What is this article about?

Key findings from the Half Year Fraud Report 2024 by UK Finance, detailing the evolving threats in payment fraud.

Why is it important?

It highlights the rising trends in fraud and stresses the need for payment leaders to implement stronger prevention strategies and collaborations.

What’s next?

Payment leaders must focus on fraud prevention, collaboration with tech and telecom sectors, and public education to mitigate future risks.

In the world of digital payments, fraud is an ever-present threat that continues to evolve, creating serious risks for both businesses and consumers. The Half Year Fraud Report 2024, published by UK Finance, paints a stark picture of how pervasive and damaging these schemes have become. In the first half of this year alone, over £570 million was lost to fraudsters constantly refining their tactics to exploit vulnerabilities. Particularly concerning is the growing sophistication of these attacks, which target personal and corporate accounts through increasingly convincing deceptions.

However, the fight against fraud is not without its successes. Financial institutions and payment providers are stepping up their efforts, and according to the report, more than £710 million in unauthorised transactions were thwarted during this same period. That said, the scale of the problem remains vast, with much of the fraudulent activity traced back to social media platforms and telecommunications channels—areas where tighter controls and collaboration are still needed.

This article breaks down the key findings from the Half Year Fraud Report 2024, providing payment leaders with insights into emerging threats and offering guidance on strengthening defences against this relentless challenge. From shifts in unauthorised card fraud to the evolving nature of authorised push payment scams, there’s a lot to unpack—and a lot at stake.

