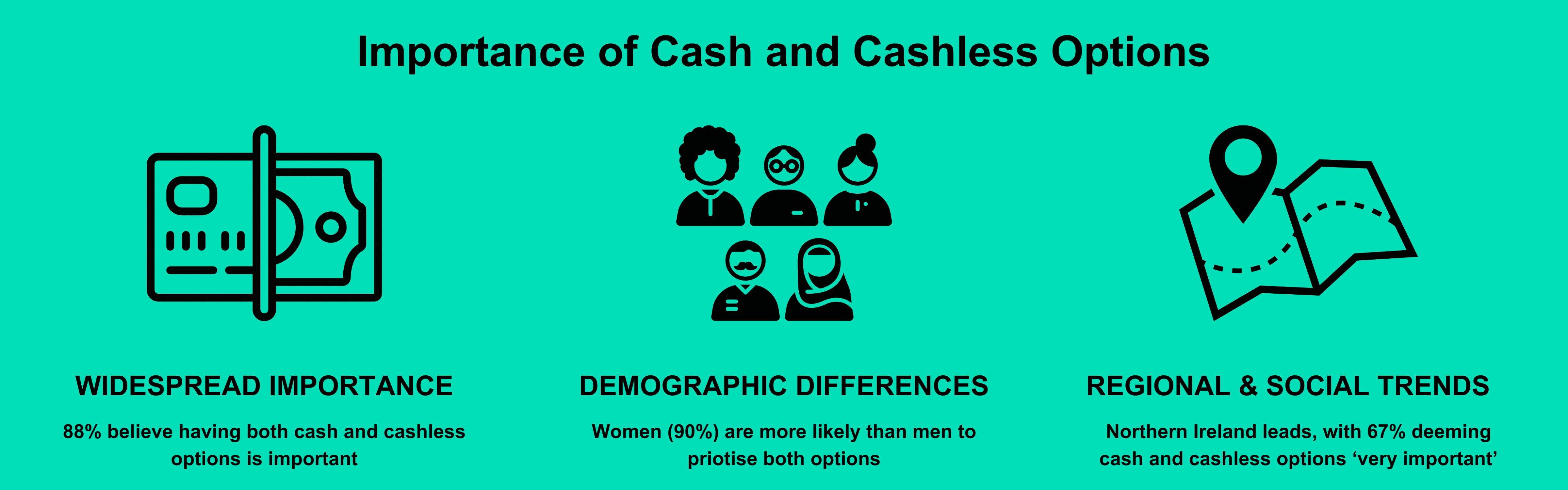

Importance of cash and cashless options

As the payments landscape continues to evolve, the balance between cash and cashless options remains a critical issue for consumers. While digital payments offer convenience and speed, cash still holds significant value for many, particularly for budgeting and accessibility. Ensuring that both options are available is vital in catering to a wide range of consumer needs and preferences, especially as different groups—by age, income, and region—rely on these methods in varying ways.

Findings analysed

A notable 88% of respondents value having both cash and cashless payment options, with 62% considering it “very important.” This indicates a strong desire for flexibility, allowing consumers to choose payment methods that suit their needs, particularly in a rapidly changing digital landscape. Without this dual availability, those who rely on cash for budgeting or who lack access to digital payments could face difficulties.

Women (90%) are slightly more likely than men (86%) to prioritise both payment options to some degree, with 65% of women rating it as “very important.” Similarly, older respondents (55+) place a degree of importance on having both options (94%) compared to 25-34 year olds (81%). Lower-income groups (C2DE) also show a high lever of importance, with 90% prioritising both options to some degree, more than higher-income groups (87%).

Regional differences are evident, with Northern Ireland (67%) and Wales (66%) rating maintaining both cash and digital payments as ‘very important’ compared to London (57%). Retired individuals (75%) and households containing three or more children (64%) similarly say it’s very important to have both options.

Key insights

- Widespread importance: A significant 88% of respondents believe that it is important to have both cash and cashless payment options, with 62% saying it is “very important” and 26% saying it is “fairly important.”

- Gender differences: Women (90%) are more likely than men (86%) to consider having both payment options important. Additionally, 65% of women view this as “very important” compared to 60% of men.

- Age gap: Older respondents (55+) place a higher value on having both cash and cashless options, with 75% saying it’s “very important.” In contrast, only 42% of 18-24 year-olds feel the same way, reflecting a generational divide.

- Social class influence: Those in lower social grades (C2DE) are more likely to see cash and cashless options as “very important” (67%) compared to those in higher social grades (ABC1), where 58% feel the same.

- Regional variations: Northern Ireland (67%) and Wales (66%) have the highest percentage of people who find cash and cashless options “very important,” whereas London (57%) and the East of England (60%) show lower levels of importance.

- Retired people prioritise both options: Retired individuals are the most likely to consider these payment options important, with 94% of them supporting the need for both. This compares to 84% of full-time workers and 82% of full-time students.

- Family dynamics: Households with three or more children are more likely to find cash and cashless options “very important” (64%), reflecting the added convenience that multiple payment methods may offer to larger families.

- Widowed individuals’ strong preference: Widowed respondents place the highest emphasis on the importance of having both payment options, with 75% viewing it as ‘very important’, in contrast to only 54% of those who have never married.

- Younger audiences are more flexible: Younger people, particularly those aged 18-24, show the lowest percentage (82%) of considering cash and cashless options very of fairly important, indicating greater comfort with purely digital payment methods.

- Social media influence: Facebook Messenger (64%) and WhatsApp (61%) users are among the most likely to view cash and cashless options as “very important.”

