Merchant survey 2025: Navigating the payment innovation divide

A 2025 survey of UK retailers reveals how payment challenges and innovation priorities are shaping merchant strategies across the sector.

What is this article about?

The challenges and strategic priorities for CEOs in the payments industry over the next 12 months, focussing on technological advancements, fraud prevention, regulatory changes, and customer expectations.

Why is it important?

It highlights the critical trends and strategies necessary for companies to remain competitive and secure in the rapidly evolving payments landscape.

What’s next?

Companies will need to adapt to regulatory changes, leverage emerging technologies like AI and blockchain, and foster a culture of continuous innovation and collaboration to stay ahead.

As the payments industry undergoes rapid transformation driven by technological advancements and shifting consumer behaviours, CEOs face a landscape filled with both opportunities and challenges. On June 26, Payments Intelligence hosted an exclusive Payments Lab session where CEOs from member companies of The Payments Association convened to discuss their strategic priorities for the upcoming year.

The discussion spanned a range of critical topics, from the impact of technological advancements and fraud prevention to adapting payment solutions to meet changing customer expectations. The roundtable also delved into leadership strategies for inspiring innovation and forward-thinking within organisations.

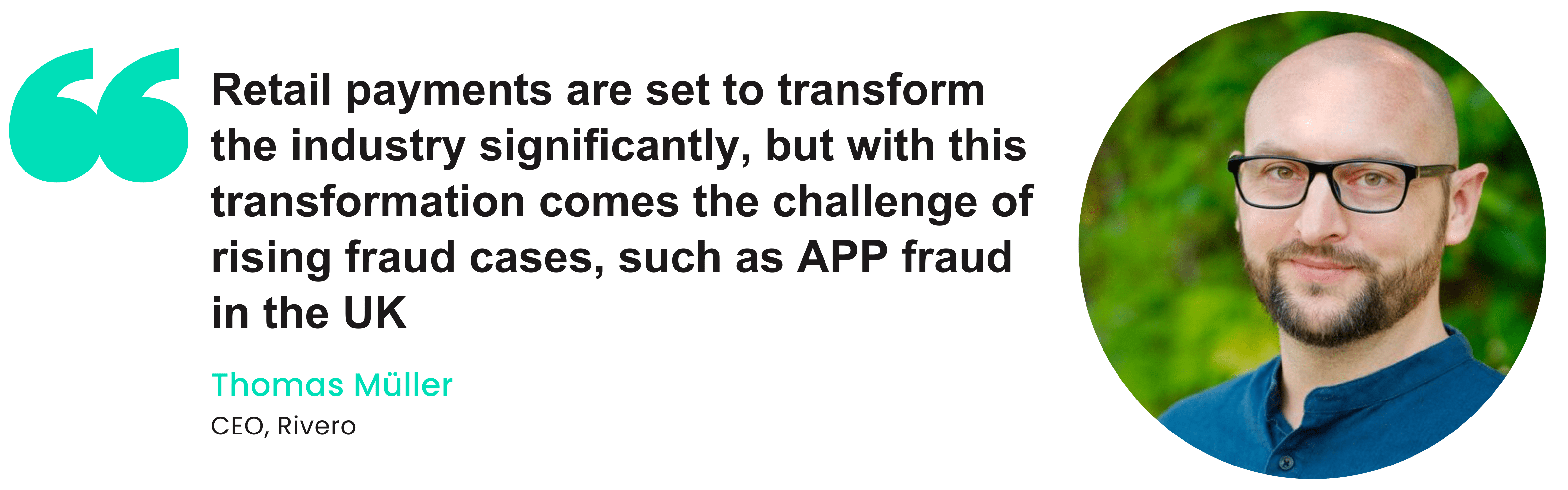

The roundtable discussion started with a focus on the emerging trends expected to shape the payments industry over the next year. Thomas Müller, CEO, Rivero, initiated the conversation by highlighting the increasing importance of retail payments and real-time payment systems. “Retail payments are set to transform the industry significantly,” he noted. “But with this transformation comes the challenge of rising fraud cases, such as APP fraud in the UK.”