Key drivers of fraud in 2024

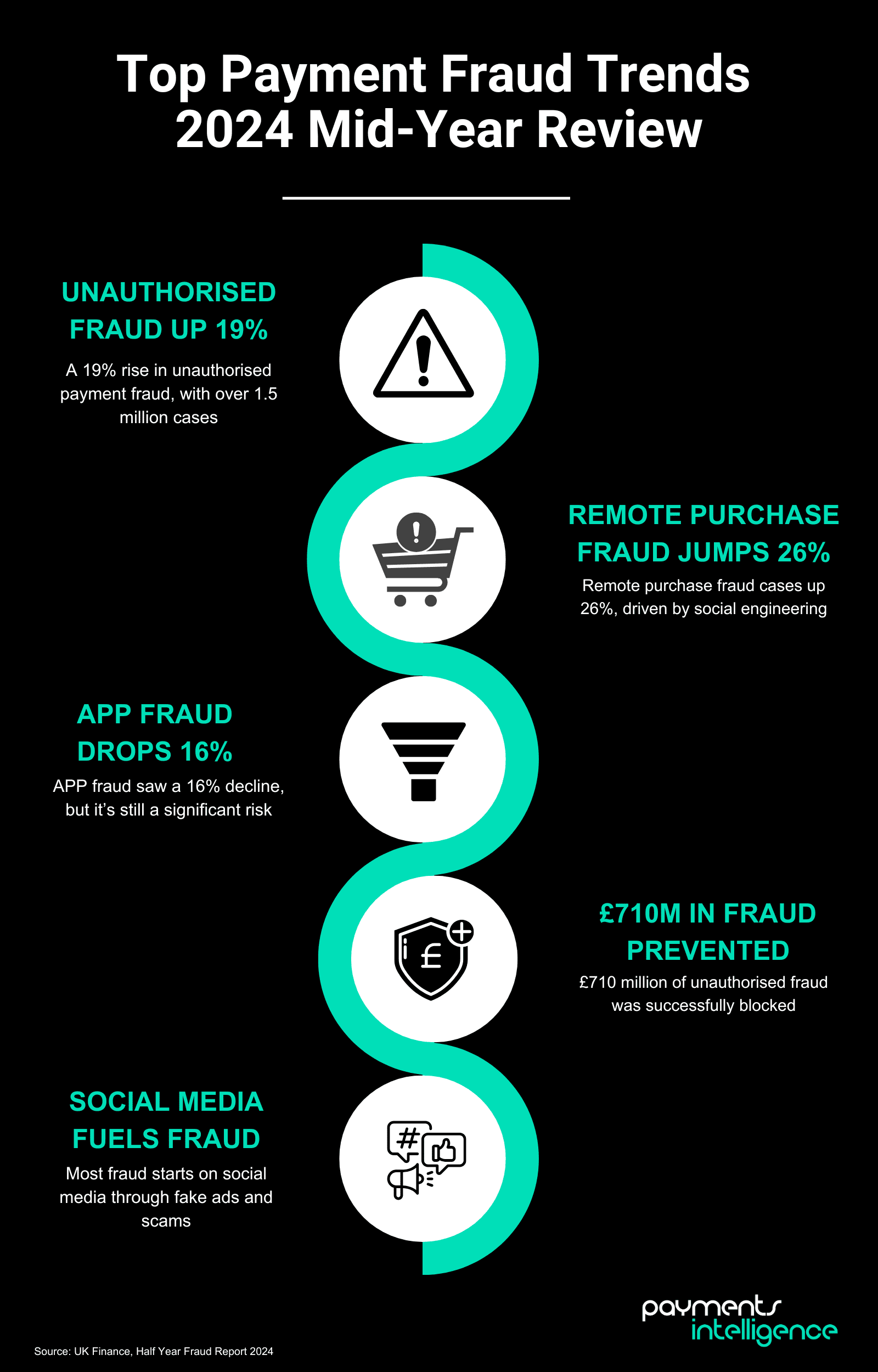

The Half Year Fraud Report 2024 highlights a clear rise in fraud cases driven primarily by unauthorised payment fraud. In the first half of the year, cases of unauthorised fraud surged by 19%, with criminals leveraging low-tech methods and digital deception to exploit vulnerabilities. Fraudsters are becoming increasingly adept at bypassing security protocols, often using social engineering techniques to convince victims to unknowingly hand over sensitive information. This has led to a noticeable uptick in card-related fraud, especially in remote purchases, where criminals use stolen card details for online transactions.

One of the most alarming trends identified in the report is the continued rise in social engineering scams, which now account for a significant portion of fraud activity. Social media platforms and telecommunications networks remain key enablers, as fraudsters use these channels to gain the trust of their victims before executing their schemes. Whether through fake profiles, phishing emails, or fraudulent advertisements, criminals are finding new ways to manipulate people into sharing their financial details or authorising payments.

While banks and payment providers are making strides in fraud detection and prevention, the report stresses the need for more robust collaboration with technology and telecom sectors. The data shows that without better cross-industry cooperation, it will be difficult to curb the tide of fraud that originates outside traditional banking systems. This underscores the urgent need for payment leaders to engage in wider partnerships to combat the evolving fraud landscape.

Authorised push payment (APP) fraud trends

Authorised push payment (APP) fraud remains one of the most significant challenges for payment leaders, as fraudsters increasingly target individuals and businesses by tricking them into authorising payments to criminal accounts. According to the Half Year Fraud Report 2024 from UK Finance, there has been a promising decline in APP fraud this year, with cases dropping by 16% and losses falling by 11% compared to the first half of 2023.

One of the key shifts in APP fraud this year involves the introduction of new reimbursement rules, which came into effect in October 2024. These build on the voluntary code in place since 2019 and aim to provide more consistent compensation for victims. However, as the report stresses, reimbursement alone is not a long-term solution. While it offers immediate relief to victims, it doesn’t address the root cause: stopping fraud at the source. Payment leaders must continue to focus on prevention strategies that address the social engineering tactics at the heart of APP fraud, alongside pushing for greater cooperation with telecom and tech platforms where much of this fraud is initiated.

