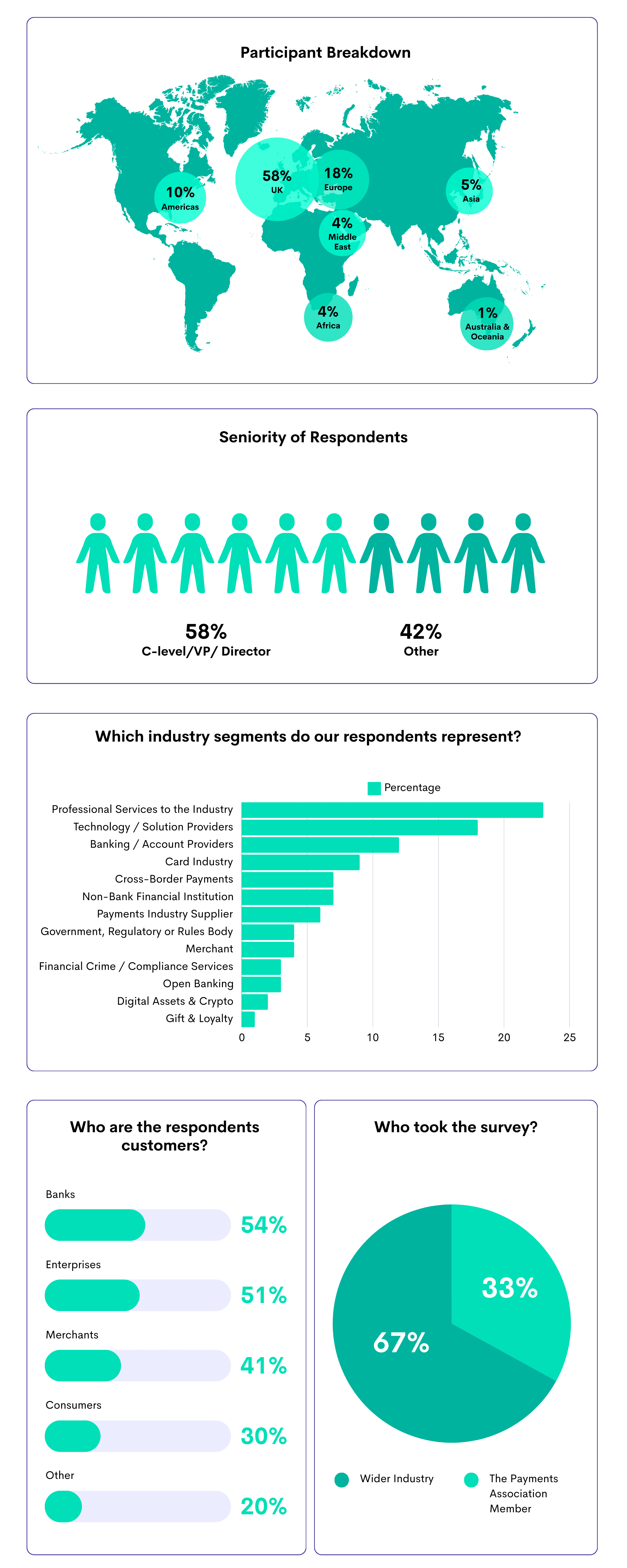

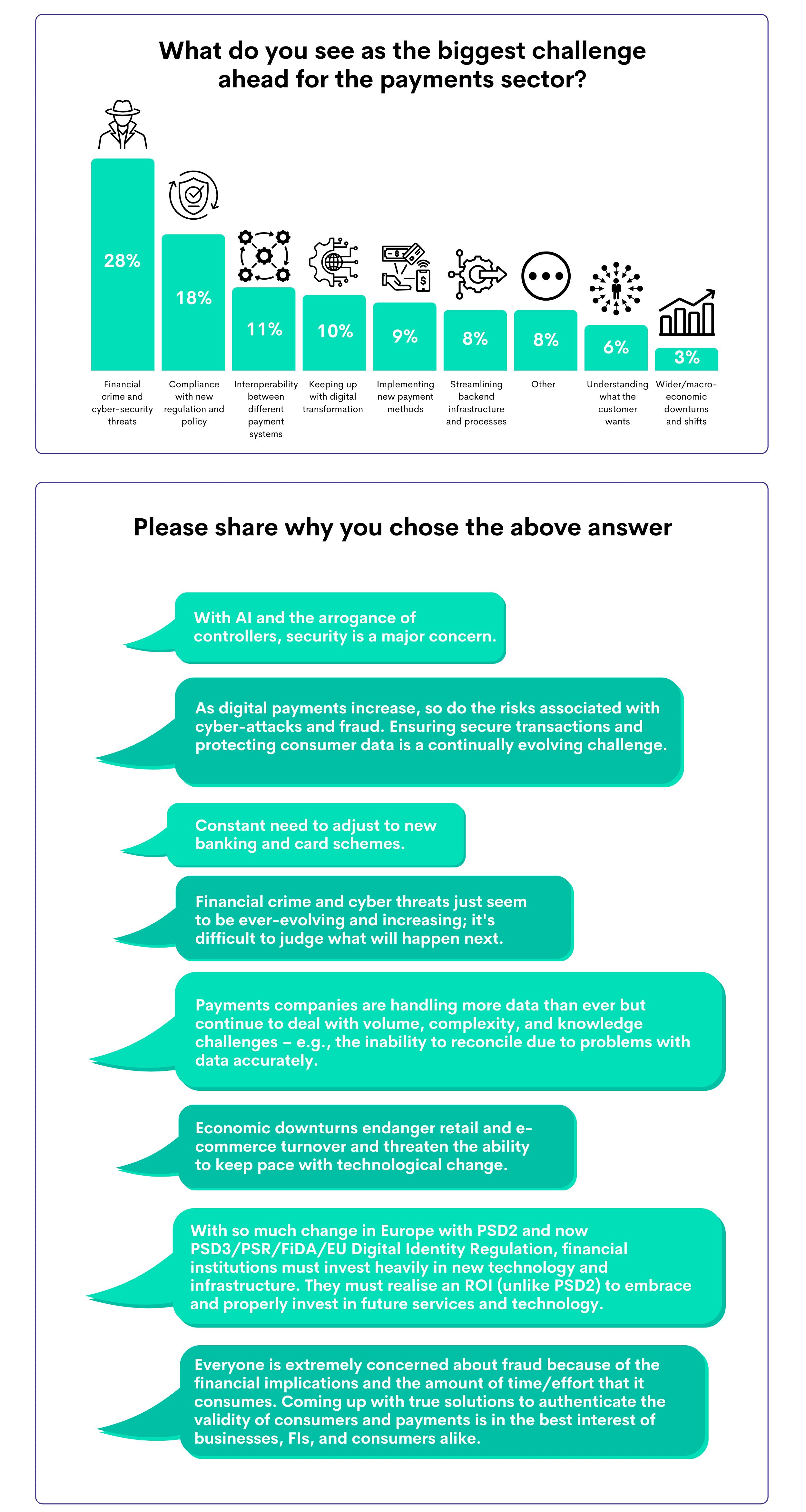

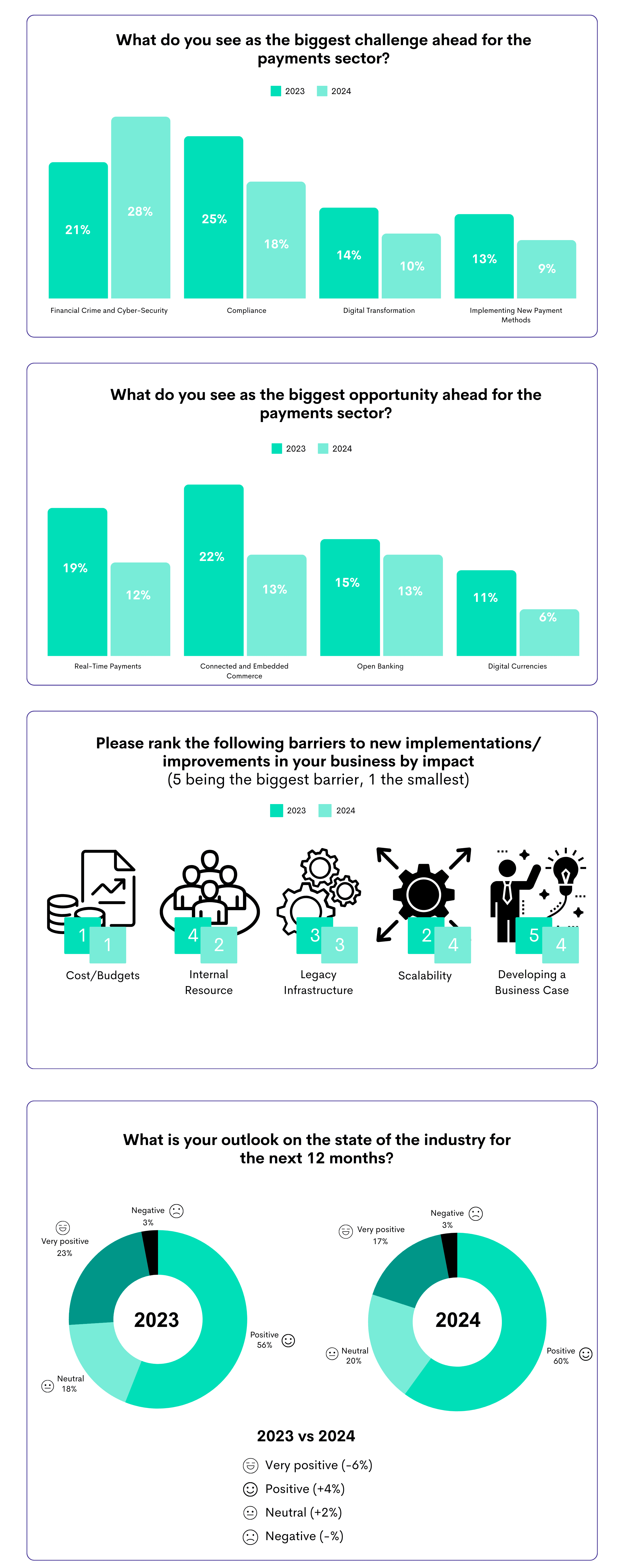

Regarding industry breakdown, 12% of respondents came from Banking and Account Providers, 23% from Professional