The industry is moving towards AI-driven compliance, real-time data, and closer collaboration among banks, fintechs, and regulators.

May 12 2025

by Payments Intelligence

What’s the article about?

A recent Payments Association webinar which explored how technology, regulation, and collaboration are reshaping cross-border payments and the correspondent banking model.

Why is it important?

Cross-border payments support global trade but remain inefficient and risky; modernising them is key to financial inclusion and economic stability.

What next?

The industry is moving towards AI-driven compliance, real-time data, and closer collaboration among banks, fintechs, and regulators.

The cross-border payments model is undergoing a quiet but significant transformation. At The Payments Association’s cross-border working group’s recent webinar, “Rewiring the Cross-Border Payments Paradigm: Risk and Security in Correspondent Banking Confirmation,” a panel of experts from fintech, banking, legal, and regulatory backgrounds explored how emerging tools and frameworks are reshaping the industry.

As global markets continue to evolve, cross-border payments remain a critical pillar of international commerce. The Bank of England projects that the value of these flows will exceed $270 trillion by 2027. Despite progress, the infrastructure remains in flux. Underserved jurisdictions are becoming increasingly accessible, enabled by improved connectivity and more sophisticated partnerships. Yet much of the system still hinges on a half-century-old correspondent banking model and a fragmented regulatory landscape.

The panel explored how global trade, technology, and regulatory approaches are intersecting in this new landscape. What follows is a summary of the key themes that emerged.

While technology continues to outpace regulation, legal frameworks are still playing catch-up. Natalie Lewis, head of fintech, market infrastructure and payments at Travers Smith, highlighted the regulatory friction points that continue to constrain efficiency. Chief among them is de-risking. “Banks in developed economies are reducing their exposure to institutions in high-risk jurisdictions,” she noted, “leaving those players cut off and often reliant on less-regulated alternatives.”

Other persistent obstacles include inconsistent anti-money laundering (AML) rules and sanctions regimes across jurisdictions, which generate conflicting alerts and limit the scope for automation. Misaligned operating hours between central infrastructures further complicate matters, trapping liquidity and delaying settlement.

Pégeman Khorsan, chief legal and regulatory officer at RTGS.global, observed that the existing regulatory architecture is largely designed around major banks accustomed to navigating heavy compliance demands—a significant barrier for newer entrants.

Still, Lewis expressed confidence in the evolving regulatory outlook: “We now have clear support from regulators who want to encourage innovation in this space.”