This insight set the stage for a deeper examination of how these trends are interlinked with consumer behaviour and technological advancements. As Müller spoke, it became clear that the evolution of retail payments is not just about the technology itself but also about adapting to the changing expectations of consumers who demand faster and more secure transactions.

Sean Forward, UK CEO, payabl., jumped in, adding that the diversification of payment methods is another key trend. “Absolutely, Thomas. Consumers now expect a variety of payment options beyond traditional credit and debit cards,” he said. “This push for multiple payment mechanisms is enhancing the customer experience and opening new revenue streams for merchants.” Forward’s comment highlighted a crucial point: the competitive advantage for merchants now lies in their ability to offer seamless and diverse payment options, catering to a global customer base with varying preferences.

Alan Schweber, CEO, Lucra, underscored the importance of addressing fraud prevention amidst these changes. “Fraud, particularly in account-to-account payments, will remain a critical concern,” he stated. We need industry-wide collaboration and innovative solutions to combat these threats effectively.” Schweber’s perspective brought attention to the darker side of technological advancement—while new systems improve efficiency, they also create new vulnerabilities that must be addressed through collaborative and innovative efforts.

Given these trends, the panellists were asked how they see the regulatory landscape evolving, especially with the rise of digital currencies and stablecoins. This question steered the conversation towards the regulatory implications of these emerging trends, a critical aspect that often dictates the pace of innovation.

Forward responded, “The FCA’s steps towards regulating stablecoins are just the beginning. This regulatory framework will pave the way for broader adoption and integration of digital currencies.” He added that while these regulations might initially pose challenges, they aim to create a safer and more reliable financial ecosystem. “Staying informed and adaptable to these changes is crucial for payment companies to remain compliant and competitive,” he added. Forward’s analysis pointed to a delicate balance that companies must maintain: driving innovation while navigating the complexities of regulatory compliance.

Müller nodded in agreement and pointed out the influence of big tech companies in this evolving landscape. “Companies like Apple and Google are integrating financial data into consumer applications, which significantly impacts how consumers interact with payment systems,” he observed. “The involvement of these tech giants is accelerating the adoption of new payment technologies and reshaping consumer behaviours.” Müller’s comment underscored the transformative power of big tech, not just as service providers but as key players influencing market dynamics and consumer expectations.

Schweber circled back to the discussion on fraud prevention, noting how technological advancements are essential in this fight. “The integration of AI and machine learning is indispensable in fraud detection. These technologies can analyse vast amounts of transaction data in real time, identifying and mitigating potential threats swiftly,” he said. This analysis revealed AI’s dual role in enabling new payment methods and safeguarding them against fraud, illustrating how technology can serve as both a catalyst and a protector in the payments landscape.

Forward then highlighted the potential for collaboration between payment companies and tech giants to enhance security measures. “By partnering with big tech, we can leverage their advanced technologies to improve our payment systems’ security and efficiency,” he delineated. This collaborative approach was seen as a strategic move to harness the strengths of various stakeholders in the ecosystem, driving innovation while mitigating risks.

As the discussion continued, it became evident that technological advancements and regulatory changes are driving significant shifts in the payments industry. However, the need for vigilance and proactive adaptation remains paramount. The participants agreed that staying agile and forward-thinking is essential to leverage these emerging trends and address the accompanying challenges effectively.

The discussion then transitioned to the most promising technological advancements currently shaping the payment sector and how companies are leveraging these innovations to stay ahead.

Thomas Müller began by laying out the transformative potential of software as a service (SaaS) in the payments industry. “The shift towards SaaS models is revolutionary,” he remarked. “By adopting SaaS, companies can deliver substantial value without needing to build every component from scratch.” Müller also discussed how Rivero’s dispute management product integrates various APIs from major card networks like MasterCard and Visa. He further explained the benefits to payments firms if they aggregate data across multiple sources to provide a seamless experience for bank agents and consumers, all through a single interface, enhancing efficiency and improving user experience.

