What is this article about?

The Payment Systems Regulator (PSR) outlining its strategic priorities for 2024 at the PAY360 conference

Why is it important?

It addresses governance and regulatory issues that impact innovation and competition within the UK’s payment systems

What’s next?

The PSR aims to foster collaboration and implement regulatory interventions to enhance innovation, governance, and consumer protection in the payments industry.

At this year’s PAY360 conference hosted by the Payments Association, Payment Systems Regulator (PSR), led by Managing Director Chris Hemsley, is setting its sights on key priorities for 2024 and beyond. In his address at the conference, Hemsley outlined the regulator’s strategic vision, emphasising the imperative of learning from the past to shape a resilient and innovative payments ecosystem for the future.

Enhancing governance for agility and innovation

A cornerstone of the PSR’s agenda is enhancing governance within payment schemes to foster agility and innovation. Drawing from historical insights, regulatory bottlenecks that may impede progress need to be addressed.

The Cruickshank report in 2000 claimed that the governance of UK payment schemes restricted their ability to innovate in several ways. In the past, established players who managed schemes often hesitated to modify their infrastructure to facilitate new entrants or customers.

This unwillingness, Hemsley says, resulted in a significant barrier to innovation and progress. Moreover, mutual governance could be a time-consuming and complicated, as many schemes were traditionally only as efficient as their least productive member.

According to Hemsley, although payment systems have been modernised significantly, governance issues still need to be addressed. Questions still surround whether the concerns raised by Cruickshank have been resolved and whether the industry has moved towards a model that supports innovation.

In addition, it’s important to question whether the industry is in a position to quickly implement new technology and adapt rules for the benefit of all stakeholders, even if it goes against the interests of some participants. “In short, the answer is no,” he says.

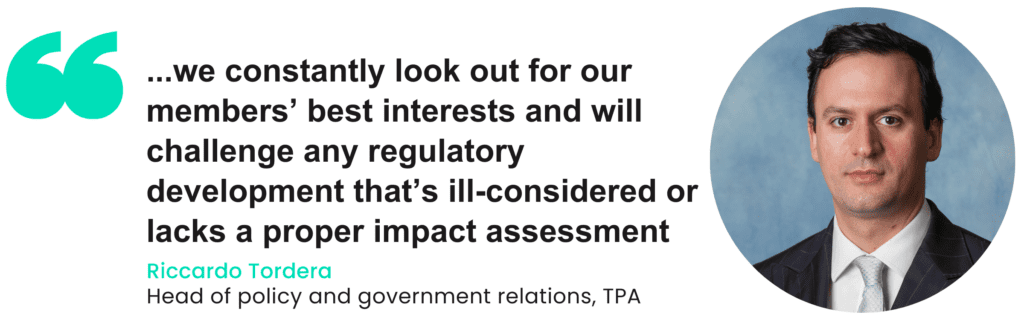

The Payments Association’s Head of Policy and Government Relations, Riccardo Tordera, says that whilst the UK continues to lead the world in FinTech investment and growth, increasingly assertive regulation is never far away. “This regulation is not always well thought out or fit for purpose,” he adds.

Tordera says: “At the Payments Association, we constantly look out for our members’ best interests, and we will challenge any regulatory development that is ill-considered or lacks a proper impact assessment.”