Unauthorised payment fraud categories

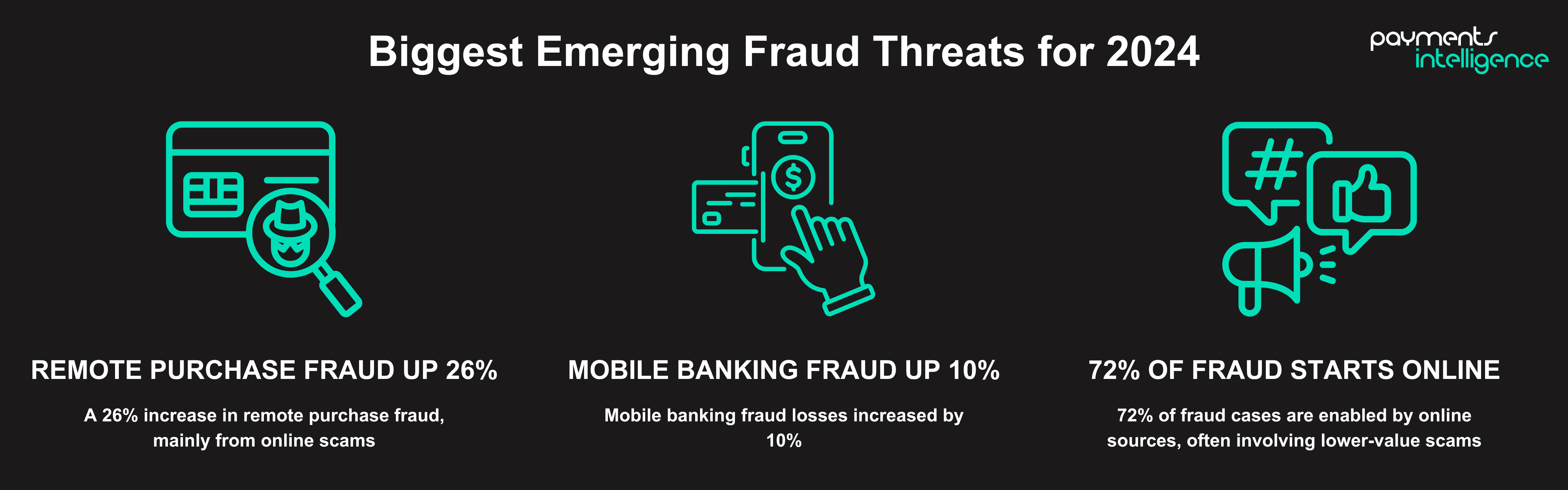

The Half Year Fraud Report 2024 reveals a concerning rise in unauthorised payment fraud, driven largely by card-related scams. Unauthorised fraud losses increased by 5% compared to the same period in 2023, with more than 1.5 million cases recorded. A significant driver of this trend has been the resurgence of remote purchase fraud, or card-not-present (CNP) fraud, which saw an 11% increase in losses and a staggering 26% rise in cases.

CNP fraud occurs when criminals use stolen card details to make purchases online, by phone, or via mail order. Despite the implementation of strong customer authentication (SCA) across the industry, fraudsters have adapted their tactics, often using social engineering methods to trick customers into revealing one-time passcodes (OTPs) required to authenticate transactions. This ability to bypass robust security measures highlights the persistent ingenuity of criminals in finding new vulnerabilities.

Lost and stolen card fraud losses increased by 4%, driven by traditional low-tech theft methods like distraction thefts and shoulder surfing, where criminals observe PINs at ATMs or point-of-sale terminals. This rise underscores the need for vigilance in both online and physical transactions.

While card-not-received fraud and counterfeit card fraud remain relatively low, both saw modest increases, reminding payment leaders that old-school fraud methods still pose a threat. The good news, however, is that banks and payment providers successfully prevented £558.6 million of card fraud during the first half of 2024, stopping approximately £6.68 in every £10 of attempted fraud. This success in prevention, though commendable, signals that fraudsters are relentless, and efforts to stay ahead of evolving tactics must continue.