Frequency of using wearable payment device for everyday purchases

Wearable payment devices, like smartwatches and fitness trackers, represent a growing trend in digital payments. These devices offer a quick and contactless way to make transactions, seamlessly integrating into everyday life. However, their adoption remains limited, influenced by factors such as cost, awareness, and preference for traditional payment methods. As technology becomes more integrated into daily routines, wearables have the potential to reshape future payment habits.

Findings analysed

The low adoption rate of wearable payment devices (79% never using them) indicates a slow integration into daily life. Factors like the cost of wearables, limited awareness, and preference for established methods such as mobile wallets contribute to this hesitation. As a result, businesses may be cautious in investing in wearable payment infrastructure, which can further slow acceptance of this technology.

Younger individuals (18-24) use wearables more frequently (16% weekly), reflecting their comfort with technology and desire for convenience. In contrast, older adults (55+) remain reluctant, with 92% never using wearables. This generational gap suggests that widespread adoption could be challenging unless older demographics are better informed about the benefits of these devices.

Social grade plays a role, as those in higher-income brackets (ABC1) use wearables more often, likely due to greater disposable income and access to premium technology. Meanwhile, lower-income individuals may find wearable devices too expensive or unnecessary. This divide could widen inequality in access to emerging payment technologies if wearables become more prevalent.

Regional variations show London leading in wearable device usage (16% weekly), likely due to its tech-forward environment, while areas like Northern Ireland (7%) and Wales (6%). Similarly, wearable payment use is linked to social media engagement, particularly among younger, tech-savvy users. However, the low adoption among retired and widowed individuals suggests potential financial exclusion if wearables become more mainstream.

Key insights

- High non-usage: A large majority of respondents (79%) reported never using wearable payment devices for everyday purchases, reflecting a low adoption rate.

- Weekly use: Only 7% of respondents use wearable payment devices more than once a week.

- Gender differences: Men and women are similar in using wearable payment devices more than once per week (both at 7%), while 11% of men and 8% of women use wearable payment devices at least once per week.

- Age influence: Younger individuals aged 18-24 are more likely to use wearable payment devices at least once a week (16%), while older individuals (55+) show the lowest weekly usage (4%) and the highest rate of never using them (92%).

- Social grade impact: Those in the higher social grade (ABC1) are more likely to use wearable payment devices frequently, with 8% using them more than once a week, compared to 6% in the lower social grade (C2DE).

- Regional variations: London leads in wearable payment device usage, with 16% using them at least once a week, while Northern Ireland (6%) and Wales (6%) show the lowest usage.

- Retirement and usage: Retired individuals are the least likely to use wearable payment devices, with 93% reporting that they have never used one.

- Household size: Individuals with three or more children in the household are the most frequent users of wearable payment devices, with 41% using them more than once a week and 41% using them at least once a month.

- Marital status: Widowed individuals are the least likely to use wearable payment devices (93% never using them), while those living as married show the highest rate of usage (17% using them at least once every six months).

- Social media correlation: Snapchat and TikTok users show the highest frequency of wearable payment device usage, with 14% of Snapchat users and 12% of TikTok users using them more than once a week.