Services, and 18% from Technology/Solution Providers. The survey results show that financial crime and cyber-security threats are the industry’s most significant challenges, with 28% of respondents highlighting this issue. Compliance with new regulations remains a critical concern for 18%, while 11% see the need for better interoperability between different payment systems as a pressing challenge.

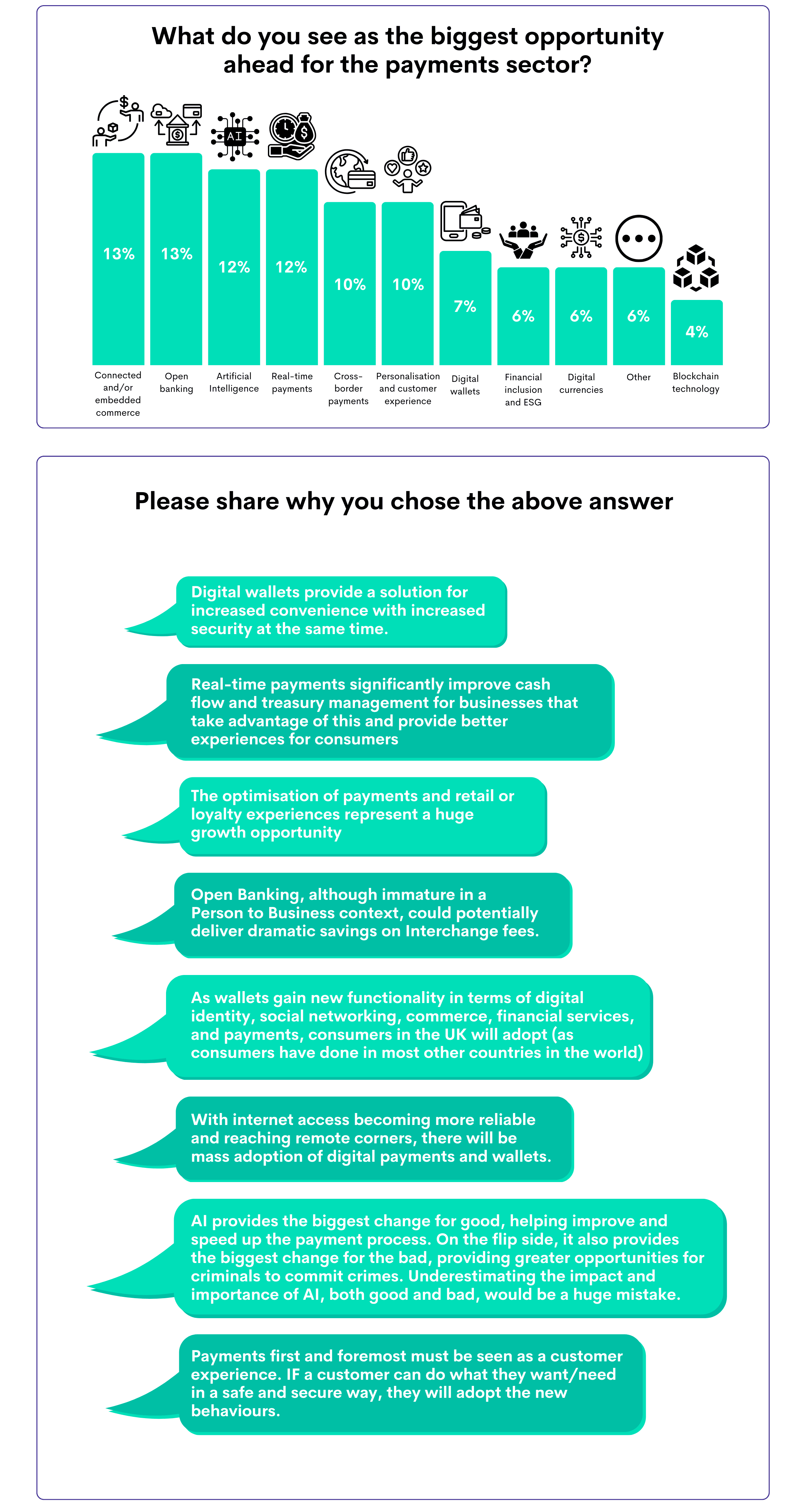

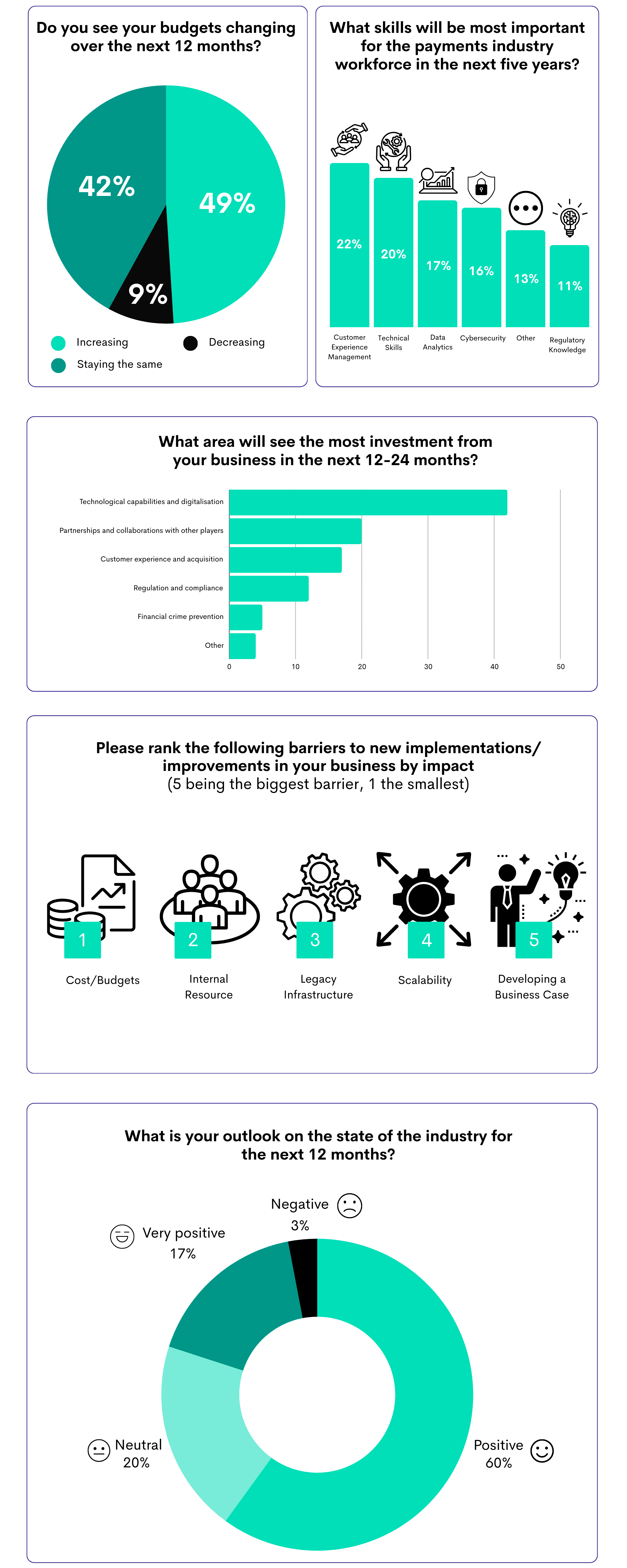