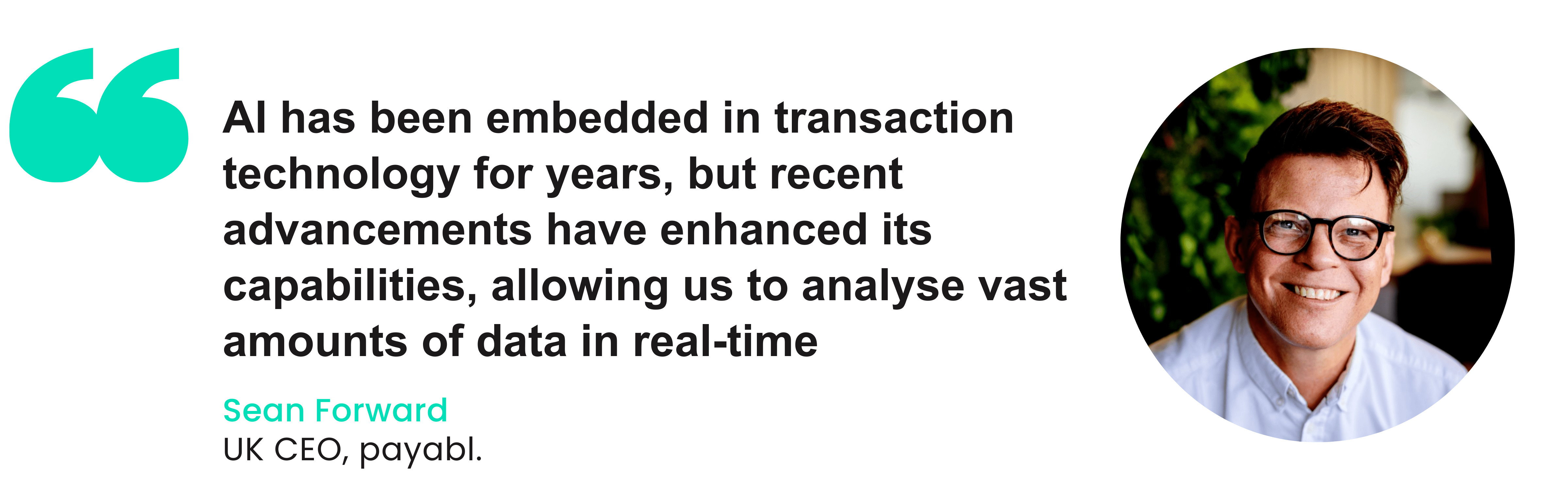

Sean Forward quickly picked up on this point, noting that AI and machine learning have become critical components in optimising payment processes. “AI has been embedded in transaction technology for years, but recent advancements have significantly enhanced its capabilities,” he remarked. He also discussed how AI personalises the customer experience, optimises transaction processing, and enhances fraud detection. “AI allows us to analyse vast amounts of data in real-time, enabling us to detect patterns and anomalies that would be impossible to identify manually,” he explained.

Alan Schweber agreed and elaborated further on AI’s role in fraud prevention. “AI is crucial in interpreting vast amounts of data at speed,” he noted. Schweber shared insights into how his company is seeking to leverage AI to tackle account-to-account (A2A) payments fraud. “By using AI, we can better understand customer behaviour and predict potential fraud, which is essential as real-time payments become more prevalent,” he said. This led to a broader discussion on how AI-driven fraud detection systems are becoming indispensable tools for payment companies, helping them stay one step ahead of cybercriminals.

The conversation then shifted towards the influence of big tech companies on the payments landscape. “The integration of financial data into consumer apps, such as Apple Wallet, is revolutionising how people interact with their financial information,” Forward pointed out. These advancements make it easier for consumers to manage their finances, track spending, and make informed decisions, fostering greater financial literacy and inclusion. The CEOs agreed that the seamless integration of these technologies into daily life is reshaping consumer expectations and behaviours.