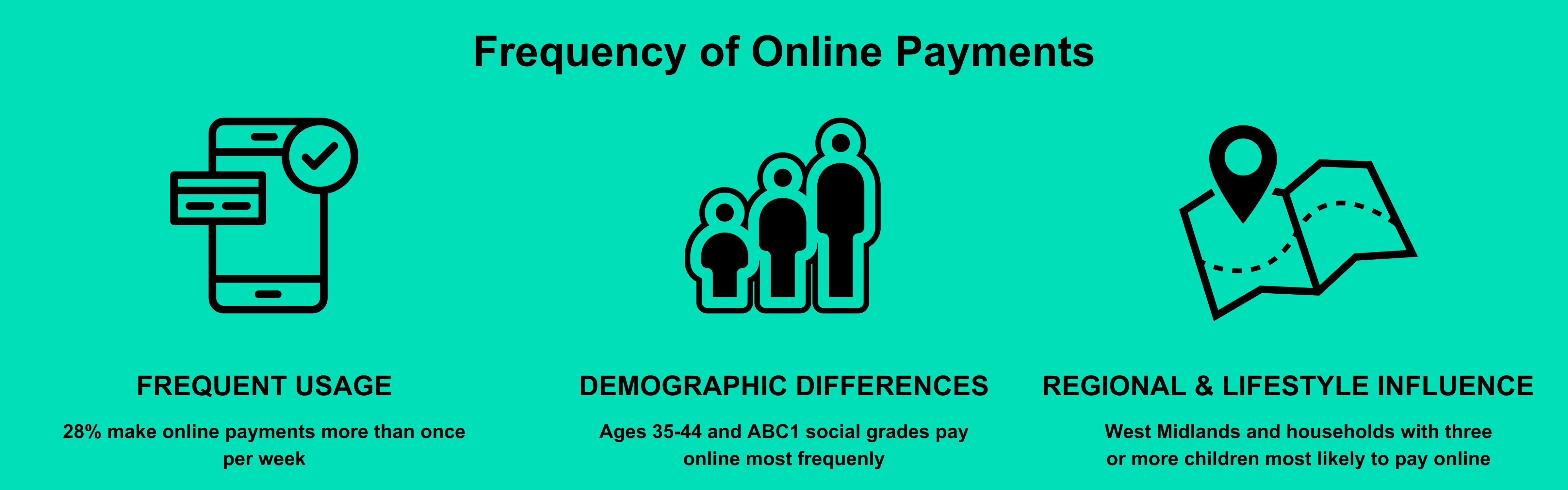

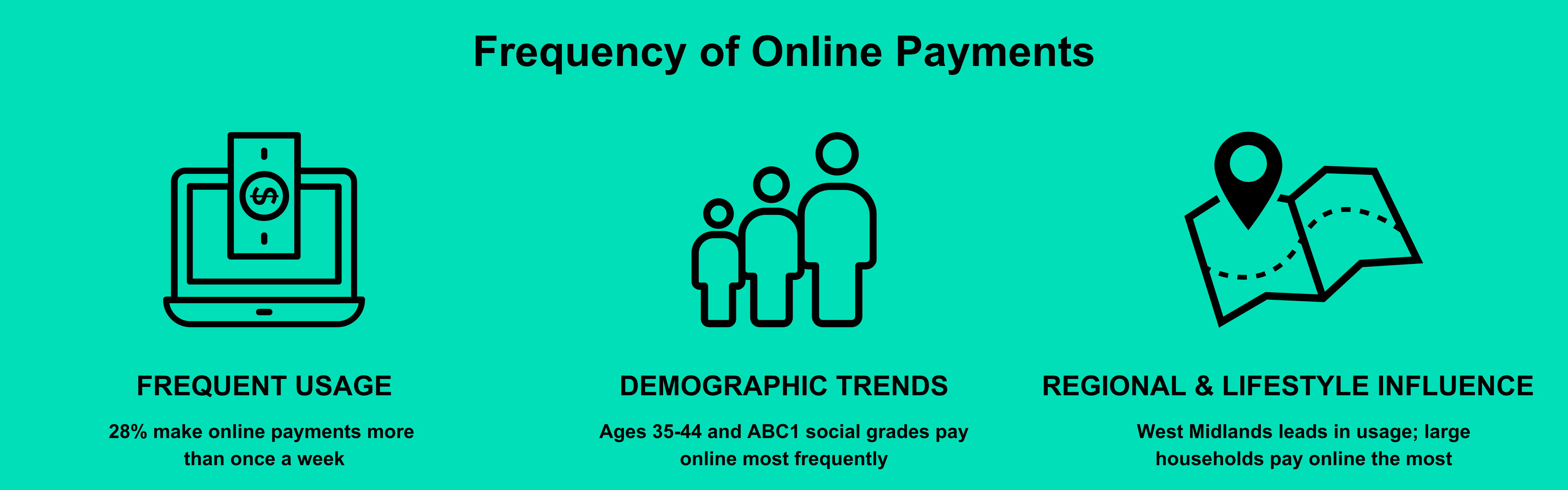

Frequency of making payments online

The frequency of making payments online has become a key aspect of modern consumer behaviour. As e-commerce and digital services continue to expand, more people are incorporating online transactions into their daily routines. This shift is driven by the convenience, speed, and variety of options that online payments provide. Understanding how often consumers engage in online payments can offer insights into their preferences and highlight areas for further innovation in the digital payment space.

Findings analysed

There is a growing trend toward frequent online payments, with 27% of respondents making transactions more than once a week. This indicates that online payments have become a regular part of daily life, driven by the convenience of e-commerce. To keep pace, businesses may need to enhance their online payment platforms to ensure a smooth user experience and maintain customer loyalty.

Men and women show similar online payment behaviours, suggesting that digital payments have become equally accessible across genders. This lack of a gender gap allows companies to focus on broadening their services without needing to target one specific group over another.

Individuals aged 35-44 are more frequent online payment users, reflecting their active roles in family, work, and e-commerce. In contrast, older adults (55+) use online payments less frequently, likely due to a preference for traditional methods or discomfort with digital transactions. As online payments continue to dominate, addressing the digital needs of older adults becomes crucial to prevent exclusion.

Higher social grades (ABC1) are more likely to make frequent online payments, while lower-income groups (C2DE) lag behind, possibly due to financial constraints or limited access to digital services. Regional variations also exist, with the West Midlands leading in usage (33% use more often than once per week) and Northern Ireland and Scotland showing lower engagement (22%), highlighting disparities in access and infrastructure that may need targeted initiatives to ensure inclusivity.

Key insights

- Frequent online payments: 27% of respondents make online payments more often than once a week, showing that regular online transactions are common.

- Gender similarities: Both males and females exhibit similar online payment behaviours, with 28% of males and 27% of females making payments more than once a week and 85% of males and 84% of females making payments at least once per month.

- Age group differences: The 35-44 age group has the highest frequency of online payments, with 37% making payments more than once a week, while younger adults (18-24 years old) are less frequent, with only 14% making payments at least once a week.

- Social grade impact: Individuals in the ABC1 social grade are more likely to make frequent online payments, with 31% making payments more than once a week compared to 22% of the C2DE group.

- Regional variations: The West Midlands leads with 33% of respondents making online payments more than once a week, while Northern Ireland has the lowest percentage of frequent online payers, with only 44% making payments at least once a week.

- Working status influence: Full-time workers have the highest frequency of online payments, with 34% making payments more than once a week, while full-time students have a much lower frequency (11%).

- Marital status effect: Respondents living as married are the most frequent online payment makers, with 34% making payments more than once a week, while widowed individuals report the lowest frequency (22%).

- Household size: Households with 3 or more children show the highest frequency of online payments, with 37% making payments more than once a week, compared to 25% for households without children.

- Social media influence: LinkedIn users are the most frequent online payment makers, with 36% making payments more than once a week, while users of X (formerly Twitter) exhibit the highest weekly payment frequency at 24%.

- High overall usage: Across all demographics, the majority of respondents (around 85%) make online payments at least once per month, reflecting the widespread adoption of online payment methods.

Preferred payment method for online payments

The preferred payment method for online transactions is a crucial aspect of consumer behaviour in the digital marketplace. With various options available—from debit and credit cards to digital wallets and online banking platforms—consumers choose methods based on convenience, security, and familiarity. Identifying these preferences helps businesses tailor their payment offerings, enhancing customer experiences and building trust in an increasingly digital economy.