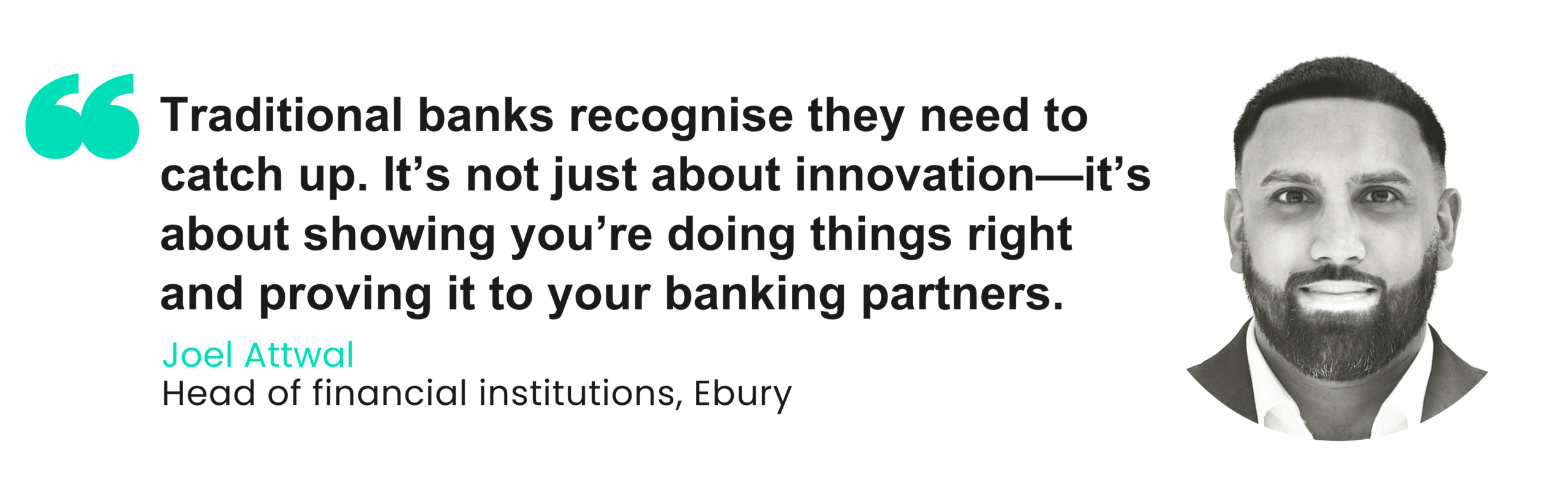

The evolving cross-border payments ecosystem is less about competition between banks and fintechs, and more about strategic collaboration. Joel Attwal, head of financial institutions and correspondent banking at Ebury, described this shift as a “dual transformation”, where fintechs contribute agility and customer-focused innovation, while banks offer the scale, liquidity, and regulatory credibility that underpin global payments. “There’s a recognition from traditional banks that they need to catch up,” he said, pointing to initiatives like Deutsche Bank’s DBX as signs of meaningful progress.

As de-risking continues to reshape correspondent banking, large institutions are reassessing their partnerships and increasingly turning to fintechs and regtechs to extend their reach. These newer players bring advanced tools, improved data flows, and a readiness to serve jurisdictions that have historically been underserved. But they must also meet stringent requirements—robust transaction monitoring, sanctions screening, and strong governance are all critical. “It’s not just about innovation,” Attwal noted, “it’s about showing you’re doing things right, and proving it to your banking partners.”

The success of this emerging model depends on both sides raising the bar. Fintechs must invest in compliance infrastructure and transparency, while traditional banks must move beyond legacy systems and embrace next-generation technology. As Attwal put it, the most promising opportunities lie in “working smarter”, leveraging complementary strengths to deliver faster, safer, and more inclusive cross-border payment services.

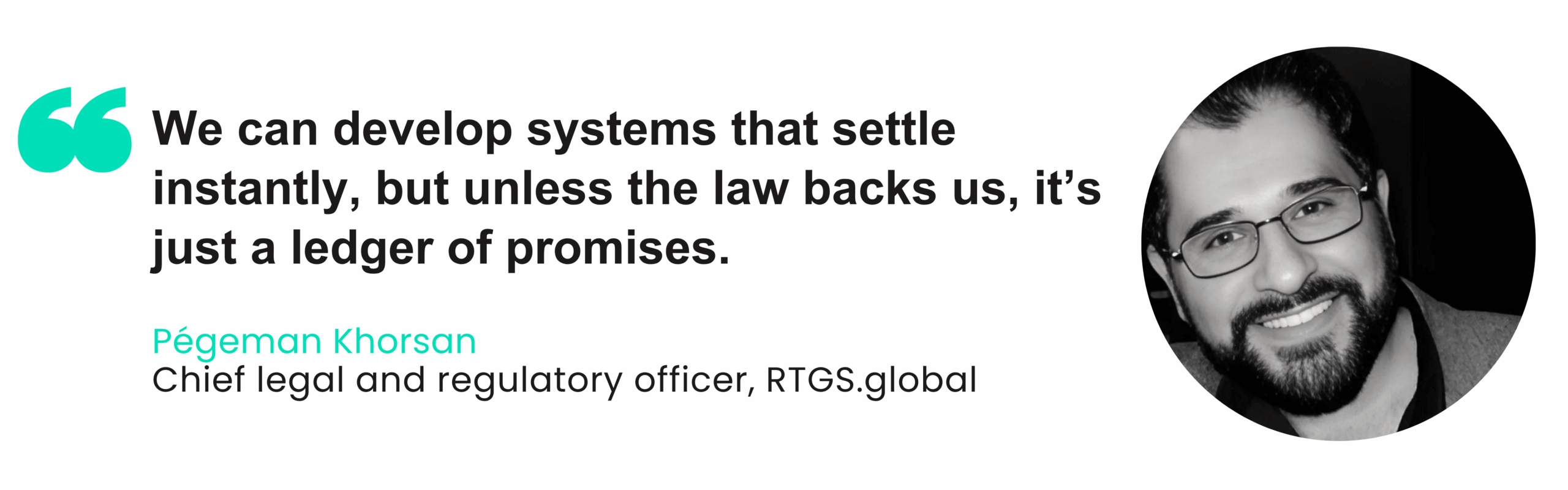

Despite rapid technological advancement, regulatory inertia continues to slow progress. “Everything is becoming faster—the technology is out there,” said Khorsan. “What we’re finding is that the regulatory landscape needs to catch up.” While digital infrastructure is advancing, including cloud-native solutions and distributed ledger technologies (DLT), legal frameworks are still rooted in outdated assumptions, creating friction in what should be frictionless systems.

