What is this article about?

The potential benefits of programmable money, such as automation and efficiency, along with its ethical concerns, including privacy, data security, and misuse by central banks.

Why is it important?

Programmable money could transform digital finance by offering significant advantages, but addressing its ethical implications is crucial for ensuring public trust and effective implementation.

What’s next?

Developing robust regulations and consumer protection measures to balance the benefits of programmable money with its ethical challenges, ensuring privacy and preventing misuse.

Digital money is on the rise, whether consumers like it or not. However, despite an influx of new technology and infrastructure being introduced and teased, it hasn’t quite hit the mainstream yet.

The impending gold rush towards digital money hinges on new products and services providing use for consumers and businesses alike. This pendulum swing could be pushed by the widespread adoption of programmable money. Programmable money offers new opportunities to provide benefits to users, drive adoption, and deliver cost savings to companies.

Programmable money holds massive potential for transforming the future of digital money. Programmability enables various functionalities such as automated payments, conditional transactions, and smart contracts, all of which can be executed without the need for intermediaries. In essence, programmable money allows for the automation of financial processes and the creation of self-executing agreements, enhancing efficiency, transparency, and security in digital transactions.

According to Sidley Austin partner Max Savoie, programmability “cuts out” a lot of the processes, which can ultimately decrease the risks involved for all parties. He says: “For example, the process of dealing with authorisation and payment transactions can be complex, time-consuming, and risky due to potential issues with messaging transfer and data security. This can lead to delays, errors, and in some cases even non-payment by the party responsible.”

For all the positive aspects of programmable money, the ethics of using such variations of digital currency are in question, however.

The role of smart contracts and their use

Smart contracts are described by Savoie as providing a mechanism for conditions and authorisation to be “baked in” upfront, providing more certainty that payments will be made when predetermined conditions are met. While this can certainly be positive, it depends on what’s written into the smart contract and what the parties agree to treat as a “single source of truth” for determining whether and when relevant conditions are met, he adds.

A smart contract is a self-executing contract where the terms of the agreement between parties are directly written into code. This code is stored and replicated across a decentralised blockchain network, automatically enforcing and executing the terms of the contract when predefined conditions are met.

Essentially, it’s a computer protocol intended to digitally facilitate, verify, or enforce the negotiation or performance of a contract, eliminating the need for intermediaries and providing transparency, security, and efficiency in various transactions, particularly in blockchain-based systems.Top of FormBottom of Form

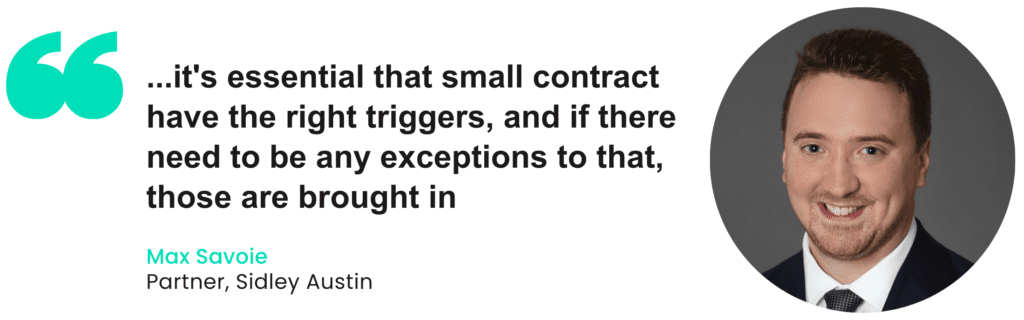

On the difficulties of this, Savoie says: “Where it gets a bit tricky is a smart contract is only as good as what you put into it. So, to have that certainty, it’s essential that that small contract has the right triggers, and if there need to be any exceptions to that, those are brought in.