Findings analysed

When it comes to online payments, debit cards emerge as the most preferred method, with 33% of respondents choosing them for their transactions. This popularity may stem from the straightforward nature and widespread acceptance of debit cards, offering a simple, direct way to manage funds. Credit cards rank second, preferred by 22% of respondents, indicating the appeal of added benefits like purchase protection and rewards points, especially for larger transactions.

Digital wallets and online payment platforms, such as Apple Pay, Google Pay, and PayPal, are equally favoured by 16% of respondents, showcasing a growing trend towards convenient, mobile-friendly payment options. Interestingly, alternative methods like cryptocurrency and Buy Now Pay Later services have minimal traction, with only 2% of respondents claiming they are their preferred method. This low adoption suggests a preference for more traditional and familiar payment methods in the online shopping space.

Gender and age play a role in payment preferences. Women slightly favour debit cards (34%), while men show a higher inclination towards credit cards (23%). Younger individuals (18-24) lean more towards digital wallets (24%), reflecting their comfort with mobile technology. In contrast, older adults (55+) prefer credit cards (29%) and debit cards (36%), indicating a reliance on more established payment methods.

Regional and social class differences also impact choices. In Northern Ireland, 38% prefer debit cards, the highest in any region, while credit cards are more popular in the East of England (28%). Higher social grades (ABC1) are more likely to prefer credit cards (24%) and digital wallets (17%), whereas lower-income individuals (C2DE) favour debit cards (30%) and digital wallets (22%), and larger households with three or more children prefer debit cards (32%) and digital wallets (22%), highlighting how lifestyle factors influence payment preferences.

Key insights

- Debit cards are most preferred: A significant 33% of respondents prefer using debit cards for online payments, making it the most commonly used method.

- Credit cards rank second: 22% of respondents prefer credit cards for online payments, showing a strong preference for card-based transactions.

- Digital wallets and online payment platforms: Both digital wallets (such as Apple Pay and Google Pay) and online payment platforms (like PayPal and Venmo) are equally preferred by 16% of respondents.

- Low adoption of cryptocurrency and buy now pay later: Only 2% of respondents prefer Buy Now Pay Later services, and 1% prefer cryptocurrency, indicating limited use of these alternative payment methods.

- Gender differences: Females slightly prefer debit cards (34%) over males (32%), while males are prefer credit cards (23%) compared to females (20%).

- Age influence: Younger individuals (18-24) have a higher preference for digital wallets (24%), while older adults (55+) prefer credit cards (29%) and debit cards (36%).

- Regional preferences: In Northern Ireland, 38% of respondents prefer debit cards, the highest among all regions, while 28% of East of England residents prefer credit cards.

- Social grade differences: ABC1 individuals are more likely to prefer credit cards (24%) and digital wallets (17%), whereas C2DE individuals show a stronger preference for debit cards (40%).

- Working status impact: Full-time workers (22%) prefer digital wallets compared to other groups, while retirees prefer credit cards (35%) for online payments.

- Household size and payment preferences: Households with three or more children show a high preference for debit cards (33%) and digital wallets (22%), while childless households prefer credit cards (24%).

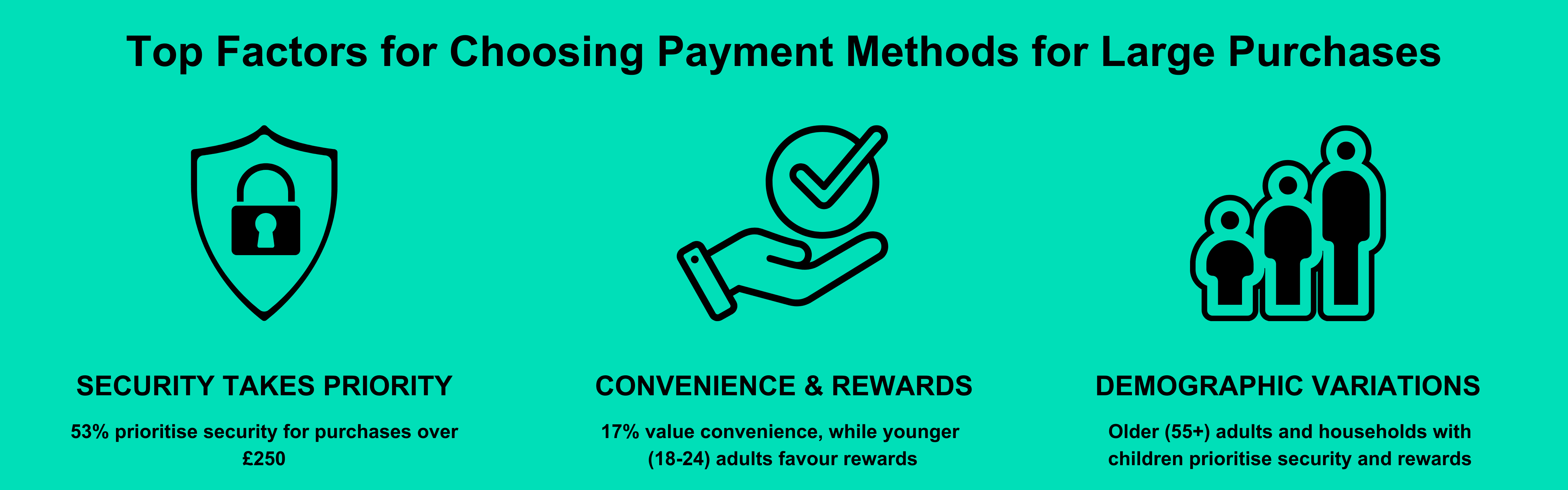

Factor most important when choosing payment method for large purchase

Findings analysed

When choosing a payment method for large purchases over £250, security emerges as the top priority, with 53% of respondents considering it the most important factor. This strong emphasis on security indicates that consumers are particularly cautious when making significant financial decisions, seeking reassurance and protection against potential fraud. Regional differences are evident, with security being more crucial in Wales (61%) and East Midlands (59%), while London places less emphasis on it (41%).