Forward expanded on the potential of biometric authentication technologies in enhancing payment security. “Biometric authentication, such as fingerprint and facial recognition, offers a higher level of security than traditional methods,” he noted. These technologies are gaining traction in mobile payments, providing consumers with a secure and convenient way to authorise transactions. “Biometric authentication not only enhances security but also improves the user experience by making payments quicker and more seamless,” he noted.

As the session progressed, the CEOs agreed that while these technological advancements are promising, their successful implementation requires a strategic approach. Companies must invest in the right technologies, ensure robust security measures, and stay compliant with evolving regulations. They also highlighted the need for continuous innovation and adaptation to keep up with the rapidly changing payments industry landscape.

Müller summarised the group’s sentiment: “Embracing technological advancements such as SaaS, AI, blockchain, and biometric authentication is crucial for staying competitive in the payments sector. By leveraging these technologies, companies can enhance efficiency, improve security, and provide a better customer experience.” Schweber and Forward nodded in agreement, underscoring the importance of strategic planning and collaboration in driving the future of payments.

The conversation transitioned to how payment companies are adapting their solutions to meet the ever-evolving expectations of customers. The CEOs discussed the necessity of understanding customer needs and leveraging technology to improve the payment experience.

Thomas Müller delineated the importance of user experience, particularly in B2B SaaS solutions aimed at banks and financial institutions. “User experience is often overlooked in B2B applications, but it’s critical,” he asserted. Müller explained that improving the user interface and overall experience for both bank employees and end consumers can significantly enhance satisfaction and efficiency. “Rivero’s goal is to make its product interfaces as intuitive and user-friendly as possible, which helps banks serve their customers more effectively,” he added.

Sean Forward built on Müller’s point, discussing the necessity of providing merchants with the flexibility to accept various payment methods. He elaborated on how traditional credit and debit cards remain dominant, but there is a growing demand for alternative payment methods. “Our orchestration layer allows merchants to integrate various payment solutions, offering customers a broader choice,” he noted. Having this adaptability is important since it not only meets diverse consumer preferences but also positions merchants to capture a larger share of the market.

