His Majesty’s Treasury is developing a vision and strategy for UK payments. This could herald a period of leadership of payments by the Government – if the ingredients are right.

Once, the UK was seen to lead the world in payments. Even without clear leadership from the Government, the industry, institutions, and regulators charted a path towards a world where payments continued to work better for everyone. However, in recent years, this approach has stopped working. While not great in number, the initiatives currently need co-ordination, leading to difficulties in aligning the regulation towards the common goal of being a world-leading jurisdiction.

There are now too many uncoordinated initiatives, with poorly aligned regulations and insufficient collaboration towards making the industry better and being a world-leading jurisdiction from which to set up and run a payments business.

Against this backdrop, the UK’s Chancellor, Jeremy Hunt, visited India. There, a digital ID and universal payments infrastructure has been rolled out for most of the country’s 1.2bn population since it was piloted in 2016. Folklore has it that the Chancellor made a payment while shopping using a QR code, and this made him ask, ‘Is the UK’s payments industry falling behind’?

Upon returning to the UK, Hunt commissioned Joe Garner, a seasoned financial services leader and ex-CEO of Nationwide, to find the answer. In his Mansion House speech in July, the Chancellor announced that the Future of Payments Review would be undertaken over the summer, and the report was featured in his Autumn Statement in November.

The Future of Payments Review presented sound analysis and strong recommendations for change. But the two biggest recommendations were simple: firstly, payments is sufficiently important for the Government to have a National Payments Vision and Strategy (NPVS). And secondly, the NPVS had to be produced and owned by HM Treasury (HMT).

To help align the industry’s main stakeholders around this idea, The Payments Association (TPA) convened a breakfast at Mansion House in January 2023. It was attended by senior representatives from HMT, the Bank of England, Open Banking Ltd and the Centre for Finance, Innovation and Technology (CFIT), as well as the PSR and FCA, other trade associations, politicians and TPA members. The Lord Mayor of the City of London opened the discussion and invited guests to express their views about HMT’s work on NPVS.

What is the NPVS and what should be its aim?

TPA believes that the Treasury’s announcement of the NPVS marks a significant milestone in the UK’s efforts to modernise its payment systems and keep pace with the evolving needs of consumers and businesses. With the right ingredients, it should promote competition, innovation, and customer choice while ensuring the safety and reliability of payments.

TPA also believes that the NPVS must be designed to complement the Future of Payments Review findings, offering a comprehensive approach to reshaping the payments ecosystem. To realise its full potential, the NPVS must incorporate several elements: a visionary and upbeat forward from a senior government representative, a bold and clear vision statement and a roadmap to guide actionable outcomes.

The NPVS’s central objective must be to ensure that end-users of payment systems are prioritised and their needs met.

The Payments Association’s Director General, Tony Craddock, believes that a successful NPVS for the UK is characterised by a vision statement that is clear, easily understood, and memorable. “It should ambitiously reflect the government’s objectives, positioning the UK payments ecosystem as a leader on the global stage,” he said. This vision should be driven by a public-private partnership aiming to achieve significant user outcomes, including increased investment, job creation, improved status for the UK, and better consumer and business satisfaction.

Additionally, Craddock says, the NPVS should transform the payments ecosystem into one that is progressive, resilient, and innovative, underpinning an inclusive and diverse society. “It should enable trusted, secure, and accessible payments that benefit everyone, facilitating global transactions.”

The NPVS must also involve users and channel partners in innovation, licensed entities in collaboration, and technology specialists in working together towards a shared goal. Its regulators should balance policing with partnership, competition with innovation, and resilience with growth.

Inclusive engagement: Who's at the table?

The NPVS should include a comprehensive and inclusive template that brings together the entire payments ecosystem, including stakeholders beyond the payments industry, such as customers and consumer groups, regulators, merchants, big tech companies, licensed entities, trade associations, membership bodies, technology companies and advisors.

The NPVS’s central objective must be to ensure that end-users of payment systems are prioritised and their needs met. Outside the bank providers, three key stakeholders need to be engaged: regulators to maintain the integrity and efficiency of the system; merchants to ensure data integrity and participate in dispute management processing transactions; and Big Tech to take responsibility for information flowing through their systems in the flow of payments.

TPA believes the NPVS should have a broad scope and that various monetary form factors must be considered throughout the development process. These form factors include account-based domestic digital payments, cards, mobile wallets, cash, tokenised assets like Central Bank Digital Currencies (CBDCs) and stablecoins, as well as innovative credit products like Buy Now Pay Later (BNPL) and cross-border payments using digital currencies.