Convenience is a secondary factor, valued by 17% of respondents. Men show a slightly higher preference for ease of use (21%) compared to women (14%), indicating some variation in priorities between genders. Social media users, especially those on TikTok (19%) and X (formerly Twitter) (21%), also highlight convenience, suggesting that younger, digitally engaged consumers may lean towards more streamlined payment methods.

Rewards points and cashback are particularly appealing to younger adults, with 20% of 25-34-year-olds prioritising these benefits. This preference diminishes with age, as only 9% of those aged 55+ view rewards as important. Households with children also show a higher interest in loyalty benefits, with those having one child placing the most importance on rewards (19%) compared to childless households (12%).

Interest rates seem to play a minor role in decision-making, with only 4% of respondents citing them as the most important factor. However, widowed individuals display a higher concern for interest rates (9%), possibly reflecting greater sensitivity to borrowing costs. There is also a notable uncertainty among some groups, particularly women (12%) and young adults aged 18-24 (20%), who are more likely to be unsure about their payment priorities for large purchases.

Key insights

- Security is the top concern: An overwhelming 53% of respondents prioritise security when choosing a payment method for purchases over £250, making it the most important factor by far.

- Convenience is a secondary consideration: Convenience is important to 17% of respondents, with men (21%) placing a slightly higher value on ease of use compared to women (14%).

- Rewards points and cashback appeal to younger consumers: Rewards points or cashback are more important for younger adults, with 20% of 25-34 year-olds valuing these benefits. However, only 9% of those aged 55+ prioritise rewards.

- Interest rates are not a major concern: Only 4% of respondents consider interest rates for credit cards the most important factor when making large purchases, showing a low sensitivity to borrowing costs.

- Higher uncertainty among women and younger people: 12% of women and 20% of 18-24-year-olds selected “Don’t know” as their answer, indicating that these groups are more uncertain about their priorities when choosing payment methods for large purchases.

- Regional variations in security concerns: Security is most important in Wales (61%) and East Midland (59%), while London places the least emphasis on security (41%), reflecting regional differences in payment concerns.

- Households with children prioritise rewards: Households with one child place the highest importance on rewards points or cashback (19%), showing a greater focus on loyalty benefits compared to childless households (12%).

- Older adults prioritise security more: Security becomes increasingly important with age, with 60% of those aged 55+ rating it as the most critical factor, compared to only 42% of 18-24 year-olds.

- Widowed individuals concerned about interest rates: Interest rates are a greater concern for widowed individuals (9%), reflecting a higher sensitivity to borrowing costs compared to other marital status groups, such as married respondents (4%).

- Social media users and convenience: TikTok (19%) and X (formerly Twitter) (21%) users place a higher emphasis on convenience, while security is less of a priority for Snapchat users (43%), the lowest among all platforms.

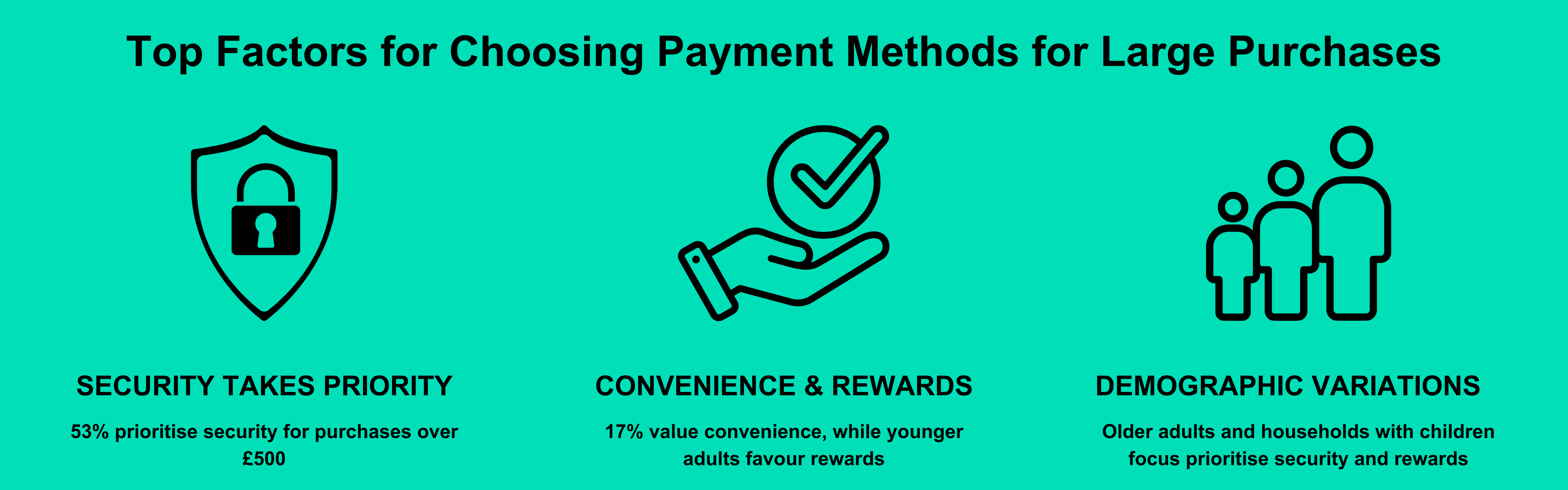

Preferred payment method for purchases abroad

The preferred payment method for purchases abroad is influenced by a variety of factors, including convenience, security, and familiarity with the payment option. When travelling, consumers may opt for different methods, such as cash, credit cards, or mobile wallets, based on their comfort and the perceived acceptance of these methods in foreign locations. Understanding these preferences can help businesses and payment providers offer solutions that cater to the unique needs of travellers, ensuring smooth and secure transactions internationally.