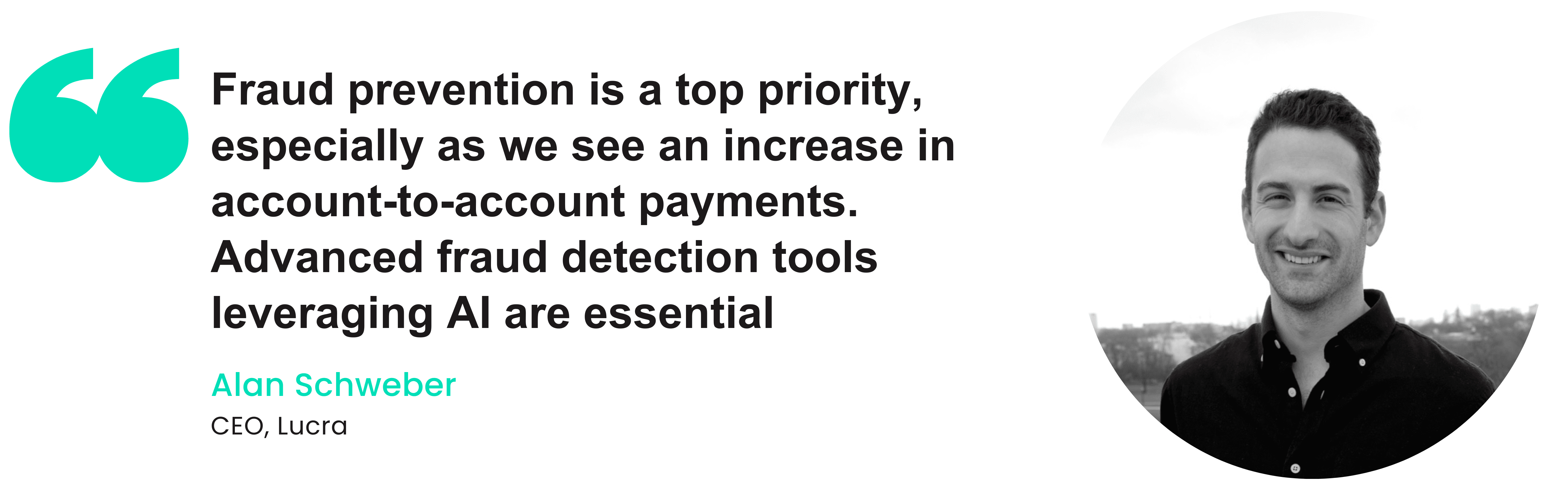

Alan Schweber underscored the critical role of fraud prevention in adapting payment solutions. “Fraud prevention is a top priority, especially as we see an increase in account-to-account payments,” he stated. Schweber explained that Lucra is developing advanced fraud detection tools that leverage AI to analyse transaction patterns and identify suspicious activities on payment recipients. “By using AI, banks are afforded the tools they need to screen payment recipients and protect their customers from fraud while ensuring a smooth and secure payment experience,” he remarked.

At this point, the conversation shifted to the regulatory changes affecting the panellists’ strategies for meeting customer needs.

Forward explained that regulatory compliance is becoming increasingly multiplex, especially with the introduction of new digital currencies. He called for payment companies to stay abreast of regulatory changes and ensure their solutions comply with evolving standards. “Adapting to regulatory changes is crucial for maintaining trust and credibility with our customers,” he noted.

Müller echoed the importance of regulatory compliance, highlighting that it also presents an opportunity for innovation. “Compliance shouldn’t just be seen as a hurdle; it can also drive innovation,” he said. Müller explained that companies can develop more robust and secure payment solutions by proactively addressing regulatory requirements. “We view compliance as a key component of Rivero’s innovation strategy, ensuring our products are effective and adhere to security and reliability standards,” he stated.

The conversation then moved towards the importance of partnerships in adapting payment solutions. Schweber highlighted the benefits of collaborating with other companies to enhance product offerings. “Partnerships allow us to leverage each other’s strengths and provide more comprehensive solutions to our customers,” he said. Schweber shared an example of how his company is exploring partnerships with banks to create a fraud data-sharing network. “By collaborating, we can share valuable insights and develop more effective fraud prevention strategies,” he noted.

Forward added that partnerships are essential for staying ahead of technological advancements. “The payments industry is constantly evolving, and partnerships help us stay at the forefront of innovation,” he said. Forward explained that by working with technology providers, payabl. has the capacity to integrate the latest advancements into its solutions. “Our partnerships enable us to offer our customers payment solutions that meet their changing needs,” he remarked.

As the discussion continued, it became evident that adapting payment solutions to meet changing customer expectations requires a multifaceted approach. Payment companies can stay ahead of industry trends by focusing on user experience, fraud prevention, regulatory compliance, strategic partnerships, and providing customers with the best possible service.

The final segment of the payments lab session centred on leadership and how CEOs inspire innovation and forward-thinking within their organisations. This discussion highlighted the importance of nurturing a culture of continuous improvement and adaptability in the rapidly evolving payments industry.

Thomas Müller began by discussing the significance of aligned autonomy within his company. “We set the North Star for our strategic goals and then trust our team to navigate towards it with a high degree of autonomy,” he explained. Müller added that regular communication is key to maintaining alignment and ensuring everyone works towards the same objectives. “We hold weekly meetings with our direct reports and monthly all-hands meetings to keep everyone informed and engaged,” he noted.

Sean Forward jumped in, explaining the role of education and personal development in cultivating leadership and innovation. “We encourage our team members to pursue continuous learning and provide opportunities for them to network and grow professionally,” he said. Forward elaborated that payabl., supports its employees in attending industry conferences, participating in professional courses, and engaging with peer networks. “This exposure helps our team stay current with industry trends and brings fresh ideas into the company,” he added.