This tension is particularly acute as traditional banks retreat from certain correspondent relationships, prompting fintechs to establish alternative networks. Yet as Khorsan pointed out, technological capabilities are not the limiting factor. “We can develop systems that settle instantly, but unless the law backs us, it’s just a ledger of promises.” In his view, the promise of instant, cross-border settlement is fundamentally limited by inconsistent legal recognition of digital transactions across jurisdictions. He called for a “re-centralisation of standards”—not to restrict innovation, but to provide a more stable legal foundation upon which decentralised systems can function.

However, not all panellists agreed with the feasibility of such harmonisation. Gary Palmer, CEO & founder of Payall, questioned whether the lack of legal alignment is the primary constraint. “It’s a folly to think we’ll get harmonisation across all jurisdictions,” he argued. “The real issue is automation and software, not the absence of liquidity or networks.” For Palmer, the focus should be on building smarter systems that can operate within existing constraints rather than waiting for global legal coherence that may never materialise. The debate underscored a central theme: while the tools to transform cross-border payments exist, regulatory and operational barriers—old and new—continue to define the pace of change.

The push toward instant cross-border settlement raises a fundamental question: can speed and safety truly coexist? While the industry is moving rapidly toward real-time capabilities, the panel warned that legal and operational safeguards have not kept pace.

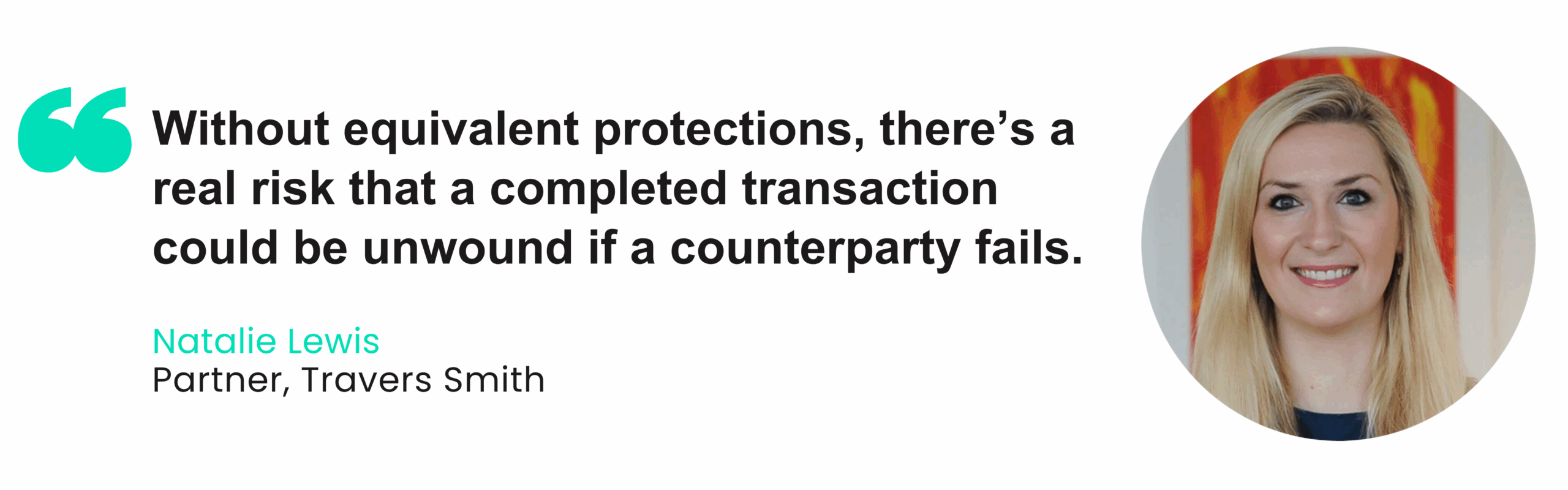

Lewis highlighted the legal grey areas surrounding settlement finality. In domestic systems, finality regulations provide clear protection in the event of insolvency. Cross-border payments, however, often fall outside these safeguards. “Without equivalent protections, there’s a real risk that a completed transaction could be unwound if a counterparty fails,” she warned—a risk amplified when payments are irrevocable and instantaneous.