Findings analysed

Cash remains the most popular payment method when making purchases abroad, with 20% of respondents preferring it. Women show a higher preference for cash (22%) compared to men (17%). Retirees are more likely to prefer using cash abroad (24%), highlighting its role for those who may not be as comfortable with digital payment methods. Regional preferences also play a part, with cash being particularly popular in the North East (29%), while only 7% of respondents from Northern Ireland prefer to use cash abroad.

Mobile wallets, such as Apple Pay and Google Pay, are favoured by younger and male respondents. Overall, 7% of respondents use mobile wallets for purchases abroad, with 11% of 18-24-year-olds and 13% of 25-34-year-olds leading in adoption. Men are slightly more likely to use mobile wallets (8%) than women (6%), indicating a generational and gender divide in the use of digital payment methods abroad. London is the leading region in mobile wallet usage (10%), reflecting its tech-forward culture.

Travel debit cards appeal more to middle-aged travellers, with 11% of those aged 25-34 and 45-54 choosing this option. In contrast, younger and older age groups show less interest, with only 8% of 18-24 and 55+ age groups choosing travel debit cards. This preference extends to specific groups, such as separated or divorced individuals, where 12% favour travel debit cards over other payment methods.

Online banking platforms are another growing choice, particularly among full-time students (10%) and those in higher social grades (ABC1) (8%). Northern Ireland (14%) and Scotland (11%) strongly prefer these platforms, suggesting regional differences in payment behaviours. Interestingly, parents with children four and under still prefer cash (22%), while those aged 5-11 increasingly opt for contactless debit card payments (8%), reflecting changing needs based on family dynamics.

Key insights

- Cash is the most popular payment method overall: 20% of respondents prefer cash when travelling abroad, with women (22%) showing a higher preference than men (17%).

- Mobile wallets are favoured by younger and male respondents: Mobile wallets like Apple Pay and Google Pay are used by 7% of respondents, with 11% of 18-24-year-olds and 13% of 25-34-year-olds preferring them. Additionally, men (8%) prefer mobile wallets than women (6%).

- Travel debit cards appeal more to middle-aged travellers: 11% of respondents aged 25-34 and 45-54 prefer travel debit cards, while only 8% of younger (18-24 year olds) and older (55+) age groups preferring them.

- Regional variations in payment preferences: Cash is most popular in the North East (29%), while London leads in mobile wallet usage (10%). Online banking platforms are especially popular in Northern Ireland (14%) and Scotland (11%).

- Cash is most preferred among retirees: 24% of retired respondents prefer using cash, making it the group with the highest cash usage. In contrast, full-time workers (18%) and students (16%) have lower preferences for cash.

- Higher social grades favour digital payment solutions: 8% of ABC1 respondents prefer online banking platforms like Revolut and Monzo, compared to 6% of C2DE respondents, indicating greater adoption of digital payments by higher social grades.

- Parents with younger children prefer cash, but contactless payment is on the rise: 22% of parents with children aged four and under prefer cash, while 8% of parents with children aged 5-11 favour contactless debit card payments.

- Travel debit cards are popular among separated/divorced individuals: 12% of separated or divorced respondents prefer using travel debit cards, more than any other marital status group.

- Cash is less popular in London: Only 16% of Londoners prefer using cash for purchases abroad, compared to higher rates in other regions like the North and Midlands (23%).

- Online banking platforms are highly favoured by students: 10% of full-time students prefer online banking platforms for international purchases, showing higher adoption rates among younger, tech-savvy users