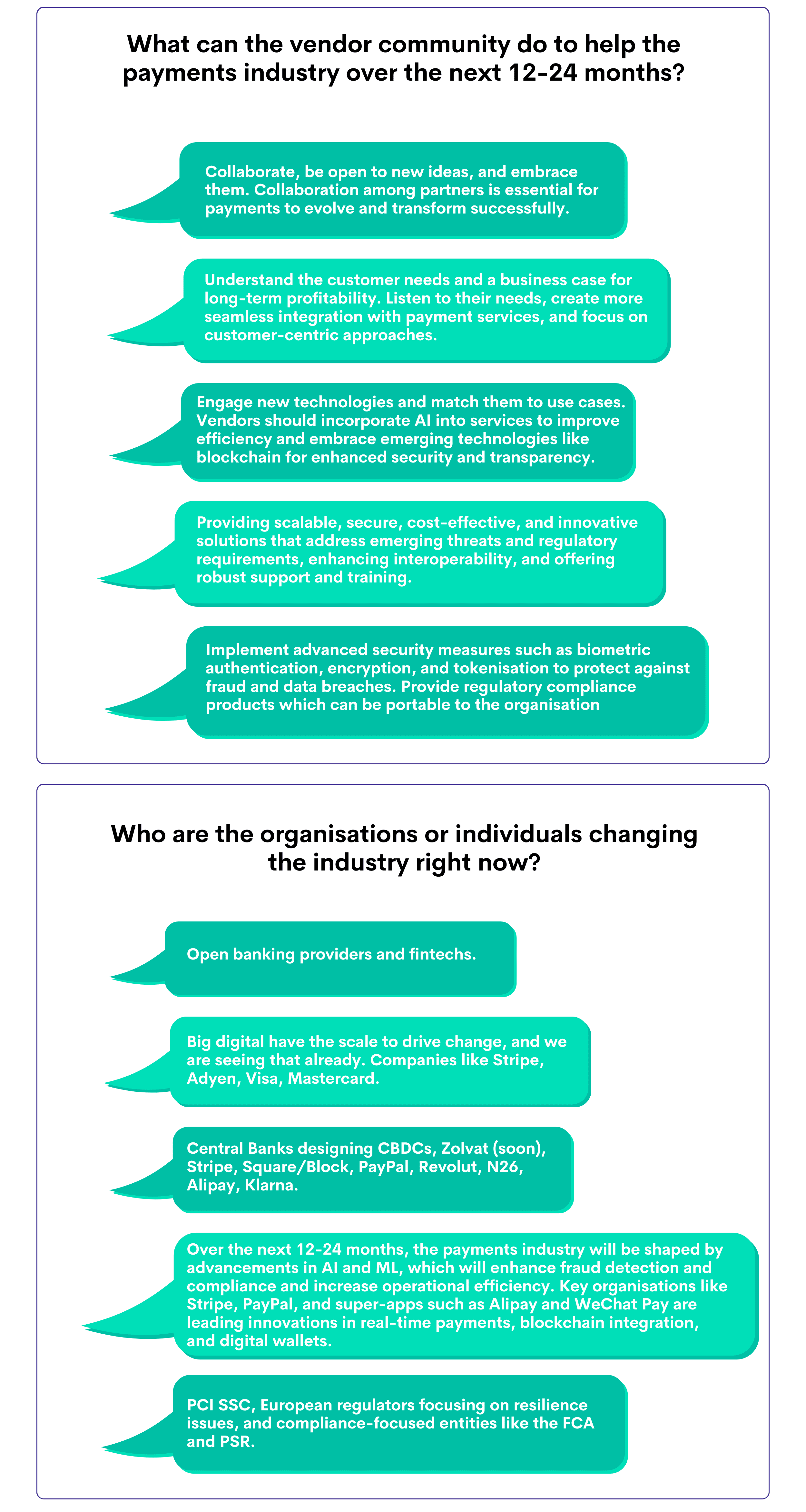

The survey also highlights opportunities in the sector, with 13% of respondents identifying connected and embedded commerce as a significant area of growth, followed closely by open banking and AI, each noted by 13% and 12%, respectively. When considering the skills needed for the future, 22% of respondents emphasized the importance of customer experience management, while 20% highlighted technical skills, and 17% pointed to data analytics.