Khorsan echoed the concern, underscoring the need for consistent legal frameworks across jurisdictions to prevent such reversals and reduce systemic exposure. But as Paul Palmer pointed out, safety in real-time payments isn’t just a legal question. “This isn’t only about speed—we need authenticated data, automated compliance, and shared responsibility for risk,” he said. The reality, he argued, is that achieving secure, real-time cross-border payments requires far more than faster pipes; it demands an integrated approach that spans law, technology, and institutional trust.

As regulatory expectations rise and payment ecosystems grow more complex, the industry is shifting from a model built on assumed trust to one grounded in real-time transparency. Both Palmer and Attwal emphasised the central role of intelligent compliance technologies in enabling this shift—not just as risk mitigators, but as enablers of sustainable cross-border growth.

Palmer described a new generation of compliance infrastructure that allows correspondent banks to observe, in real time, how their partners make decisions. This includes visibility into documentation, rule application, and risk assessments. “Trust is replaced with transparency,” he said. “No more audits six months after the fact.” By embedding this level of oversight directly into transaction flows, institutions can move away from retrospective compliance and toward continuous, automated assurance.

Attwal pointed to the expanding use of AI across the compliance lifecycle—from onboarding and customer due diligence to transaction monitoring and sanctions screening. These tools allow for a seamless flow of information across systems, making it easier to assess risk, calibrate thresholds, and respond to red flags proactively. “There’s now a full flow of information from onboarding through to payment execution,” he explained. For banks under pressure to maintain high compliance standards while scaling services, such transparency is not just a safeguard—it’s a competitive advantage.

As discussion turned to stablecoins and digital assets, panellists weighed their potential as a force for modernising cross-border payments—but also flagged the risks of adopting them without sufficient safeguards. Lewis acknowledged that stablecoins may address some of the core issues the industry faces. “One of the core use cases is addressing the speed and efficiency issues we’ve been discussing,” she said, noting that the UK’s draft regulatory framework for digital assets will likely accelerate experimentation and deployment in this space.

However, Palmer offered a more cautious view. While stablecoins might reduce friction and increase speed, he argued, many implementations do so by sidestepping the safeguards built into the traditional system. “A lot of stablecoin models solve a speed problem by not addressing the risk problem,” he said. In particular, Palmer warned that some projects are enabled by banking partners who fail to conduct proper due diligence on counterparties, creating blind spots that compromise systemic integrity.

Beyond questions of risk and oversight, there is a deeper structural tension between decentralised finance and the legal assumptions underpinning today’s financial markets. Lewis pointed out that settlement finality laws and financial market supervision frameworks were drafted with the premise of centralised operators—a premise that doesn’t hold in decentralised networks. “Of course that jars completely with all the libertarian views around exactly what this technology ought to be able to achieve,” she said. The result is a regulatory grey zone: laws intended to be technology-neutral in principle are, in practice, misaligned with how decentralised systems operate. Until that gap is resolved, stablecoins may remain more of a workaround than a true solution.

Cross-border payments are not evolving through technology alone—they are being reshaped by new forms of collaboration, regulatory shifts, and strategic rethinking. Legacy systems may be outdated, but they are not obsolete. With targeted innovation, greater transparency, and alignment between institutions, these systems can be rewired to meet the demands of a globalised, real-time economy.

As Attwal observed, the retreat of Tier 1 banks from certain corridors is creating space for fintechs, regtechs, and challenger institutions to step in. These emerging players bring agility and modern infrastructure, helping to connect underserved jurisdictions and foster financial inclusion on a global scale. The shift is not about replacement, but rebalancing—integrating the trust and liquidity of traditional institutions with the speed and intelligence of modern platforms.