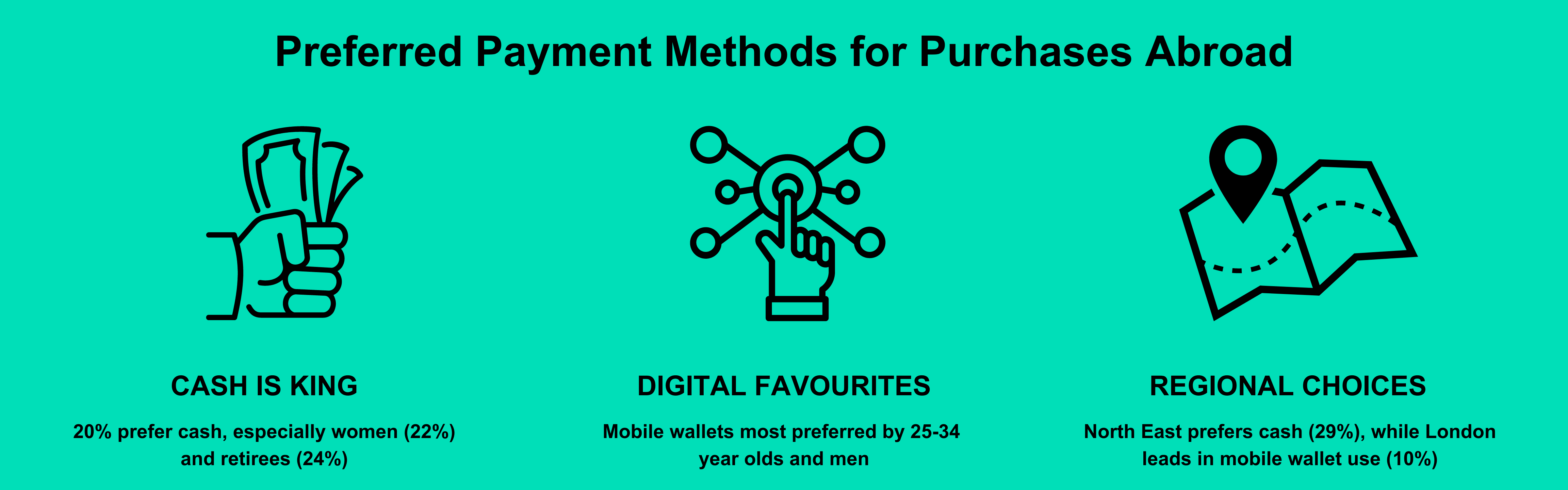

Types of fraud you've been a victim of

Experiencing fraud can significantly impact consumer trust in payment methods and digital transactions. The types of fraud individuals fall victim to, such as credit card and APP fraud, online scams, or identity theft, often shape their future payment behaviour and preferences. By understanding the common types of fraud affecting consumers, businesses and financial institutions can implement more effective security measures, provide better education on fraud prevention, and build a more secure payment environment.

Findings analysed

Credit card fraud is the most commonly reported type of fraud, affecting 14% of respondents, with both males (13%) and females (14%) experiencing it at similar rates. Notably, credit card fraud incidents increase with age, as 18% of individuals aged 55+ report being victims compared to just 4% of those aged 18-24. Retired individuals appear particularly vulnerable, with 17% falling prey to credit card fraud.

Despite these figures, a significant 53% of respondents have not been victims of any type of fraud, indicating that over half of the surveyed population has successfully avoided such incidents. However, online shopping fraud is the second most common, impacting 12% of respondents and affecting males and females equally. Phishing scams also remain a consistent threat, affecting around 4-5% of respondents across all age groups.

Younger people, particularly those aged 18-24, are more susceptible to social media scams, with 10% reporting being victims. In contrast, only 5% of individuals aged 55+ have experienced such scams. Additionally, romance scams are reported more by males (3%) than females (1%), suggesting differing vulnerabilities across genders.

Regional variations show that Northern Ireland has the highest percentage of individuals who have never been victims of fraud (68%), whereas London has the lowest rate (46%). Households with three or more children report higher incidences of credit card fraud (15%) and social media scams (12%) compared to those with fewer or no children, indicating that family size may also influence exposure to fraud.

Key insights

- Credit card fraud is most common: Credit card fraud is the most frequently reported type of fraud, affecting 14% of respondents, with a relatively even distribution across both males (13%) and females (14%).

- High non-victim rate: A significant 53% of respondents report never having been a victim of any type of fraud, showing that over half of the population surveyed has managed to avoid such incidents.

- Online shopping fraud: This is the second most common fraud type, with 12% of respondents having been affected. It’s equally prevalent among males and females.

- Age differences in fraud: Credit card fraud increases with age, with 18% of individuals aged 55+ reporting being victims, compared to only 4% of those aged 18-24. Younger people are more prone to social media scams (10% for 18-24 year-olds).

- Romance scams more common for males: Males are more likely to report being victims of romance scams (3%) compared to females (1%).

- Regional variations in fraud: Northern Ireland has the highest percentage of people who have never been victims of fraud (68%), while London has the lowest rate (46%), indicating regional disparities in fraud experiences.

- Phishing scams affect all age groups: Phishing scams affect around 4-5% of respondents across all age groups, showing that this type of fraud is equally distributed among different age brackets.

- Social media scams impact younger people: Social media scams are most prevalent among 18-24-year-olds, with 10% reporting being victims, whereas only 5% of those aged 55+ have experienced this type of fraud.

- Retired individuals and fraud: Retired individuals report the highest level of credit card fraud at 17%, showing that this group is more susceptible to such fraud compared to other working status categories.

- Families with more children report more fraud: Households with three or more children report higher incidences of credit card fraud (15%) and social media scams (12%) compared to households with fewer or no children.