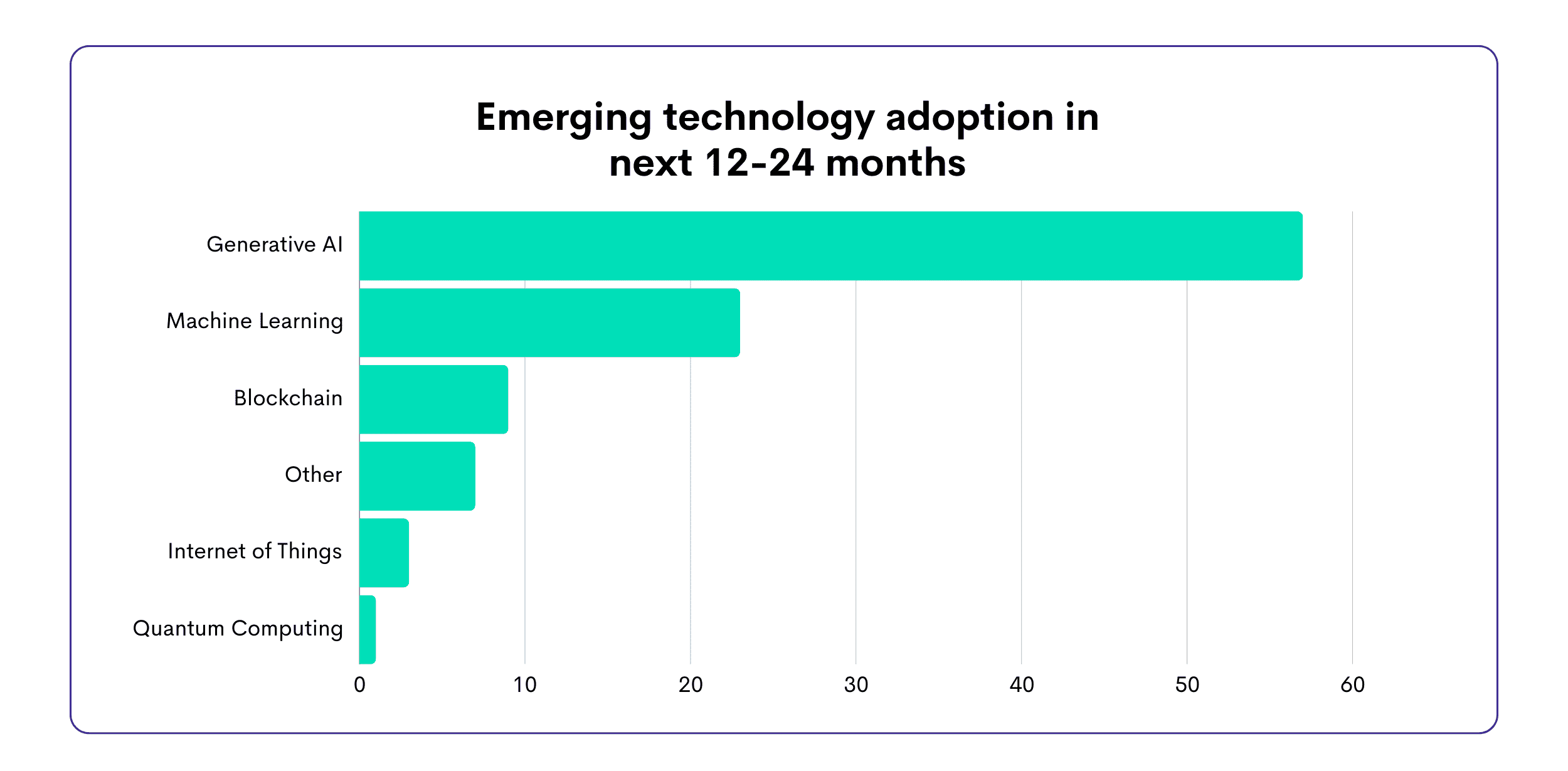

Budgetary trends are positive, with 49% of respondents indicating an increase in their budgets over the next 12 months. This suggests a continued investment in areas such as technological capabilities and digitalisation. In terms of emerging technologies, generative AI and machine learning are anticipated to be widely adopted, with 51% and 19% of respondents, respectively, planning to integrate these technologies into their operations. Despite these advancements, the overall outlook for the industry is predominantly positive, with 60% of respondents expressing optimism, while 20% remain neutral and a minimal 3% expressing a negative outlook.