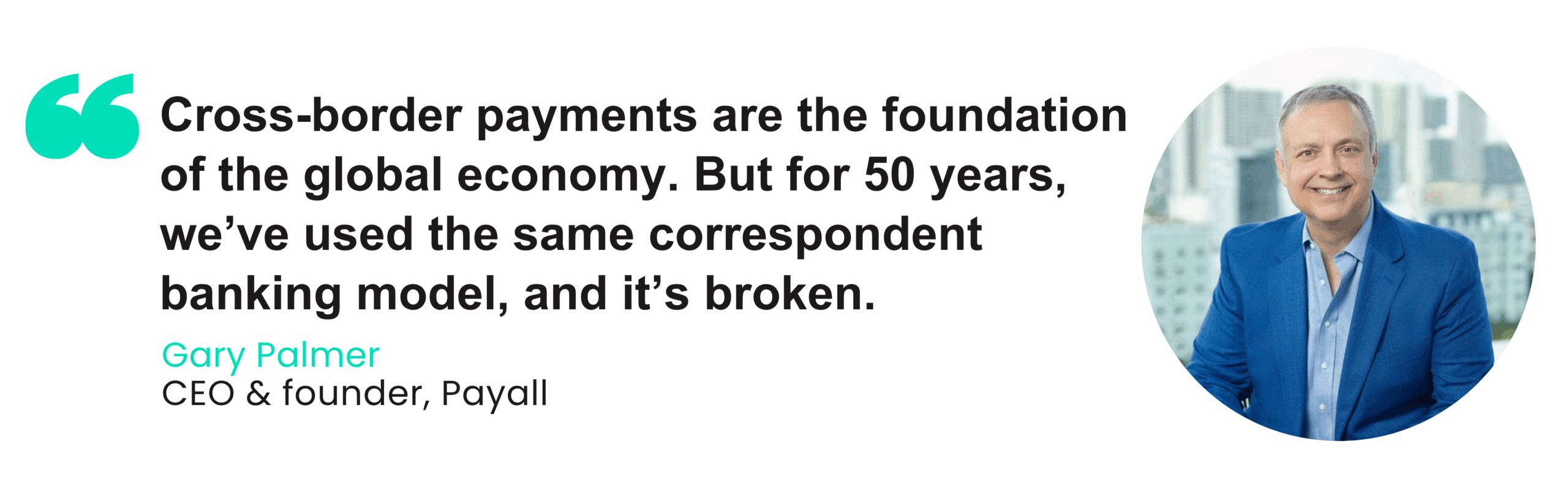

Paul Palmer made clear that the need for change is urgent: “Cross-border payments are the foundation of the global economy,” he said. “But for 50 years we’ve used the same correspondent banking model, and it’s broken.” For payment leaders, the message is clear. Incremental tweaks to legacy processes will not suffice. The path forward lies in purpose-built infrastructure, embedded compliance, and a new generation of partnerships. Those who embrace this shift—and help shape the standards that support it—will define the future of global payments.

A 2025 survey of UK retailers reveals how payment challenges and innovation priorities are shaping merchant strategies across the sector.

UK SME survey shows open banking intrigues merchants with faster, cheaper payments, but gaps in awareness and security fears slow adoption.

The Bank of England’s offline CBDC trials show it’s technically possible—but device limits, fraud risks, and policy gaps must still be solved.

The Payments Association

St Clement’s House

27 Clements Lane

London EC4N 7AE

© Copyright 2024 The Payments Association. All Rights Reserved. The Payments Association is the trading name of Emerging Payments Ventures Limited.

Emerging Ventures Limited t/a The Payments Association; Registered in England and Wales, Company Number 06672728; VAT no. 938829859; Registered office address St. Clement’s House, 27 Clements Lane, London, England, EC4N 7AE.

Log in to access complimentary passes or discounts and access exclusive content as part of your membership. An auto-login link will be sent directly to your email.

We use an auto-login link to ensure optimum security for your members hub. Simply enter your professional work e-mail address into the input area and you’ll receive a link to directly access your account.

Instead of using passwords, we e-mail you a link to log in to the site. This allows us to automatically verify you and apply member benefits based on your e-mail domain name.

Please click the button below which relates to the issue you’re having.

Sometimes our e-mails end up in spam. Make sure to check your spam folder for e-mails from The Payments Association

Most modern e-mail clients now separate e-mails into different tabs. For example, Outlook has an “Other” tab, and Gmail has tabs for different types of e-mails, such as promotional.

For security reasons the link will expire after 60 minutes. Try submitting the login form again and wait a few seconds for the e-mail to arrive.

The link will only work one time – once it’s been clicked, the link won’t log you in again. Instead, you’ll need to go back to the login screen and generate a new link.

Make sure you’re clicking the link on the most recent e-mail that’s been sent to you. We recommend deleting the e-mail once you’ve clicked the link.

Some security systems will automatically click on links in e-mails to check for phishing, malware, viruses and other malicious threats. If these have been clicked, it won’t work when you try to click on the link.

For security reasons, e-mail address changes can only be complete by your Member Engagement Manager. Please contact the team directly for further help.