Remote banking fraud insights

Remote banking fraud, covering internet, mobile, and telephone banking, continues to challenge the payment industry, even as advancements in security measures are made. The Half Year Fraud Report 2024 highlights some key shifts in this area, with overall losses from remote banking fraud decreasing by 2% in the first half of 2024 compared to the same period in 2023. While this decline is encouraging, it masks some important underlying trends that payment leaders should be aware of.

- Internet banking fraud, once a dominant form of remote fraud, saw a dramatic 37% drop in cases and an 11% reduction in losses. This can be attributed to the increasing sophistication of fraud detection tools, improved authentication measures, and greater consumer awareness of phishing scams.

- Mobile banking fraud, on the other hand, is on the rise, with a 10% increase in losses, reaching a new record high for the first six months of a year since data collection began in 2015. As mobile banking apps become the preferred platform for an increasing number of users, fraudsters have identified new vulnerabilities to exploit. With more consumers relying on their phones for banking transactions, the rise in fraud within this channel highlights the need for stronger in-app security features and user education on protecting their devices from attacks.

- Telephone banking fraud also increased, with losses rising by 20%. Fraudsters often use social engineering tactics, such as impersonating a bank representative, to trick customers into revealing their account details or authorising payments. This method can be highly effective, especially with vulnerable customers who may not be as familiar with the warning signs of a scam.

While there has been progress in reducing certain types of remote banking fraud, the rise in mobile and telephone banking fraud should serve as a reminder to payment leaders that fraudsters are constantly adjusting their tactics. Investment in consumer education, combined with continued innovation in fraud detection technologies, will be essential in mitigating these growing risks.re

Emerging APP scam types

The Half Year Fraud Report 2024 provides a detailed breakdown of APP scams. While the overall number of APP fraud cases has declined, several types of scams within this category remain prevalent and costly, posing ongoing challenges for payment leaders.

Purchase scams remain the most common form of APP fraud, making up 70% of all APP cases reported in the first half of 2024. These scams typically involve fraudsters advertising fake goods or services, often on social media or online marketplaces, and convincing victims to pay via bank transfer. What’s particularly worrying is that, despite increased awareness and prevention efforts, losses from purchase scams have reached their highest point since data collection began in 2020. With over £42 million lost in the first six months of the year, this form of fraud highlights the critical need for secure payment methods and enhanced customer education around recognising suspicious sellers.

Investment scams, while accounting for fewer cases, lead to the largest financial losses among APP scams, totalling £56.4 million in the first half of 2024. Criminals lure victims with promises of high returns, often using fake investment opportunities in areas like cryptocurrency, property, or gold. The combination of enticing returns and pressure tactics creates a sense of urgency that traps victims. These scams tend to involve higher-value transactions, making them financially devastating for those targeted. Despite a slight reduction in the number of cases, payment leaders need to be vigilant, especially as fraudsters continuously evolve their tactics.

Romance scams, though smaller in number, are notable for their emotional and psychological toll on victims. In these scams, fraudsters develop a relationship with their target, often over a prolonged period, before fabricating personal crises to solicit financial help. Losses from romance scams amounted to £14.5 million in 2024, a 21% decrease from the previous year but still a significant issue. This decline may reflect greater public awareness, but payment leaders should continue to support education campaigns aimed at preventing such emotionally manipulative crimes.

Advance fee scams, where victims are tricked into paying a fee with the false promise of a larger payout or goods in return, saw £15.8 million in losses in the first half of 2024—a 5% increase from the previous year. These scams often begin on social media or through unsolicited emails and letters, targeting individuals with claims of lottery wins, inheritances, or even job offers. The persistence of this type of fraud highlights the importance of continuously updating fraud detection systems and public messaging to ensure consumers remain cautious.

Preventative measures and recommendations for payments leaders

The Half Year Fraud Report 2024 provides crucial insights into the ongoing efforts by the banking and payments industry to combat fraud. Several key measures highlighted in the report have contributed to both the prevention of fraud and the reduction of fraud losses, particularly in unauthorised transactions.