According to Neil Harris, chair of the Advisory Board at TPA, the NPVS should not list specific initiatives as their inclusion could become rapidly outdated and lead to subjective and contentious selections. However, an appendix or separate document could be created post-agreement of the NPVS to review and evaluate potential activities, initiatives, or programs. “This approach ensures the NPVS remains a guiding document rather than a detailed action plan,” he said. “It will be more effective and durable, and avoid short-term thinking and turf wars.”

Harris listed various initiatives for future consideration, including building next-generation payments infrastructure and the Retail Liability Network that is being developed by a task force at UK Finance. Programmes to attract and facilitate investment in technology companies and licensed payment firms through Venture Capital and Private Equity should also be considered.

A three-year roadmap, laying out the timeline and milestones for achieving the desired outcomes (not initiatives), should be an integral part of HMT’s NPVS, as should a series of next steps outlining the immediate actions to be taken following publication.

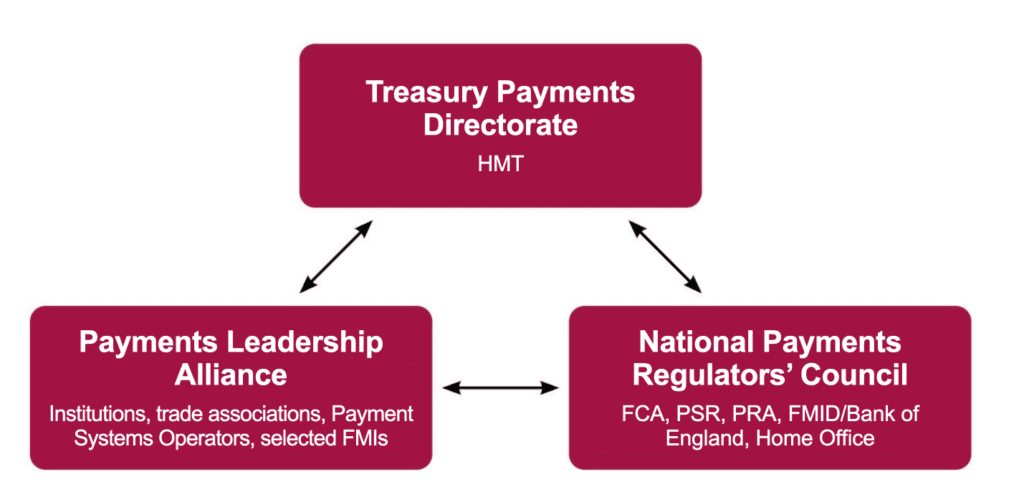

Governance of the NPVS

Governance is everything. TPA has drafted some initial ideas that reflect the importance of HMT in leading payments, making decisions and assessing performance, and an alliance across the industry that is involved with reviewing and prioritising initiatives, simplifying structures and making recommendations to HMT. These ideas also include a new group of regulators to focus on payments, listening to the concerns and priorities of the industry alliance in light of the principles defined by HMT.

Key principles

A framework of principles categorised into two levels should guide the implementation of the vision while also assessing its progress, suggests TPA. First-level principles should focus on enabling innovation that delivers beneficial outcomes for payment users, promoting an efficient payments ecosystem with fair commercial practices, and deploying modular API-enabled payment technologies suited to the problems at hand.

According to Craddock, these principles also “emphasise the importance of progressive governance that bolsters government leadership and ensures accountability, while utilising principles-based regulation where regulators work in tandem with the industry to achieve the vision.”

With courage and determination, the Government can show its leadership, knowing that it has the support of the whole ecosystem to implement it effectively.

Tony Craddock, The Payments Association’s director general

Second-level principles delve into specific areas of focus. For payments users, these include focusing on the needs of consumers and businesses for secure and safe payments, and providing choice and transparency while also reducing payment costs through competition and innovative services.

TPA advocates for intelligent and secure payment experiences to reduce fraud, appreciating the ongoing importance of cash for certain segments of the population and integrating payments into the education system. Competition should be used as a driver of positive change, ensuring fair value exchange among all stakeholders using suitable commercial models.

Timelines and moving forward

The NPVS is set to be a dynamic and evolving framework with specific timelines and processes for review and refinement. Publication of the NPVS is not currently set, but ideally, it would be presented a year after the Chancellor announced the Future of Payments Review at the Mansion House Speech in July 2024.

Beyond this initial launch, the NPVS is designed to be a living document, with updates scheduled every two years. These biennial reviews will assess the NPVS’ achievements against its success criteria, ensuring the vision remains relevant and effective in the rapidly changing payments landscape.

The community’s role

These initial ideas from TPA will likely evolve rapidly. But an industry rarely faces such a pivotal moment in its evolution. “With courage and determination, the Government can show its leadership, knowing that it has the support of the whole ecosystem to implement it effectively”, says Craddock. Perhaps Mansion House in the City of London will be where, as it has been for generations, the future of money is determined.