Importance in continuing to modernise

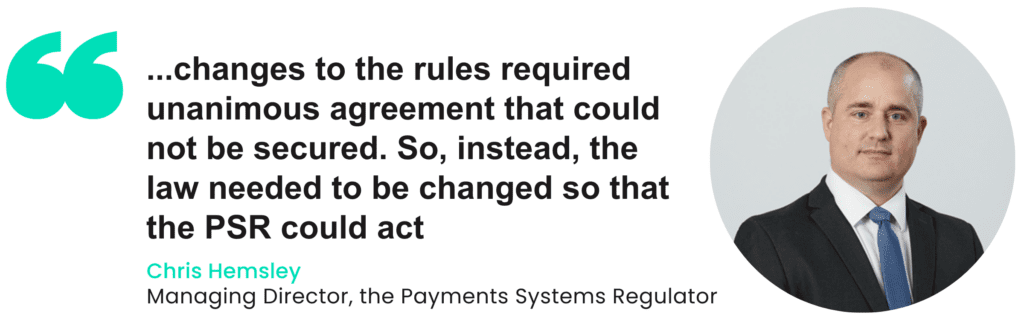

The PSR recognises the importance of streamlining decision-making processes to facilitate the swift adoption of new technologies and business models that benefit all stakeholders. Hemsley points out barriers to change, such as the need for unanimous agreement among industry participants, that have held back the UK’s progress in the past.

He says: “We can look at what happened when there were attempts to change the central rules to protect people from authorised push payment fraud. Despite considerable efforts, changes to the rules required unanimous agreement that could not be secured. So instead, the law needed to be changed so that the PSR could act.”

According to Lorraine Mouat, head of payment services at Thistle Initiatives, some challenges remain despite the governance structures facilitating a degree of innovation.

She says: “The ability of current governance frameworks to effectively facilitate innovation varies, with some areas demonstrating agility in adapting to change while others may lag behind.”

Focus on collaboration

Moving forward, the regulator is putting collaboration high on its list of priorities. By fostering a culture of collaboration and innovation, the PSR aims to empower payment schemes to respond effectively to emerging trends and consumer demands.

He says: “It is absolutely imperative that our payment system firms continue to modernise and change. And that the markets that they support continue to develop, promote competition and drive innovation.”

Moreover, mechanisms are being instigated to incentivise proactive governance practices prioritising consumer protection, market integrity, and fair competition.

Hemsley is keen on emphasising the importance of regulatory oversight in creating a framework for governance that balances innovation with risk management. As we move forward towards the second interim of the year, the PSR is actively seeking to collaborate with industry stakeholders to develop solutions that improve governance structures, encourage transparency, and reduce regulatory barriers to innovation.

Mouat believes there has been significant progress, particularly regarding the regulatory oversight championed by Hemsley, since the Cruickshank Report of 2000. However, she believes there is still work to be done to create a regulatory framework that fosters competition but does not disadvantage innovation.

Hemsley hopes that by promoting dialogue and collaboration, this regulatory environment that supports responsible experimentation and builds trust among consumers and businesses can be achieved.

As part of building a foundation of trust, he highlighted the importance of ensuring fair access for all market participants, including new entrants and smaller banks. Mouat claims that this has been on the agenda for years without being successfully implemented.

She explains: “Regulatory authorities, it was suggested, would need to take steps to ensure that payment systems are open and accessible, but 24 years later, we are still calling for regulatory interventions to address such barriers and facilitate the entry of new players into the market.”

On just how this could be achieved, she adds: “Ultimately, to achieve these goals, specific regulatory interventions are still necessary. This could include measures to enhance transparency further, promote interoperability, and prevent anti-competitive practices.”

FIS Global payments ecosystem strategy director Kevin Flood reiterates Mouat’s claims, expressing concern over the lack of innovation and stagnation in the UK payments industry since the Cruickshank report in 2000.

He tells Payments Intelligence that while the report called for interventions to make payment systems more open and accessible 24 years ago, “We’re still calling for them; now is the time to accelerate change given the access to technology and opportunity we now have .”

Fostering Innovation in open banking

Looking ahead, Hemsley has outlined the regulator’s commitment to fostering innovation in open banking. Central to this effort is the expansion of variable recurring payments (VRPs), which hold the potential to revolutionise subscription-based services and recurring transactions.

He says: “Markets and competition are powerful forces that we rely on to deliver innovation. But markets are institutions. They depend on agreeing on the rules of the game. And effective rules are needed to provide fair competition and to unlock investment and innovation.”

