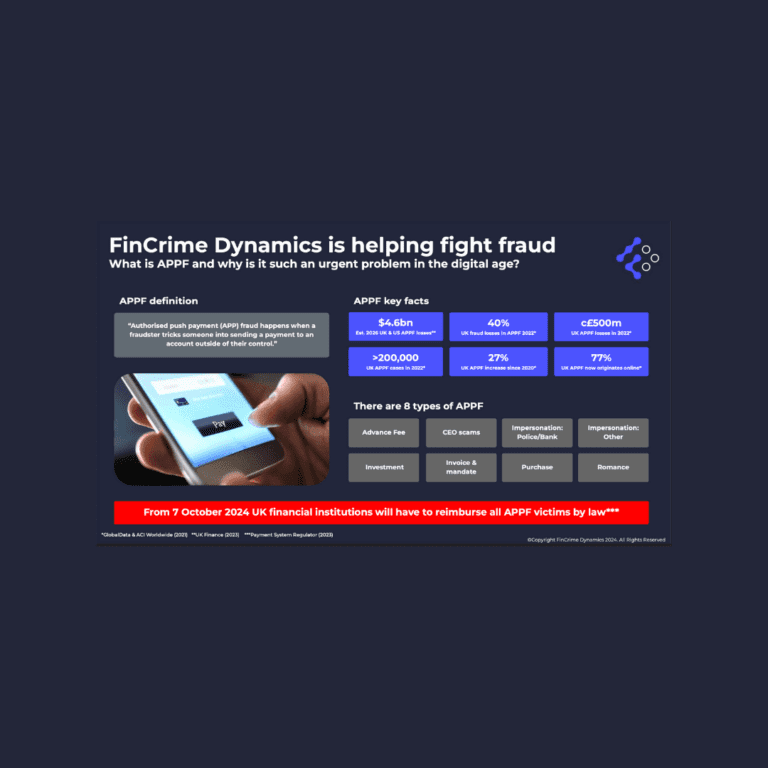

From 7 October this year, all consumers who are victims of automated push payment (‘APP’) fraud paid via faster payments must be reimbursed within 5 business days, with the cost split equally between the paying and receiving payment service providers (PSPs).

With five months to go, what should PSPs do now to prepare?

PSPs can look to regulatory expectations to inform their preparations now and set themselves up for success come October. In particular, the PSR’s final Policy Statement includes a section addressing ‘PSP readiness’, and the FCA has published common weaknesses they identified in PSP firm’s antifraud controls and complaint handling processes. From these, PSPs can get a good indication of broader activities they should be doing over the coming months in the run-up to implementation.

To comply with regulator expectations under the new rules, PSPs need to ensure that APP fraud is easy to report and reimbursement is made within the new regulatory timescales while ensuring consumers are given clear communication throughout the process.

PSPs should invest in their end-to-end anti-fraud framework now to avoid costly non-compliance and reputational damage further down the line. The PSR and FCA will be on the lookout for any firms seen to be underperforming in either reimbursement or fraud prevention.

Log in to access complimentary passes or discounts and access exclusive content as part of your membership. An auto-login link will be sent directly to your email.

We use an auto-login link to ensure optimum security for your members hub. Simply enter your professional work e-mail address into the input area and you’ll receive a link to directly access your account.

Instead of using passwords, we e-mail you a link to log in to the site. This allows us to automatically verify you and apply member benefits based on your e-mail domain name.

Please click the button below which relates to the issue you’re having.

Sometimes our e-mails end up in spam. Make sure to check your spam folder for e-mails from The Payments Association

Most modern e-mail clients now separate e-mails into different tabs. For example, Outlook has an “Other” tab, and Gmail has tabs for different types of e-mails, such as promotional.

For security reasons the link will expire after 60 minutes. Try submitting the login form again and wait a few seconds for the e-mail to arrive.

The link will only work one time – once it’s been clicked, the link won’t log you in again. Instead, you’ll need to go back to the login screen and generate a new link.

Make sure you’re clicking the link on the most recent e-mail that’s been sent to you. We recommend deleting the e-mail once you’ve clicked the link.

Some security systems will automatically click on links in e-mails to check for phishing, malware, viruses and other malicious threats. If these have been clicked, it won’t work when you try to click on the link.

For security reasons, e-mail address changes can only be complete by your Member Engagement Manager. Please contact the team directly for further help.