1. Industry investment in fraud prevention

The banking sector continues to invest heavily in sophisticated fraud detection systems, and this is reflected in the 13% increase in prevented unauthorised fraud during the first half of 2024, amounting to £710.9 million. This equates to £6.65 of every £10 of attempted fraud being successfully blocked. These advanced detection tools have been particularly effective in areas like remote banking, where the value of prevented fraud rose by 34% compared to the previous year.

2. Collaboration with law enforcement and the Government

The report stresses the importance of ongoing collaboration between financial institutions, regulators, and law enforcement. For example, the Dedicated Card and Payment Crime Unit (DCPCU), a specialist police unit funded by the industry, continues to play a vital role in the fight against fraud. In 2023 alone, this partnership led to 149 arrests or interviews under caution and the recovery of nearly 25,000 compromised card numbers from criminal gangs. These collaborations are essential for disrupting organised crime and apprehending fraudsters.

3. Strengthening consumer awareness and education

UK Finance continues to lead public awareness campaigns like Take Five to Stop Fraud, encouraging individuals to pause and consider before sharing personal information or making payments. The report reiterates the importance of these efforts, especially as criminals increasingly use social engineering tactics to manipulate victims. Educating the public remains a key line of defence against fraud, particularly in combating authorised push payment scams, where victims are often deceived into authorising payments themselves.

4. New APP reimbursement rules

The introduction of new APP fraud reimbursement rules on 7 October 2024 marks a significant step in enhancing consumer protection. These new regulations are designed to increase the proportion of losses reimbursed to victims of authorised push payment scams, building on the existing voluntary code. The report notes that while these rules are crucial for victim compensation, prevention remains the ultimate goal. The focus is on ensuring that fraud is stopped before it happens, rather than relying on reimbursement after the fact.

5. The role of technology in prevention

The report highlights the growing sophistication of fraud techniques, particularly in circumventing security measures like Strong Customer Authentication (SCA). While SCA has helped reduce certain types of fraud, such as remote purchase fraud, criminals continue to evolve their tactics, including tricking customers into divulging one-time passcodes (OTPs). The industry’s investment in technologies to detect and prevent these sophisticated attacks remains a cornerstone of the fight against fraud.

Conclusion

UK Finance’s Half Year Fraud Report 2024 makes one thing clear: fraud remains a significant and evolving threat to both individuals and businesses in the UK. Despite advances in fraud prevention technology and industry-wide efforts to reduce losses, criminals continue to find new ways to exploit vulnerabilities in the payments ecosystem. The increase in unauthorised fraud and the persistence of social engineering tactics highlight the need for ongoing vigilance.

While the report notes some positive trends—such as the decline in authorised push payment (APP) fraud and the increased prevention of unauthorised transactions—the overall landscape remains challenging. Social media platforms and telecommunications networks are key enablers of fraud, and cross-industry collaboration will be essential to address these weaknesses.

For payment leaders, the insights from the Half Year Fraud Report 2024 serve as a reminder that the battle against fraud is far from over. Investment in fraud detection technologies, strengthened partnerships with law enforcement, and public education initiatives will continue to play crucial roles in mitigating the risks. Additionally, the new APP reimbursement rules introduced in October 2024 mark an important step toward ensuring fairer compensation for victims.

However, as the report stresses, reimbursement can only go so far. The ultimate goal must be prevention—stopping fraud before it causes financial or psychological harm. For payment leaders, this means staying ahead of the evolving tactics used by fraudsters, leveraging technology, and fostering a culture of security both within their organisations and among their customers. The fight against fraud is ongoing, and it will require constant adaptation and innovation to keep pace with the threats on the horizon.

Read more Payments Intelligence

Regulation Roadmap Q3

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Consumer behaviour 2026 report

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.

How AI-powered banking tools are failing vulnerable customers

New research shows vulnerable customers are strong adopters of AI and digital banking, but are far more likely to experience failed payment journeys and poorer outcomes.