Hemsley believes that there needs to be coordination between market participants in order to achieve this, especially “where there are powerful incumbents” and where rules need to take into account future participants

This is what the PSR seeks to do regarding open banking, and discussions are being held between the strategic working group and the more recent VRP working group. He mentions that while widespread appetite exists to expand VRPs, there are important areas where targeted regulatory action might improve success.

Initial proposal feedback is required from some who feel that we are proposing to intervene too much, notably on requiring participation and controlling some prices.

He also touched on proposals to require participation and control of some prices in open banking payments and how views on the proposals varied in the consultation.

Placing VRPs offers consumers greater flexibility and control over their finances while enabling businesses to offer tailored services that meet evolving consumer preferences.

To support the growth of VRPs, the PSR is exploring targeted regulatory interventions to create commercially sustainable models that incentivise innovation while ensuring fair competition and consumer protection. This includes initiatives to address interoperability challenges, establish dispute resolution mechanisms, and promote data security standards within the open banking ecosystem.

According to Mouat: “To foster a commercially sustainable market for open banking payments, collaboration between regulators and industry stakeholders is crucial. Regulatory clarity, standardisation of APIs, and measures to address data privacy and security concerns are essential for building trust and encouraging innovation.”

The PSR recognises the importance of industry collaboration in driving innovation in open banking. By engaging with banks, fintech, consumer groups, and other stakeholders, the PSR seeks to identify barriers to innovation and co-create solutions that promote market development and consumer welfare. Moreover, the PSR is committed to monitoring market dynamics and adapting regulatory frameworks to support the evolution of open banking while safeguarding consumer interests.

Promoting collaboration and regulatory compliance

Hemsley emphasised the importance of collaboration between industry stakeholders and regulatory bodies in navigating the complexities of the payments landscape. By drawing parallels with successful regulatory approaches in other sectors, such as telecoms, the PSR seeks to leverage targeted regulation to unlock competitive markets and drive positive outcomes for businesses and consumers alike. With a clear emphasis on promoting regulatory compliance, the PSR aims to foster a culture of accountability and transparency within the payments industry.

Tordera believes that the strategy posed by the regulator may be problematic, especially for the fintech sector. He says: “It appears the PSR’s current strategy may pose significant challenges to the UK payments industry, risking the success of many innovative businesses,”

“This is when a reset of the timings would give the industry and Faster Payment Service (FPS) time to build and bring in properly tested systems and controls that would create a far more sustainable solution and help to protect UK fintechs from the turbulent waters ahead of them.”

The PSR recognises that effective regulation requires collaboration between regulators, industry stakeholders, and consumer groups. By engaging in constructive dialogue and information sharing, the PSR seeks to enhance regulatory effectiveness, promote industry best practices, and address emerging risks and challenges. Moreover, the PSR is committed to facilitating industry compliance through guidance, education, and enforcement actions where necessary.

In conclusion, the PSR’s priorities for 2024 and beyond underscore its commitment to fostering innovation, promoting competition, and ensuring consumer protection within the payments landscape. With a clear strategic vision and proactive approach to regulatory oversight, the PSR is poised to navigate the complexities of the digital era and shape a resilient and innovative payments ecosystem for the future. As industry stakeholders collaborate and engage with the PSR, they can expect a dynamic and responsive regulatory environment that supports growth, innovation, and prosperity within the UK payments industry.

Read more Payments Intelligence

Regulation Roadmap Q3

TPA’s Q3 UK Payments Regulation Roadmap explains the key UK and international regulatory developments affecting payment firms over the coming years.

Consumer behaviour 2026 report

New research uncovers the payment habits, preferences and priorities shaping the future of payments in the UK.

How AI-powered banking tools are failing vulnerable customers

New research shows vulnerable customers are strong adopters of AI and digital banking, but are far more likely to experience failed payment journeys and poorer outcomes.