Embedded finance and multi-banking give corporates greater control, new revenue streams, and stronger networks, unlocking value beyond traditional banking.

In today’s rapidly evolving financial landscape, disintermediation of finance, where financial services are embedded directly into non-financial platforms, presents a unique opportunity for corporates to own a bigger share of value and gain control over the financial relationships with their customers to satisfy needs within their merchant networks.

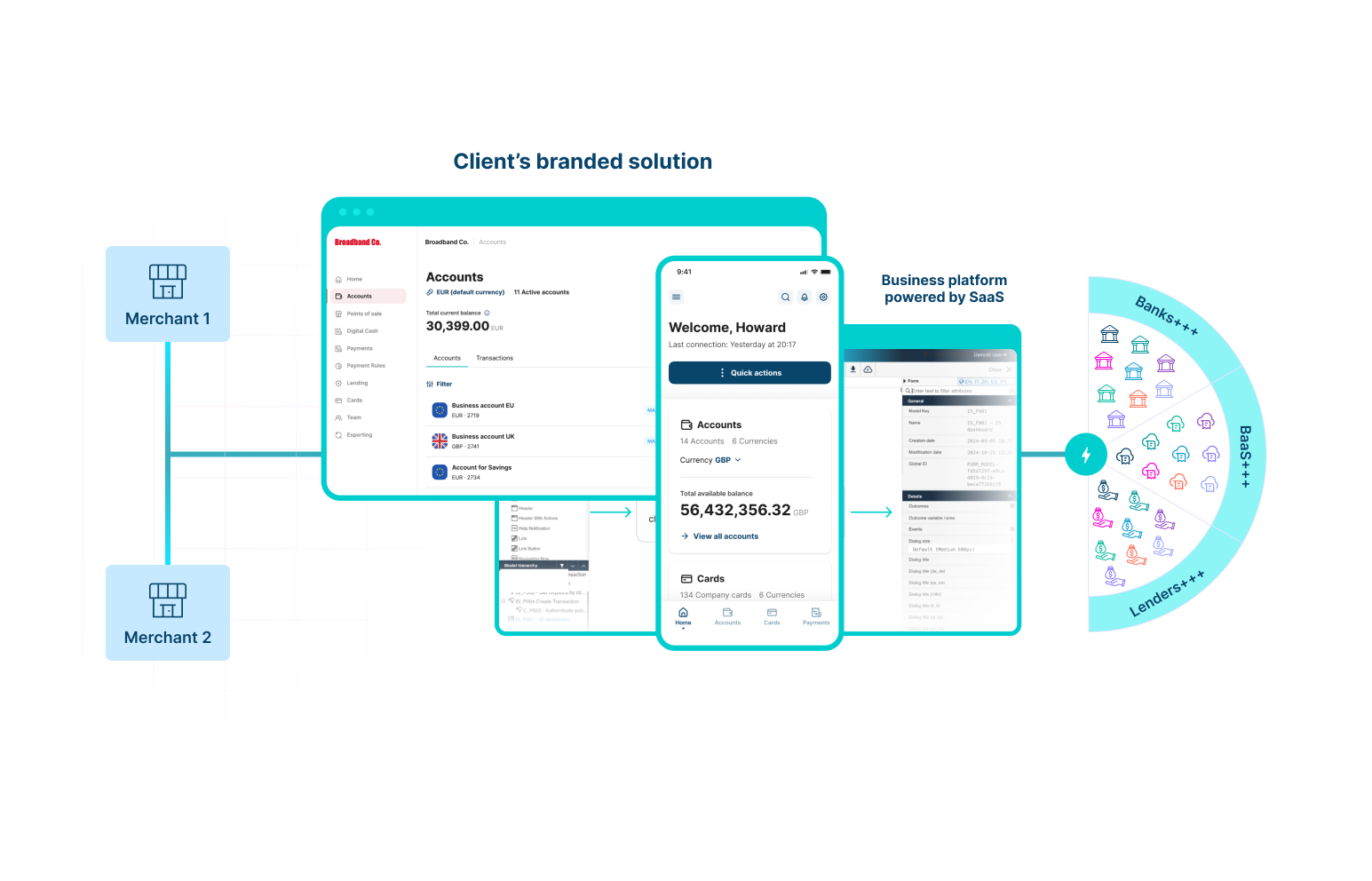

Relying on a single provider can limit flexibility and expose businesses to unnecessary risks, such as service disruptions or unfavourable terms. Multibanking, (which is access to best of breed financial services among use cases and locations) can empower corporates to take full advantage of this opportunity.

Corporates can boost their relevance, drive demand, and strengthen customer loyalty by strategically partnering with financial service providers that align with their needs and those of their merchants. By integrating these financial solutions into their existing offerings, companies can enhance their overall value proposition, making it more attractive and “stickier” to customers, thereby increasing retention and long-term engagement. Furthermore, they can spread these services across multiple providers to lower transaction costs.

This shift not only enables a more streamlined flow of capital but also drives growth, control, and revenue within the network.

Corporates often rely on third-party financial institutions such as banks, fintechs, and intermediaries to provide payments, financing, and other financial services within their distribution networks. Traditionally, these financial partners are introduced directly to the merchant network, resulting in individual relationships between each financial institution and merchant. However, this approach presents several challenges. It weakens the connection between merchants and the corporate value proposition, reducing loyalty and retention. Additionally, it leads to fragmented service experiences, increased costs, and a lack of transparency in the transactions that are crucial to the corporate’s operations.

By embedding financial services directly into their propositions, corporates can now:

The beverage industry, like many others, is facing a shift. Breweries, distributors, and suppliers are grappling with more than just supply chain complexities; they’re also dealing with customer loyalty fatigue. Branded products, once seen as the ultimate driver of customer loyalty and revenue, are no longer enough. Consumers are looking for more than a label; they expect simple, tailored experiences that make their lives easier.

Take, for example, the challenges bars in Europe faced during peak seasons. Cash flow pressures often prevent them from stocking up and meeting demand. Traditional financial institutions are too slow and rigid to offer necessary or innovative solutions. But now, thanks to embedded finance technology, non-financial platforms such as distributors and breweries can offer financing solutions directly, empowering merchants to manage cash flow in real-time.

A recent example from the FMCG sector shows how embedding digital banking products like payment solutions and financing directly into their e-commerce platform helped a company go beyond selling products. By offering financing options linked to merchant payment terms, they strengthened partnerships across geographies and created a seamless experience that built trust and loyalty. Merchants could access the funds they needed quickly and easily without waiting for a bank to approve traditional loans.

This shift allows businesses to directly serve the financial needs of their merchant partners while sidestepping the traditional banking intermediaries. For breweries and distributors, this means offering more than just products; it’s about providing real, tangible value that helps merchants sell better, manage cash flow, and build stronger, more sustainable partnerships.

In today’s market, many traditional providers fail to meet the full spectrum of industry demands. Their offerings are often too narrow to provide comprehensive, end-to-end solutions, forcing businesses to juggle multiple providers and systems and creating unnecessary complexity.

A multi-bank approach eliminates this fragmentation by enabling access to various financial institutions within a single ecosystem. This disintermediation allows businesses to select and bundle the best solutions, improving flexibility and operational control.

The advantages of leveraging the multi-bank approach are clear:

The disintermediation of finance through embedded solutions represents a powerful shift for corporates. By integrating financial services directly into their market propositions, businesses can capture a larger share of the revenue, strengthen financial relationships, and create more efficient, growth-oriented networks.