How to create a smart contract |

|---|

1. Parties have to agree on the terms and conditions that they want to see implemented. |

2. These terms and conditions are translated into programming language in order to create a smart contract, covering rules and consequences if these rules are followed or not followed. A badly designed smart contract can pose major risks. |

3. The smart contract needs to be deployed by broadcasting it on the blockchain. Once this ‘transaction’ has been confirmed, the smart contract is live. |

4. If the terms and conditions in the smart contract are met, these are automatically verified. |

5. The smart contract is then executed. |

6. The execution is recorded on the blockchain. |

The temptation of central banks: Embedding monetary policy in currency and its problems

The allure for central banks to issue programmable Central Bank Digital Currencies (CBDCs) to integrate monetary policy decisions directly is one of the primary ethical concerns that must be considered.

According to the Payments Association’s whitepaper, “Coding Cash: Explore the Horizon of Programmable Money and Payments”, a central bank could issue programmable central bank digital currency (CBDC) to embed monetary policy decisions directly into the money itself.

Given that CBDCs are exposed to interest rate changes, any increase from a central bank will be reflected in the currency. Some have argued that negative interest rates could be passed onto the population if the CBDC is programmable.

Aside from being unethical in principle, it’s also untested. If central banks introduce a central bank digital currency (CBDC) while physical cash is still in circulation, people may begin to hoard cash.

Similarly, if CBDCs were designed with an expiration date to incentivize spending, individuals may opt to use physical cash or commercial bank money instead, potentially rendering such a policy approach ineffective.

Another potential use case of programmable money is in the welfare sector. Programmability in the context of welfare payments could ensure that funds are used in their prescribed way, maximising the use of benefits for those in need.

While it may seem logical to restrict welfare spending to certain categories like food, imposing such restrictions directly into the currency could be seen as overly intrusive and ethically questionable. It also raises questions about the balance between government oversight and individual autonomy.

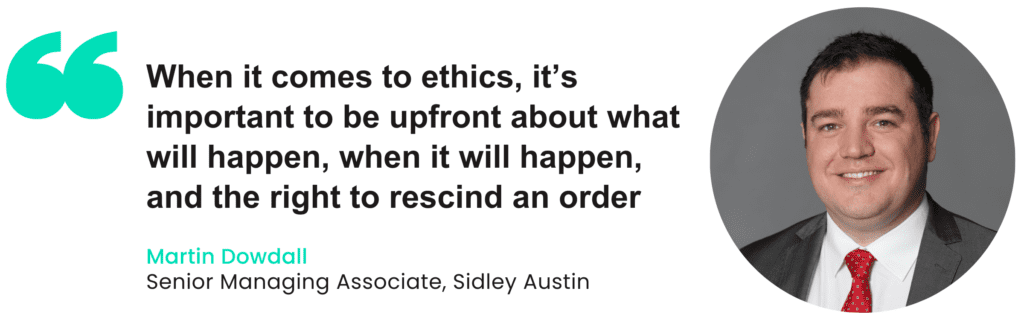

Savoie’s colleague Martin Dowdall believes this must be taken into account. Dowdall says more work must be done to examine the irreversible nature of programmable money.

Senior managing associate Dowdall says: “When it comes to ethics, it’s important to be upfront about what will happen, when it will happen, and the right to rescind an order in the future, as circumstances can change. Balancing the need for certainty with the recognition that things can change is a big challenge.

“For example, in a lending context, automatic payments may pose problems if unexpected financial difficulties arise. Additionally, it’s important to consider where the money will be held and whether third parties can control accounts. These factors are crucial in ensuring that funds are available when needed.”

Savoie also noted the need to consider data privacy. He stated: “If the program connected to the money is collecting information about me, such as my spending habits, behaviour, location, ethnicity, and job, it could potentially lead to misuse of data or unfair and discriminatory decision-making based on that data.”

Ensuring a level playing field

The general principle of payment regulation in both the EU and the UK has been to apply the same regulations to similar risks. This means considering potential harms, mitigating risks, and ensuring consumer protection.

For example, when setting up a subscription payment, strong customer authentication is required, along with various notices and protections for the consumer. There’s usually a cooling-off period and the right to cancel.

According to Savoie, the idea is to apply similar principles to smart money transactions, ensuring that consumers and data are protected in the same way. This approach would level the playing field between traditional and smart money methods.

Financial crime 2026 pulse report

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Regulation Roadmap Q3

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Consumer behaviour 2026 report

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.