Alan Schweber agreed, adding that fostering a culture of open communication is essential for innovation. “Innovation thrives when team members feel safe to propose new ideas without fear of criticism,” he stated. Schweber explained that Lucra holds regular brainstorming sessions and maintains an open-door policy for feedback. “We want to create an environment where creativity is encouraged, and all ideas are considered,” he said.

The conversation then shifted to the role of trial and error in driving innovation, particularly how the CEOs encourage their teams to experiment and learn from failures.

Müller responded, “We recognise that trial and error is fundamental to the innovation process. By allowing our teams to experiment, we can discover new solutions and approaches that might not be apparent through conventional methods.” He drew attention to the importance of learning from failures and iterating quickly. “Innovation involves taking risks, and sometimes those risks don’t pay off. What’s important is that we learn from these experiences and continue to push forward,” he said.

Forward echoed this sentiment, affirming that celebrating successes, no matter how small, can boost morale and encourage further innovation. “Acknowledging the hard work and achievements of our team members motivates them to keep striving for excellence,” he observed. This positive reinforcement helps build a culture where innovation is valued and pursued actively.

Schweber highlighted the importance of setting clear expectations and goals. “Clarity in what we aim to achieve helps our team focus their efforts and drive innovation towards specific outcomes,” he noted. By communicating these objectives clearly and consistently, leaders can ensure that all team members are working towards the same vision.

As the session drew to a close, the CEOs agreed that inspiring innovation and forward-thinking within organisations requires a multifaceted approach. By focusing on education, clear communication, direct customer engagement, and a supportive culture that encourages risk-taking and celebrates success, leaders can foster an environment where innovation thrives.

In conclusion, the roundtable underscored the importance of adaptive leadership in navigating the challenges and opportunities in the payments industry. By integrating advanced technologies, fostering industry collaboration, and maintaining a keen awareness of regulatory developments, payment companies can stay ahead of the curve and drive the future of payments.

A 2025 survey of UK retailers reveals how payment challenges and innovation priorities are shaping merchant strategies across the sector.

UK SME survey shows open banking intrigues merchants with faster, cheaper payments, but gaps in awareness and security fears slow adoption.

The Bank of England’s offline CBDC trials show it’s technically possible—but device limits, fraud risks, and policy gaps must still be solved.

The Payments Association

St Clement’s House

27 Clements Lane

London EC4N 7AE

© Copyright 2024 The Payments Association. All Rights Reserved. The Payments Association is the trading name of Emerging Payments Ventures Limited.

Emerging Ventures Limited t/a The Payments Association; Registered in England and Wales, Company Number 06672728; VAT no. 938829859; Registered office address St. Clement’s House, 27 Clements Lane, London, England, EC4N 7AE.

Log in to access complimentary passes or discounts and access exclusive content as part of your membership. An auto-login link will be sent directly to your email.

We use an auto-login link to ensure optimum security for your members hub. Simply enter your professional work e-mail address into the input area and you’ll receive a link to directly access your account.

Instead of using passwords, we e-mail you a link to log in to the site. This allows us to automatically verify you and apply member benefits based on your e-mail domain name.

Please click the button below which relates to the issue you’re having.

Sometimes our e-mails end up in spam. Make sure to check your spam folder for e-mails from The Payments Association

Most modern e-mail clients now separate e-mails into different tabs. For example, Outlook has an “Other” tab, and Gmail has tabs for different types of e-mails, such as promotional.

For security reasons the link will expire after 60 minutes. Try submitting the login form again and wait a few seconds for the e-mail to arrive.

The link will only work one time – once it’s been clicked, the link won’t log you in again. Instead, you’ll need to go back to the login screen and generate a new link.

Make sure you’re clicking the link on the most recent e-mail that’s been sent to you. We recommend deleting the e-mail once you’ve clicked the link.

Some security systems will automatically click on links in e-mails to check for phishing, malware, viruses and other malicious threats. If these have been clicked, it won’t work when you try to click on the link.

For security reasons, e-mail address changes can only be complete by your Member Engagement Manager. Please contact the team directly for further help.