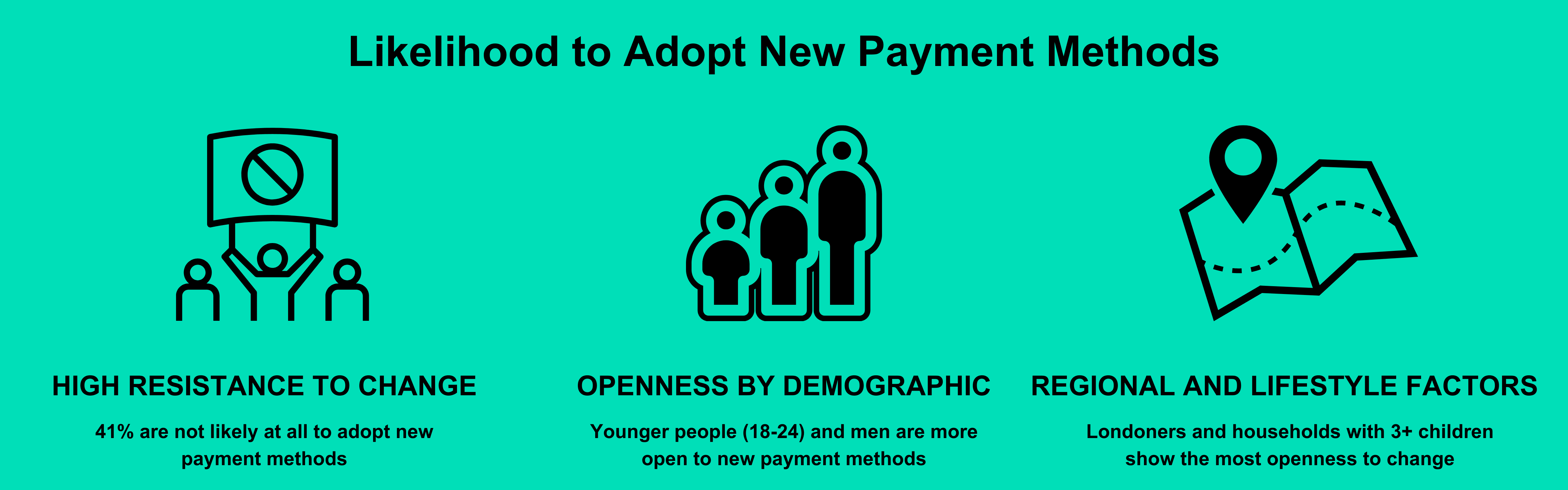

Likelihood to adopt a new payment method in future

The likelihood of adopting a new payment method in the future reflects consumers’ openness to change and their trust in emerging technologies. This willingness can be influenced by factors such as convenience, perceived security, and familiarity with digital innovations. Understanding these attitudes helps businesses and payment providers anticipate market trends, address consumer concerns, and design payment solutions that cater to evolving preferences while ensuring ease of use and security.

Findings analysed

There is a noticeable scepticism about adopting new payment methods, with 41% of respondents indicating they are not at all likely to change in the future. This resistance is particularly strong among older adults (55+), with 56% not likely at all to adopt new methods. On the other hand, younger individuals (18-24) show the most openness, with 38% very or fairly likely to try new payment options.

Gender differences are also apparent, as males are generally more open to adopting new payment methods (27% very/fairly likely) than females (15%). Conversely, 46% of females are not likely at all to consider new payment options, compared to 36% of males. Regional variations reflect a similar divide, with Londoners leading in openness (30% very/fairly likely), while residents of Northern Ireland are the most resistant, with 51% not likely at all to embrace new payment methods.

Social grade and working status further influence openness. ABC1 individuals are more likely (21%) to adopt new payment methods compared to those in the C2DE group (16%). Full-time students show the highest openness (33%), whereas retired individuals exhibit the most resistance, with 60% not likely to adopt new payment options.

Household dynamics also play a role. Families with three or more children are the most open, with 42% likely to adopt new payment methods. In contrast, households without children show greater resistance, with 71% not inclined to change. Parents of children aged four and under are notably more receptive (30%) than adults and guardians without children (62% unlikely). Social media use aligns with this trend, as Snapchat users are the most open to new methods (33%), while Facebook users are the least likely (21%) to adopt new payment options.

Key insights

- Scepticism about new payment methods: A large proportion of respondents (41%) are not likely at all to adopt a new payment method in the future, reflecting high levels of resistance to change.

- Gender differences: Males are more open to adopting a new payment method, with 27% saying they are likely, compared to only 15% of females. Meanwhile, 46% of females are not likely at all to adopt a new payment method compared to 36% of males.

- Age impact: Younger individuals (18-24) are the most likely to adopt new payment methods, with 38% likely to do so. On the other hand, older adults (55+) are the least likely, with 56% not likely at all to adopt any new methods.

- Regional variations: London leads in openness to new payment methods, with 30% likely to adopt, whereas Northern Ireland shows the highest resistance, with 51% not likely at all to embrace new payment methods.

- Social grade influence: ABC1 individuals show slightly higher openness, with 25% likely to adopt a new payment method, compared to 16% of C2DE individuals, showing that higher social grades might be more adaptable to changes in payment technology.

- Working status influence: Retired individuals are the most resistant to new payment methods, with 60% not likely at all to adopt them. Full-time students, on the other hand, are the most open, with 33% likely to adopt.

- Marital status: Widowed individuals are the most resistant, with 60% not likely at all to adopt a new payment method, while those never married show the highest likelihood, with 27% likely to adopt.

- Households with children: Households with three or more children are the most likely to adopt a new payment method, with 42% being likely, whereas households with no children are much less likely, with 71% not likely to adopt.

- Parent/guardian status: Parents/guardians of younger children (aged four years and under) are the most open, with 30% likely to adopt new payment methods, compared to adults without children, 62% of whom are not likely to adopt new payment methods.

- Social media users: Snapchat users are the most open to adopting new payment methods, with 33% likely to do so. X (formerly Twitter) users also show high openness (28%), while Facebook Messenger users are the least likely (21%) to adopt new payment methods.

Conclusion

The consumer behaviour survey results reveal a payment landscape in transition, where traditional methods like cash and credit cards coexist with emerging digital payment options. While there is a clear shift toward convenience and digital solutions, preferences vary widely across demographics, regions, and social grades. Younger individuals and those in higher-income brackets are leading the adoption of mobile wallets and contactless payments, while older adults, retirees, and lower-income groups continue to rely heavily on cash and more established payment methods.

Security remains a paramount concern when choosing payment options for large purchases, reflecting a cautious consumer mindset in the face of increasing fraud incidents. Similarly, while there is openness to adopting new payment methods, a significant portion of the population remains hesitant, particularly among older adults and those with fixed incomes. These insights highlight the importance for businesses, financial institutions, and policymakers to strike a balance between promoting innovative payment technologies and ensuring inclusivity and accessibility for all consumer segments.

As digital payment solutions continue to evolve, understanding these nuanced consumer behaviours will be essential in shaping future strategies. Businesses must offer a variety of secure, convenient payment methods while addressing the barriers faced by those less inclined to adopt new technologies. By acknowledging and catering to these diverse preferences, the financial sector can navigate the ongoing transition toward a more inclusive and adaptable payment ecosystem.

Read more Payments Intelligence

Regulation Roadmap Q3

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Consumer behaviour 2026 report

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.

How AI-powered banking tools are failing vulnerable customers

New research shows vulnerable customers are strong adopters of AI and digital banking, but are far more likely to experience failed payment journeys and poorer outcomes.